Three Key Advertising Trends from Amazon Prime Big Deal Days 2023

Amazon once again tried to jumpstart Q4 shopping with a Prime member sales event in mid-October, continuing a strategy that started with last year’s Prime Early Access Sale. While the event was renamed Prime Big Deal Days (PBDD), it held similar promise of driving up demand relative to what would otherwise be expected so early in the final quarter of the year.

Here we’ll unpack three of the key trends Amazon advertisers observed during this year’s fall event, which ran October 10 and 11.

Compared to the Prime Early Access Sale of 2022, vendors and sellers invested much more in Amazon Sponsored Products, as spend rose 25%, driven primarily by a 21% increase in CPC. The increase in the cost of ad clicks was fairly in line with the expected value of those clicks, with the sales attributed to Sponsored Products growing 23%, nearly the same as spend growth.

While some observers describe PBDD as a fall Prime Day, the reality is that the October event presents a smaller opportunity for brands than Amazon’s premiere July event. Relative to Prime Day 2023, Sponsored Products advertisers spent 42% less with 36% fewer clicks during PBDD, as there weren’t as many shoppers flocking to Amazon for the fall event.

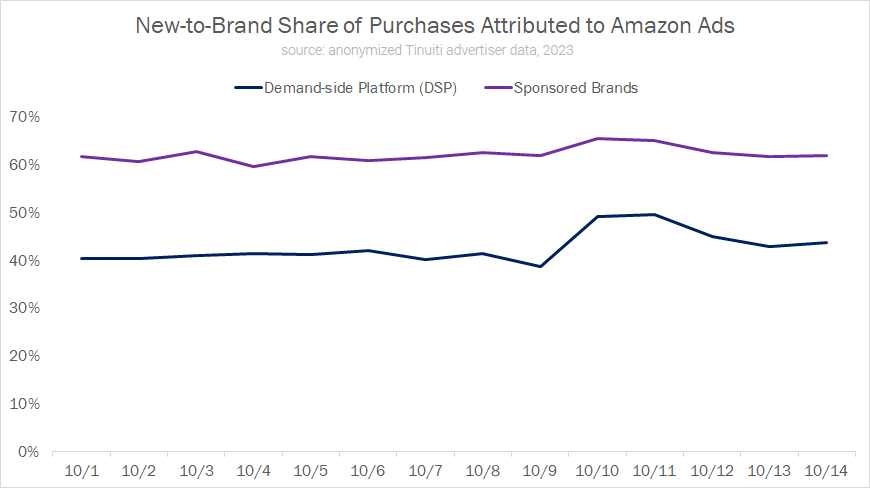

A big reason why brands are willing to invest heavily in Prime member sales events is the potential to get in front of new customers. The PBDD delivered a bump in new-to-brand customer share, with 65% of Sponsored Brands purchases attributed to new-to-brand customers compared to an average of 61% over the first nine days of October. Amazon DSP new-to-brand purchase share also jumped, rising from an average of 41% in the first nine days of October to 49% during the event.

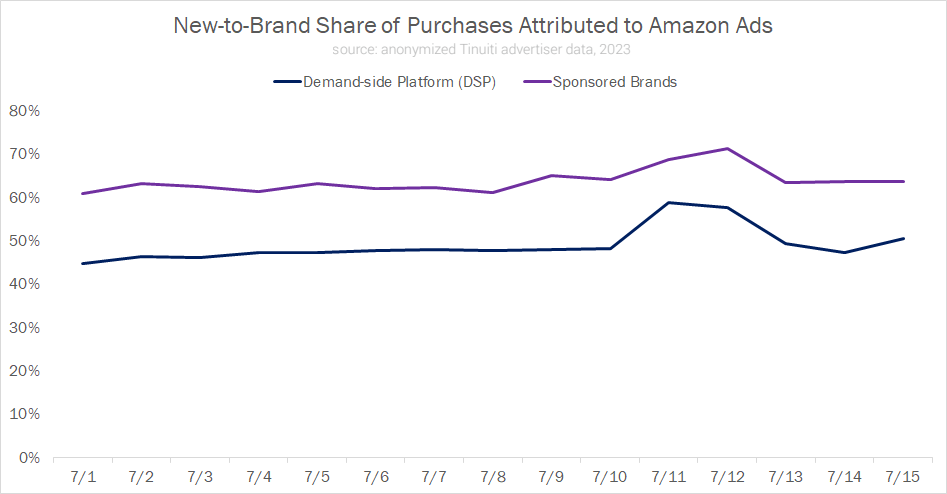

However, these shares are lower than the highs observed over July Prime Day, during which new-to-brand share hit 70% for Sponsored Brands advertisers and 59% for Amazon DSP advertisers.

As such, it does appear that the July Prime Day event is more likely to attract new customers for advertisers, but that advertisers can still expect a bump in new-to-brand share during fall Prime member events.

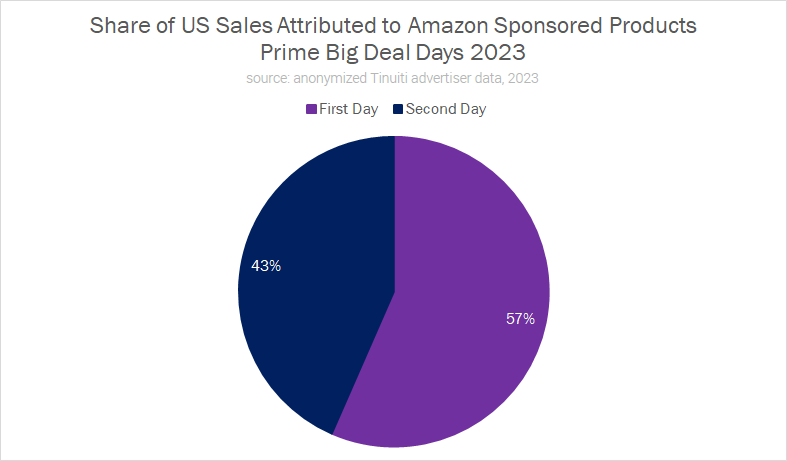

Looking at sales attributed to Sponsored Products by day, the first day of PBDD accounted for 57% of sales, with the second day accounting for 43%.

This continues a trend observed for years now in which the first day of Prime member events accounts for the lion’s share of sales attributed to ads during the event. During Prime Day 2023, 61% of Sponsored Products sales were attributed to the first day of the event.

While the last 24 hours of these multi-day events is regularly smaller than the first day, the second day is still a huge contributor to advertiser success, and brands should look to remain active throughout the entirety of Prime member sales.

With PBDD in the books, Q4 is now fully underway for Amazon vendors and sellers. Make sure to stay tuned to the Tinuiti blog for more trends and insights as we get deeper into the holiday shopping season.

VP, Research

Andy Taylor is the VP of Research at Tinuiti, where he leads proprietary data research that translates billions in annual ad spend into clear, actionable insights for brands. He lives in Richmond, VA, where he enjoys running, tending his yard, and binge‑watching baking shows.