2025 Beauty Marketing Study

New Insights Into Clean Beauty and the Roles of AI, TikTok, and GLP-1 Drugs Like Ozempic

New Insights Into Clean Beauty and the Roles of AI, TikTok, and GLP-1 Drugs Like Ozempic

The beauty industry continues to evolve at a rapid pace, with new technology and platforms giving consumers more ways than ever to explore personalized recommendations, evaluate products, and make purchases. Tinuiti surveyed 1,003 beauty shoppers in January 2025 to understand what’s driving purchase decisions and how the customer journey is changing, gaining insight into key developments like the rise of AI chatbots, weight-loss drugs, and video formats like Get Ready With Me.

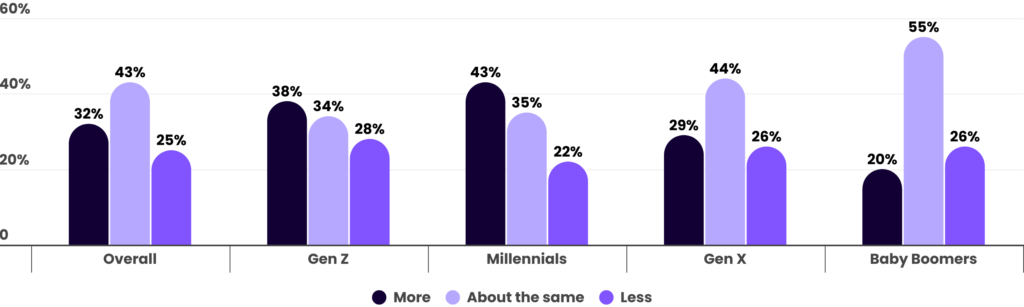

Asked how their current spending compares to a year ago, 32% said that they’re spending more compared to 25% who responded that they’re spending less. With 43% of beauty shoppers spending about the same as a year ago, 75% of those studied are spending at least as much as they were a year ago, the same figure observed in last year’s survey results.

Gen Z and millennials were more likely than older generations to report that they had increased their beauty spending with 42% saying they were spending more than a year ago. For Gen X and baby boomers, that rate was just 25%. Baby boomers were the only generation where a larger share said they had decreased their beauty spending than increased it.

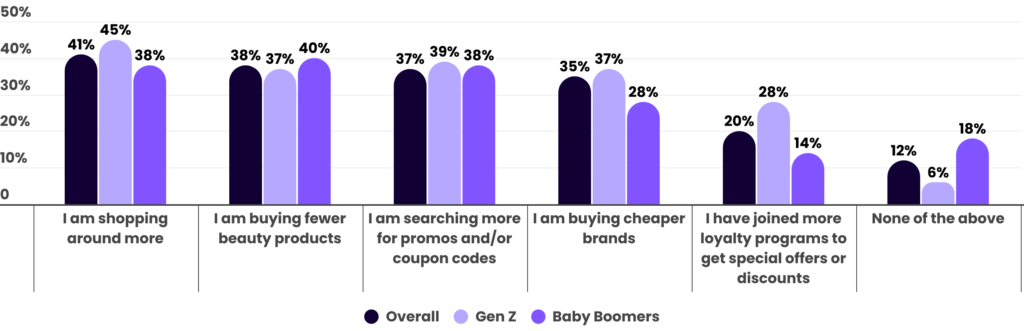

While the rate of price inflation has cooled, beauty shoppers still say it’s having an impact on their shopping. Fully 41% say they shopped around more over the past year because of inflation, while 38% purchased fewer products and 37% are searching more for promotions and coupon codes.

Among Gen Z, 37% of beauty shoppers reported buying cheaper brands, which was well above the 28% share of baby boomers who said the same. Gen Z was also much more inclined than baby boomers were to join loyalty programs to get product discounts, with 28% of Gen Z having done so compared to just 14% among baby boomers.

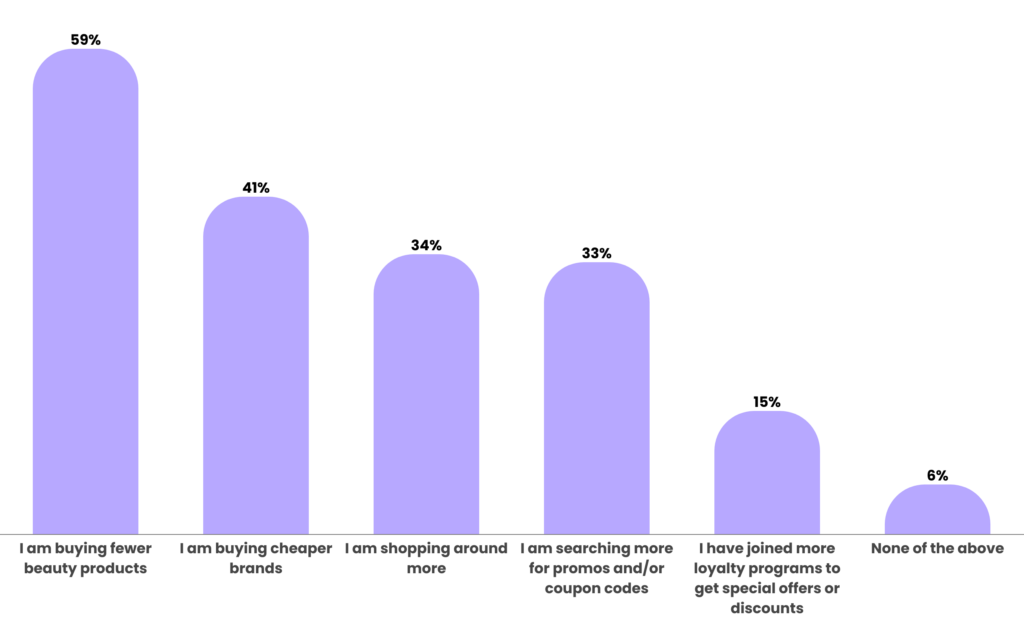

For those beauty shoppers who said that they had reduced their spending on beauty products in the past year, the most common response to inflationary pressures has been to simply buy fewer products, with 59% making that choice. The next most common response was to buy cheaper beauty brands at 41% and to shop around more at 34%.

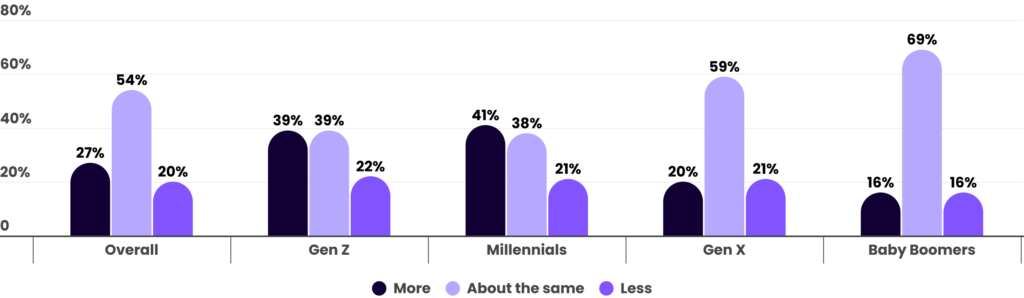

Looking to the year ahead, a majority of respondents expect to buy about the same amount of beauty products compared to the previous year, whether online or in a physical store. Among those who do expect to adjust their beauty product shopping, more respondents expect to increase their purchases than expect to decrease them.

Gen Z and millennials were twice as likely as Gen X and baby boomers were to say they expect to buy more beauty products over the next year. Gen Z in particular is still building its spending power, and they also expressed more openness than older generations to trying new beauty products and brands.

Recently introduced and potentially forthcoming tariffs may meaningfully impact demand for brands that are forced to raise prices as a result. Canada, China, and Mexico, each currently in the crosshairs of possible tariffs, are among the biggest suppliers of imported beauty products in the US.

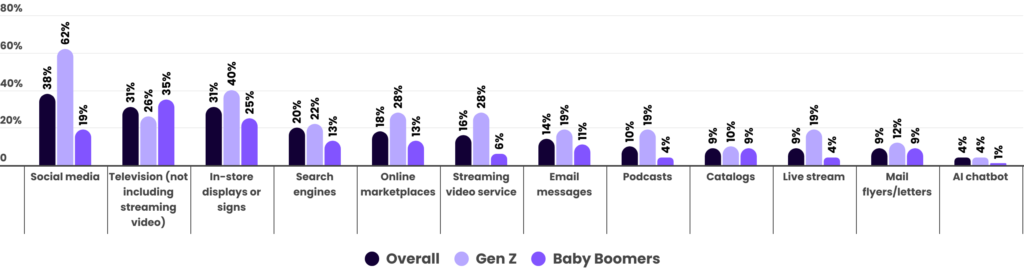

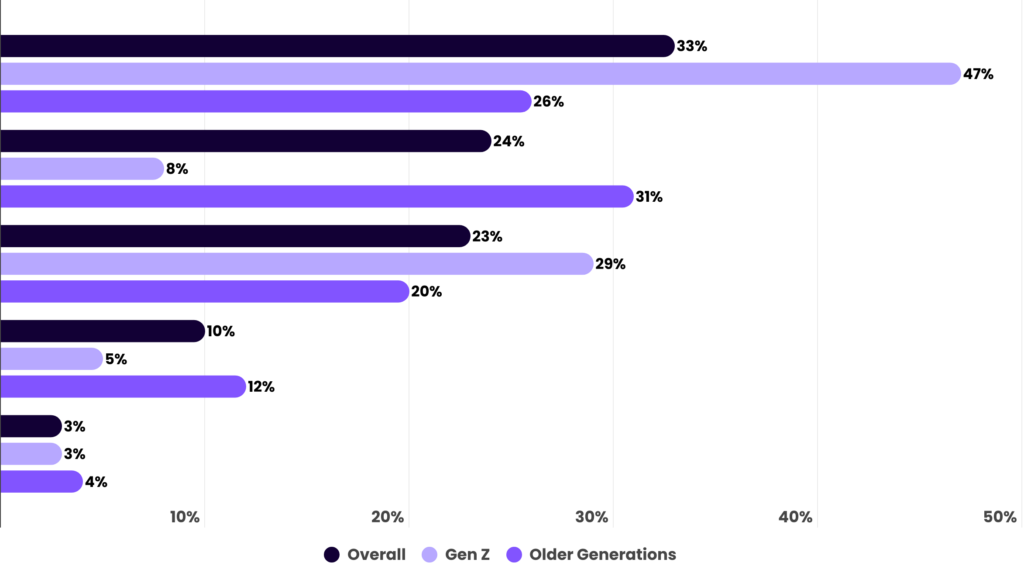

Asked where they recalled seeing or hearing about a new beauty product that they later went on to purchase in the last year, 38% of respondents selected social media, the top response. This was followed by television and in-store displays/signs, which both garnered selections from 31% of respondents.

An impressive 62% of Gen Z beauty shoppers said that they had discovered a beauty product on social media that they went on to purchase in the past year, which was 43 points higher than the 19% share of baby boomers who said the same. The next largest gap was for streaming video services, which was selected by 28% of Gen Z, but just 6% of baby boomers. Traditional television was the only channel of beauty product discovery chosen by a larger share of boomers than Gen Z.

AI chatbots helped 4% of beauty shoppers find new products that they later went on to purchase, a figure that is likely to rise as adoption of generative AI platforms grows.

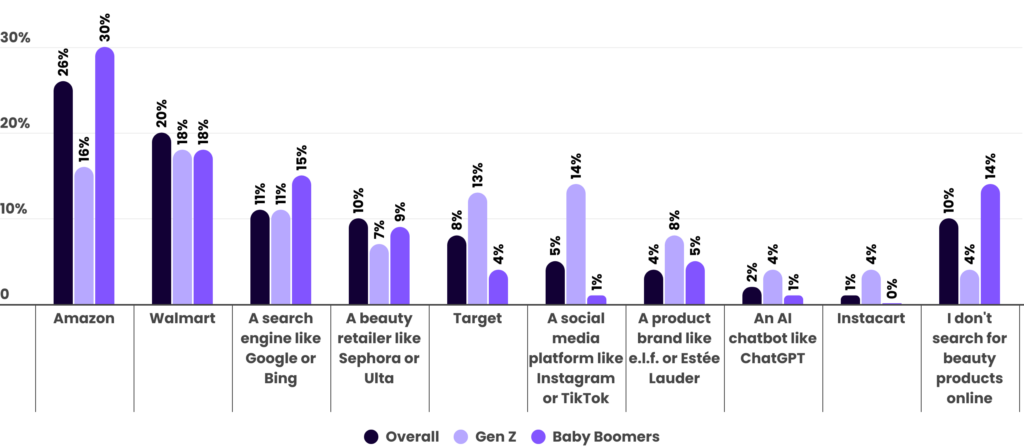

Looking over at where shoppers typically start searches for beauty products online, AI chatbots were selected by only 2% of respondents, as big ecommerce sites like Amazon and Walmart were much more likely to attract shoppers for initial searches. Traditional search engines like Google or Bing were the third most common starting point, while beauty retailers like Sephora or Ulta came in fourth.

AI chatbots fared a bit better for beauty product search among Gen Z and millennials, with 4% of each group selecting it as their first choice. Social media, however, saw the strongest lift for Gen Z compared to other generations with 14% of Gen Z choosing it for beauty product search compared to just 5% across all respondents.

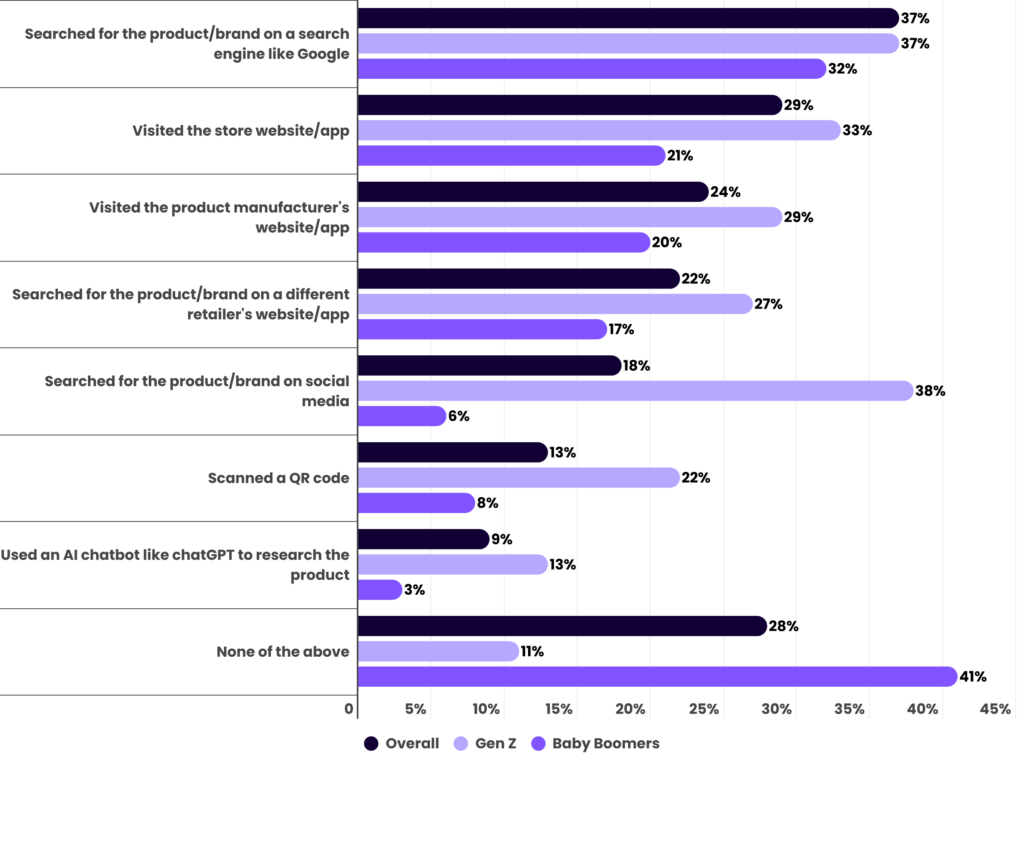

AI chatbots also play a more significant role when it comes to in-store actions, with 9% of respondents saying they’ve researched a product using an AI chatbot to learn more about it while in a store. Respondents were most likely to say they turn to traditional search engines like Google for in-store research, but 18% indicated that they search on social media, a figure that jumps to 38% for Gen Z.

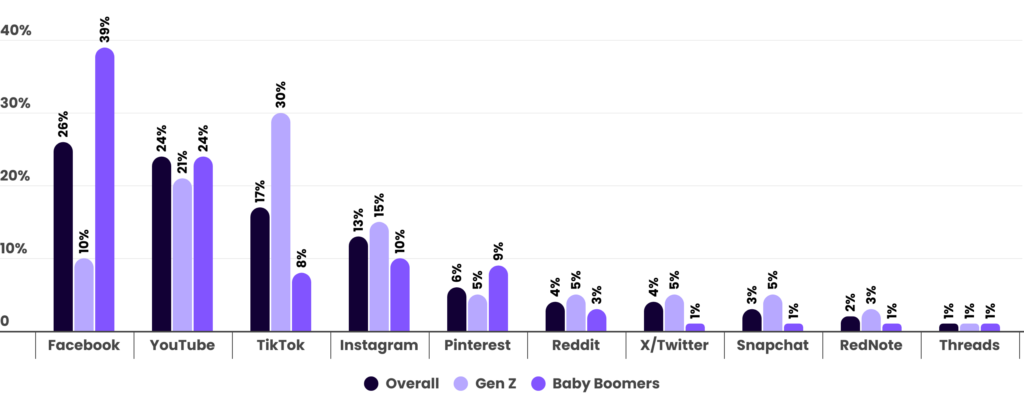

Fully 26% of respondents who discover new beauty products on social media said that they do so most frequently on Facebook. YouTube came in a close second at 24%, with TikTok in third at 17%.

These results vary considerably across generations, though. For Gen Z, TikTok is easily the top choice for beauty product discovery on social media, while Facebook is a distant fourth. Among the platforms with the highest overall ranking, YouTube saw the most consistent response rate across generations with 21% of Gen Z making it their top choice along with 24% of baby boomers.

While TikTok is currently back online in the US, questions about its future continue to swirl. If it were ultimately banned, those who say TikTok is the social media platform where they most often discover new products were most likely to choose Instagram as the platform they would use most often for beauty product discovery. This was followed by Facebook and YouTube, and all three of the top TikTok alternatives have invested in vertical short form video over the last few years.

With 47% choosing it, Instagram was the top TikTok alternative for Gen Z, but Facebook ranked better than Instagram among older respondents who currently discover beauty products most frequently on TikTok. Again, YouTube saw more consistent support with 29% of Gen Z choosing it as their top TikTok alternative along with 20% older generations.

Nearly two out of three beauty shoppers studied say they’ve purchased a beauty product on the recommendation of an influencer over the past year. Fully 11% said they did so frequently and 12% responded that they did so very frequently.

Influencers held greater sway among younger generations with 90% of Gen Z beauty shoppers saying they had bought a beauty product in the past year based on the recommendation of an influencer. Just 41% of baby boomers said the same. Similar shares of Gen Z and millennials said that they had frequently or very frequently bought beauty products because of influencers, but millennials were twice as likely as Gen Z to say they never did.

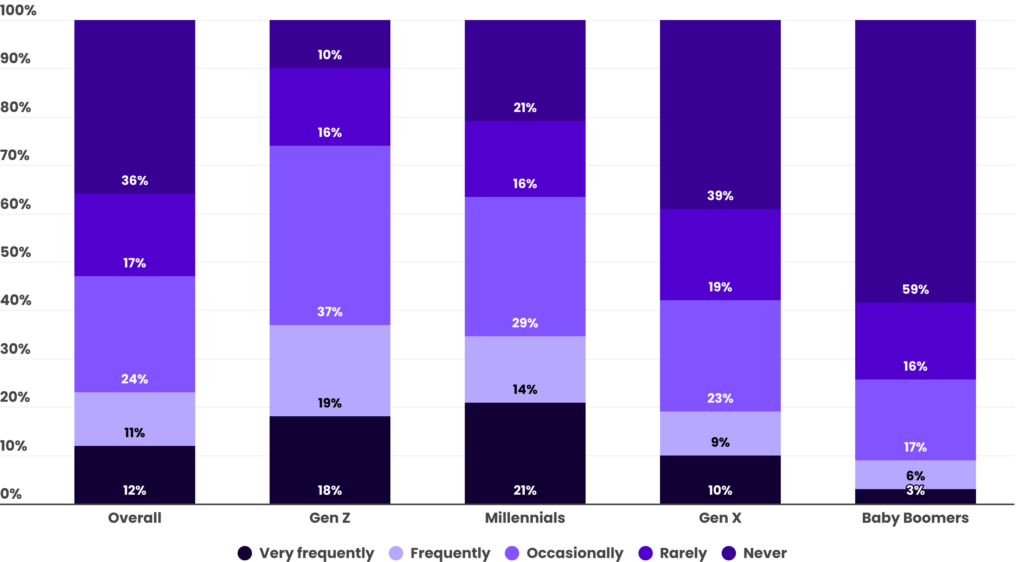

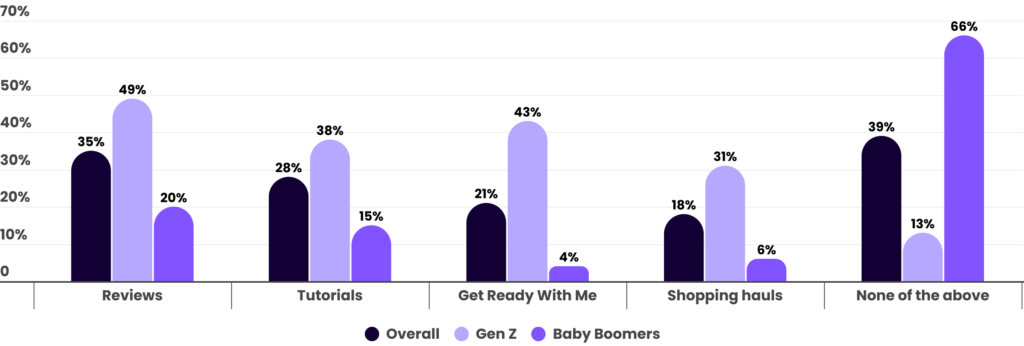

When it comes to what kinds of video content beauty shoppers are most likely to consume, reviews were the top selection, followed by tutorials. Fully 21% of shoppers say they regularly watch Get Ready With Me (GRWM) videos, and 18% tune into shopping hauls.

Gen Z was much more likely than average to say that they do regularly watch each of the four types of beauty videos they were asked about, but GRWM videos saw the biggest lift among this group and were the second most popular option behind reviews.

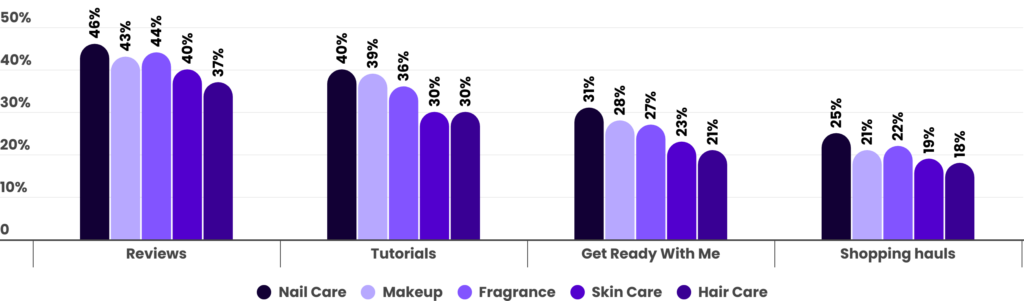

Looking at video preferences broken down by the beauty product categories respondents expect to purchase in 2025, those planning to purchase nail care products showed the greatest interest in all four types of beauty videos they were asked about. Makeup purchasers also showed relatively strong interest across video types, particularly for tutorials.

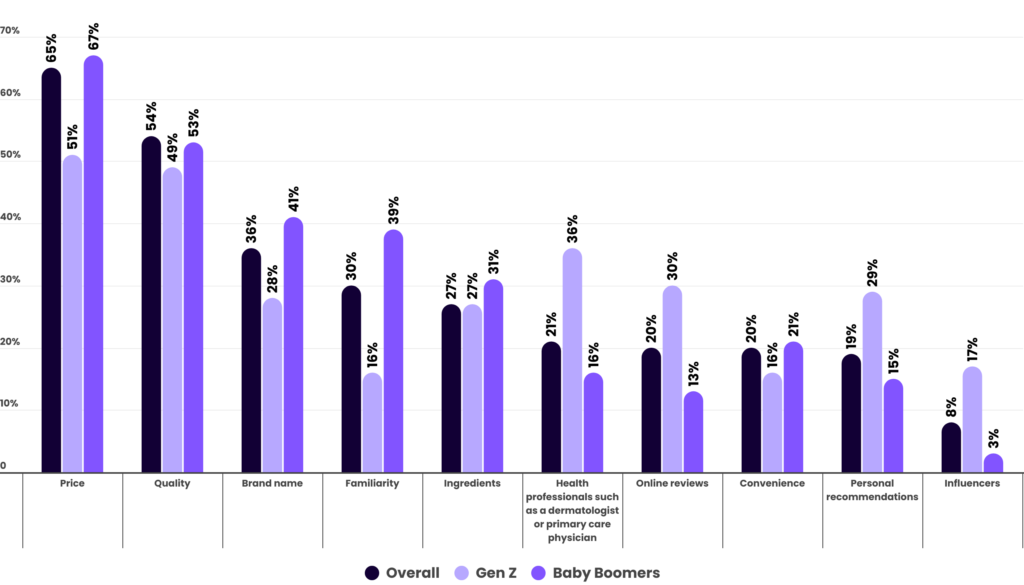

Asked to select the three most important influences on their beauty purchases, 65% selected price, the top response. This was followed by quality and brand name as the second and third most influential attributes.

While price was the top influence on beauty purchases for Gen Z, the younger generation was less likely than average to select each of the top four overall influences. Instead, Gen Z’s influences were more spread out with particularly strong showings for health professionals, online reviews, personal recommendations, and influencers.

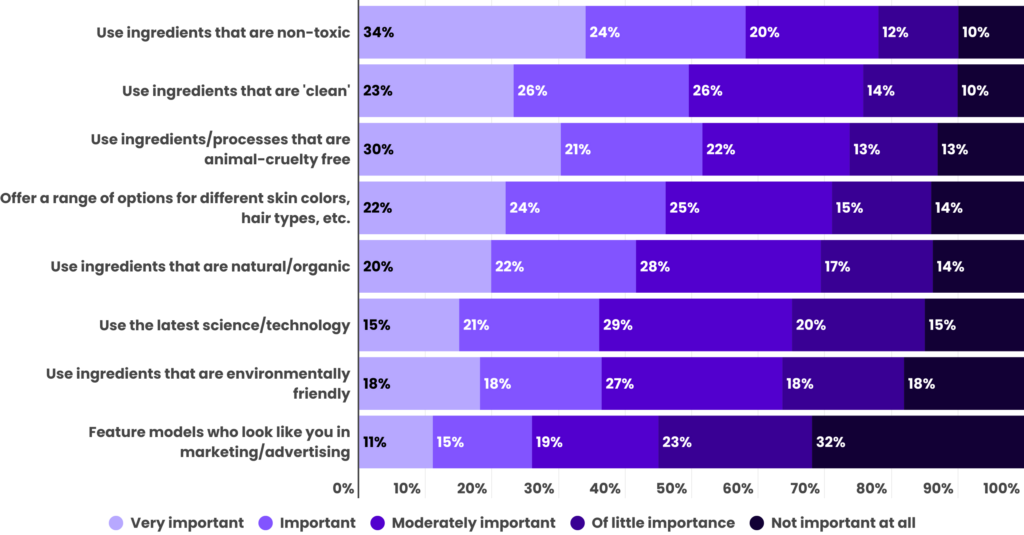

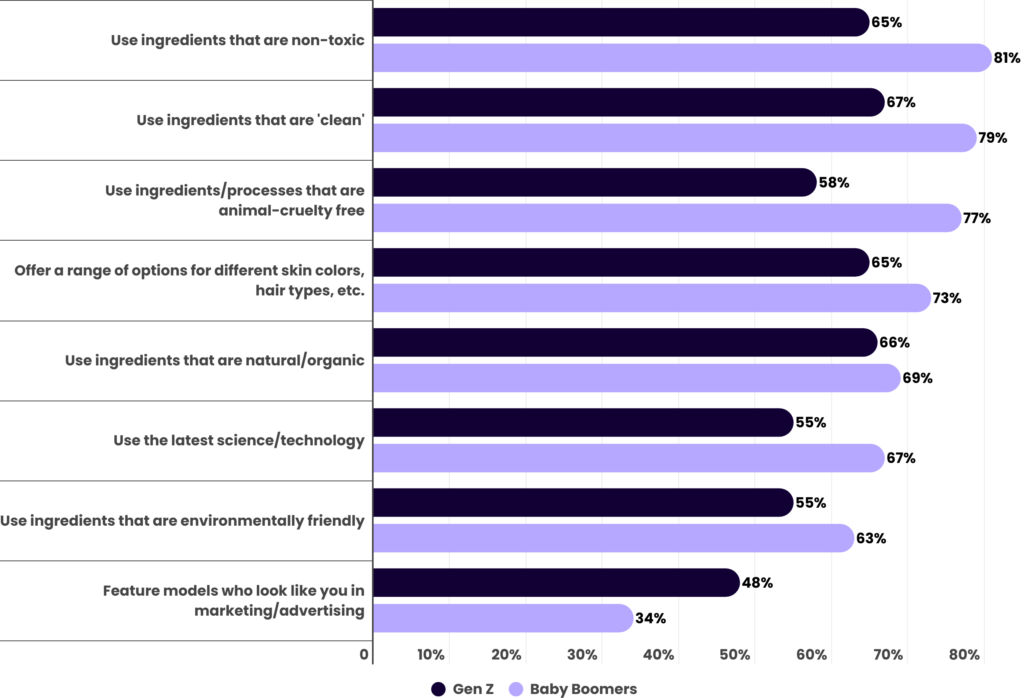

Considering the impact of specific attributes of beauty brands, products, and messaging to consumers, being ‘clean’ has become an important selling point for many beauty shoppers with 75% saying a product using clean ingredients is at least moderately important to their beauty purchase decision.

That rate nearly matches the bar set of a product being ‘non-toxic’, which was at least moderately important to 77% of beauty shoppers. Similar attributes to being clean or non-toxic were less likely to be deemed important by shoppers with 64% saying using environmentally friendly ingredients was at least moderately important, while 69% said the same about a product being natural/organic.

Consumers cared less about seeing models who look like them in marketing/advertising than whether or not the brand in question offered a range of options for different skin colors and hair types. As such, it’s not enough to feature diversity in marketing and brands need to support diverse consumers with products tailored to their needs.

For all but one of the eight beauty product attributes they were asked about, Gen Z was less likely than baby boomers to say that the attribute was at least moderately important to their purchase decision. The exception was for featuring models who look like them in beauty product marketing, which was at least moderately important to 48% of Gen Z, but just 34% of baby boomers.

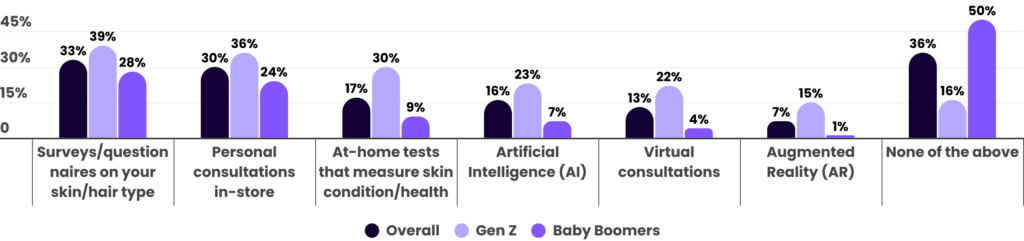

Asked if they’d ever used technology such as filters to see digitally how a product would look on them before purchasing, 34% said they had. That rate rises to 55% among Gen Z and jumps to 69% among members of Gen Z that expect to purchase makeup this year.

While filters are largely based on augmented reality (AR) and in some cases artificial intelligence (AI), consumers may not associate them as such. Just 7% of respondents say they’ve used AR to receive more personalized beauty product recommendations, with 16% saying they’ve used AI.

By comparison, 33% of respondents say they’ve used surveys/questionnaires, and 30% have done in-person consultations. These IRL consults were more popular than some remote options such as virtual consultations and at-home tests that measure skin condition/health.

Gen Z was much more likely than baby boomers to say they had used each of the personalized beauty product recommendation methods they were asked about. The biggest gaps between the two generations were for athome tests, virtual consultations, and AI.

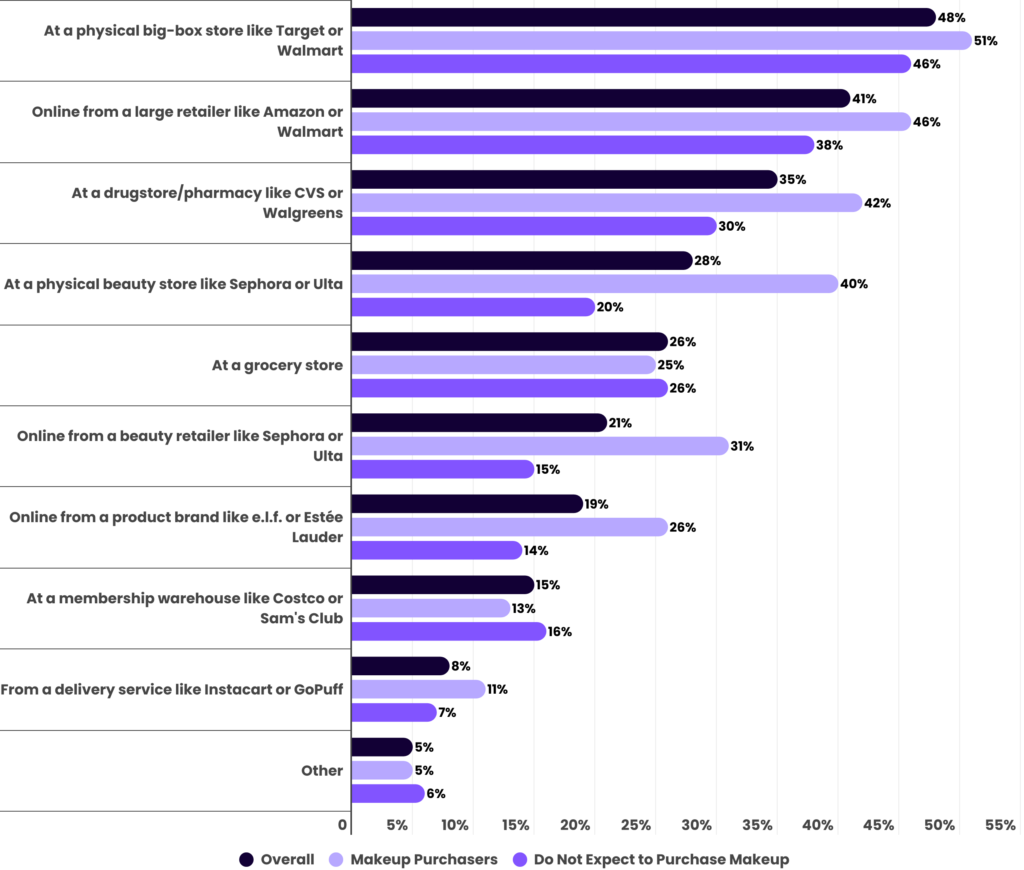

Asked where they’ve bought beauty products in the last year, the most popular response was big-box stores like Target or Walmart, followed by online from a large retailer in second. Drugstores/pharmacies were the only other destination chosen by at least a third of respondents.

Beauty retailers like Sephora and Ulta are making inroads with consumers, both online and IRL. Fully 28% of respondents say they’ve gone to a beauty retailer’s physical store for purchases, and 21% have gone to their online destinations.

For those that expect to purchase makeup in 2025, big-box stores were still the number one reported option for past beauty purchases, but beauty retailers see big gains in share with 40% of makeup purchasers having bought at physical beauty stores and 31% having bought from beauty retailers online.

Beauty retailers are also more likely to be frequented by younger beauty shoppers as 37% of Gen Z reported buying beauty products at a physical beauty store in the past year, compared to just 18% among baby boomers. Gen Z was also much likely to say they had bought directly from a product brand online or used a delivery service like Instacart or GoPuff.

Asked if they had ever purchased beauty products directly on TikTok, Facebook, or Instagram, 42% of respondents said that they had done so on at least one of these platforms. Fully 27% of respondents said they’d made a purchase on Facebook, while TikTok and Instagram were selected by 23% and 22%, respectively.

Among Gen Z respondents, 72% reported purchasing a beauty product directly either on TikTok, Facebook, or Instagram, with 54% saying they had done so specifically on TikTok, the highest of the three. Just 21% of baby boomers had bought beauty products on one of these platforms, with Facebook ranking the highest at a share of 15%.

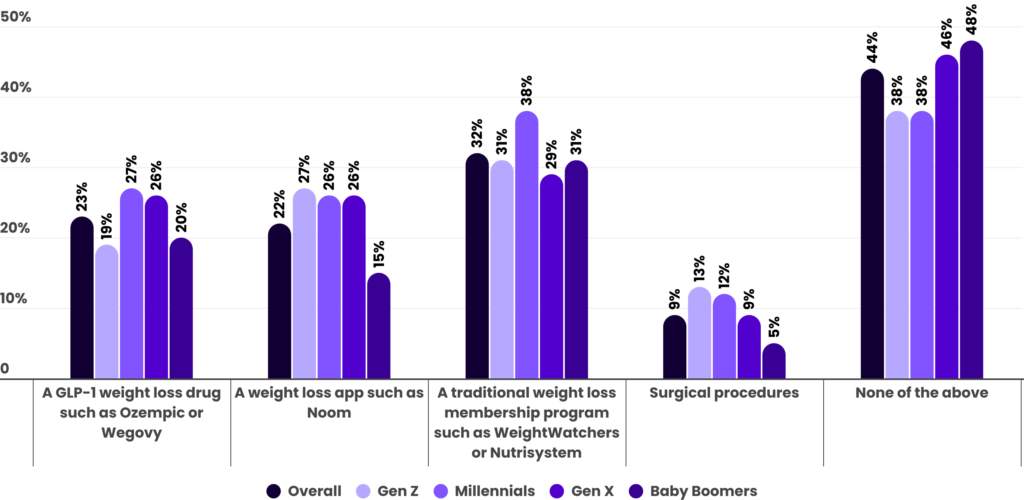

GLP-1 weight loss drugs like Ozempic and Wegovy have quickly grown in popularity, and 23% of beauty shoppers studied say they’d consider using them. This outpaces the share of respondents who say they’d use a weight loss app like Noom or undergo surgical procedures, but trails the share who would join a traditional weight loss program like Weight Watchers or Nutrisystem.

Millennials and Gen X were the most likely to consider using a GLP-1 weight loss drug with 27% of millennials saying they would consider it, along with 26% of Gen X. For Gen Z and baby boomers, around one out of five respondents said they would consider using a GLP-1 drug for weight loss.

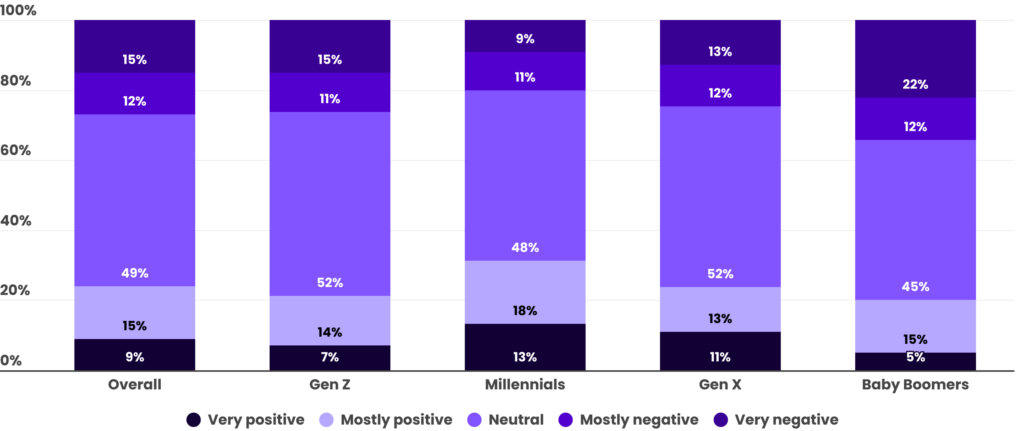

Current attitudes toward the use of GLP-1 drugs aren’t overly positive or negative, with the most popular stance on such drugs being neutral. Fully 25% of respondents felt mostly or very positive about GLP-1s, while 26% felt mostly or very negative.

Along with being the most likely to consider using a GLP-1 weight loss drug, millennials also had the most positive views of the use of GLP-1 drugs generally. Just over 31% of millennial beauty shoppers had a positive view of GLP-1 drugs, while just 20% had a negative view. Baby boomers had the most negative views of GLP-1 drugs with negative responses outweighing positive ones by 13 points.

Check out our most recent Beauty Marketing Study for more exclusive insights.