Research

Digital Ads Benchmark Report Q2 2026

Quarterly Trends Across Google, Meta, Amazon, And More

Quarterly Trends Across Google, Meta, Amazon, And More

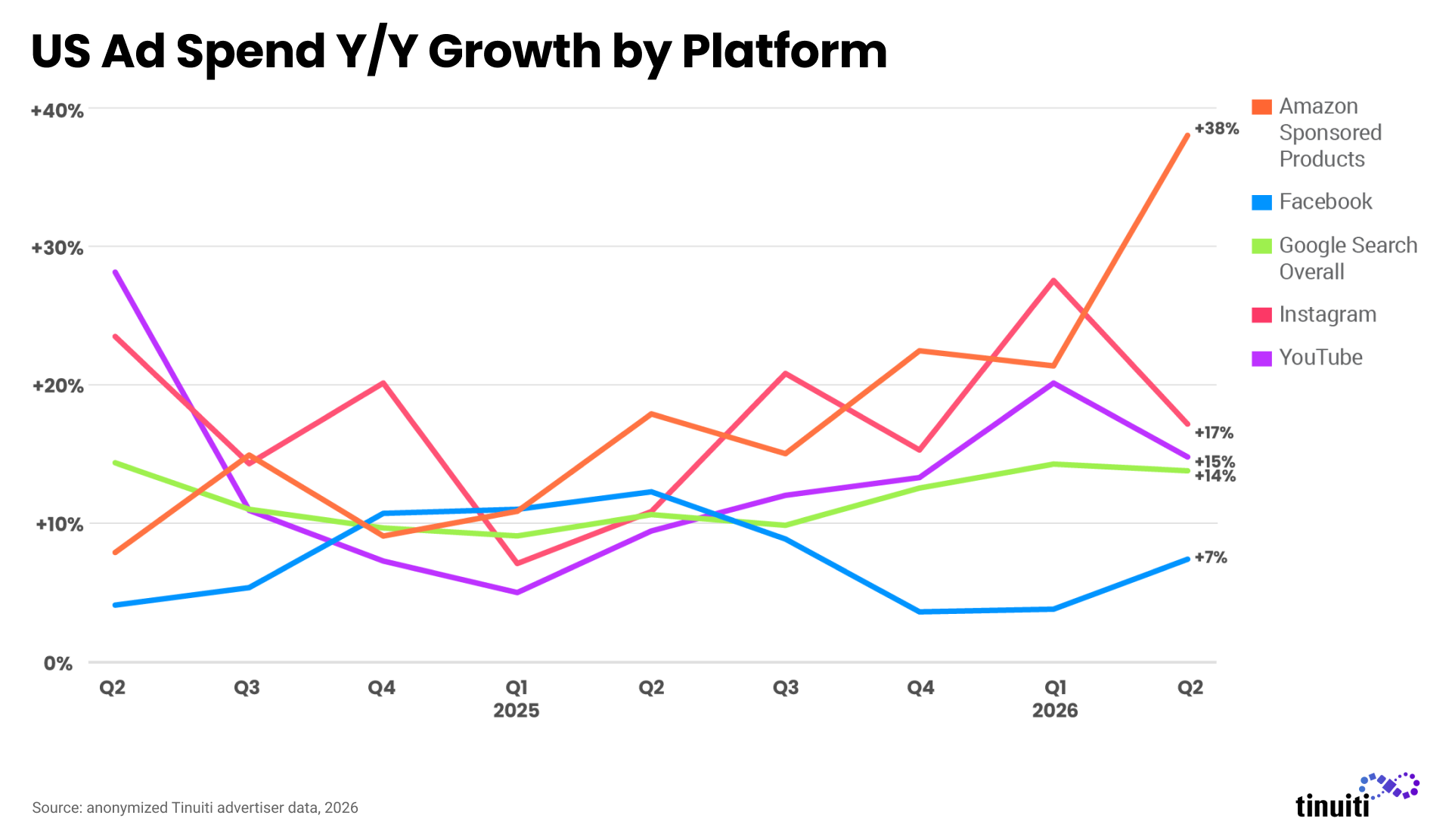

Across five of the largest digital ad segments in the US, Amazon’s Sponsored Products was a standout in Q2 2026 with same-site spending growth jumping sharply as Amazon moved its Prime Day sales event up to June from its typical July timing.

Google search and YouTube, along with Instagram, all saw slower ad spending growth in the quarter in the face of stronger year-ago comps, while Meta’s other marquee property, Facebook, rebounded from a relatively weak start to the year.

More than four dozen charts will help prepare you for the back half of the year, unpacking all of the key shifts across search, social, streaming, display, and commerce media.

Increase in Amazon DSP spending

of all Instagram ad impressions now attributed to Reels

Amazon’s US Google shopping impression share against the median retailer