Media Update: Tubi Q4 Performance, Low NBA All-Star Game Viewership, and Shifting Consumer Demands

Ad-supported streaming video supply continues to hold steady, about 25% above the level this time last year.

Industry Notes (Video)

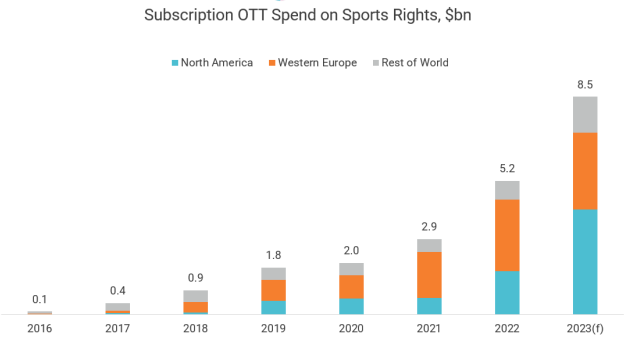

1. Spending on sports broadcast rights for subscription OTT services is projected to exceed $8.5 billion in 2023, a 64% increase over last year. The estimate from Ampere Analysis covers global spend and credits the massive increase to the streaming wars and the decline of traditional channels, such as broadcast and cable.

This should be a familiar narrative to readers of this newsletter, as we frequently discuss the ever growing list of platforms that have brought sports (and the accompanying advertising inventory) to streaming. However, for all this increased investment, spend from streaming companies on sports rights still represented just 13% of global spend and will only reach 21% in 2023. We may be approaching a tipping point in viewing behavior, with major deals for NFL broadcast rights going to streamers Amazon Prime and YouTube TV; but the vast majority of viewing still occurs on linear TV, and broadcast rights are entrenched in linear deals for years to come. | Fierce Video

2. Fox’s Tubi continued to make gains in the fourth quarter, reaching 64 million active users and increasing total viewing time by 44% annually. The platform’s most recent research report indicates that its user base is increasingly diverse, with African American and LGBT audiences growing over 50% in 2022, and viewership increasing over 25% at all major levels of household income. Tubi’s audience also matured in the last year, with its median age now 39 years old. The report also includes a number of surveys and data points that support the rise of ad-supported video on demand (AVOD) as an increasingly popular viewing medium for consumers, who are fatigued by subscription costs. | Fierce Video

Last month we discussed Bally Sports bringing its many regional sports networks (RSNs) back to FuboTV just six months after developing its own DTC platform. Underlying that move was acute financial woes, which are coming to a head right now. For a bit of context, Bally Sports is the new name of the Fox Sports RSNs that Sinclair Broadcast Group acquired in 2019 when Disney bought Fox’s other entertainment assets. In the transaction, Sinclair acquired the RSNs for $10.6 billion, which included about $8 billion in debt. Without diving too deep into the minutiae of the company’s financial position, Sinclair’s subsidiary Diamond Sports is facing bankruptcy after announcing that it would not make a $140 million interest payment on its debt. It is in an untenable position with negative cash flow and no clear path to profitability in the near term.

Diamond Sports/Bally Sports Networks have faced a perfect storm of challenges: the acceleration of cord cutting, a pandemic that shut down professional sports for an extended period, and exclusion from vMVPDs like YouTube TV. Essentially, revenue from carriage fees is being squeezed as pay TV subscriptions plummet, but RSNs can’t find a home on virtual bundles because vMVPDs still need to undercut the cable bundle (and RSN carriage fees are pricey). This issue is what led sports-centric Fubo TV to part ways with Bally Sports in 2020.

The upshot of all of this is that if Diamond files for bankruptcy, leagues like the MLB could take control of local broadcast rights and deliver local sports DTC in addition to partnering with big broadcasters like Comcast and Charter. While this might be a temporary fix while Diamond restructures, removing the exclusivity of these rights could have profound effects on the role of RSNs and the cable bundle in general. For example, if the RSNs don’t have exclusive broadcast rights, they might not be included in the cable bundle, which in turn could make cable cheaper and more competitive with vMVPDs. There are many moving parts in this story, as is to be expected when the largest network of RSNs nears bankruptcy, and it might still be the case that the old model stays in place. Regardless, the result of this unfolding saga will have a significant impact on televised sports and potentially on the broader cable bundle. | Stratechery

Broadcast networks, general entertainment, and Spanish language all remain well below last year’s level. News viewership has come back down from last week, while sports viewing has moderated somewhat yet remains higher than last year.

Industry Notes

1. The NBA All-Star Game drew an incredibly disappointing audience on Sunday – the smallest in the history of the game – averaging 4.59 million viewers across TNT and TBS. That’s far below the previous low of 6 million in 2021. Lacking competition and star power (Steph Curry, LeBron James, Kevin Durant, and Giannis Antetokounmpo were all injured or left early), the game was an offensive showcase with a ridiculous 184-175 score. Nuggets coach Michael Malone even went as far as to call it “the worst basketball game ever played.” Viewership for the All-Star weekend was down double digits in all events, with the exception of the Celebrity Game on ESPN, which increased 8% over last year to 1.4 million viewers. Despite the poor showing this weekend, regular season viewership on TNT is actually pacing at its highest level in four years, averaging 1.4 million viewers. | SMW

2. Continuing with basketball, the men’s college hoops regular season is drawing to a close, and viewership numbers point toward a favorable March Madness audience turnout. The NCAA Men’s regular season is averaging 7% greater viewership than last year and national TV spend is up a steep 22% across networks. Impressions increased by one billion this season, equating to nearly $100 million in advertising revenue. March Madness is the primary revenue driver for college basketball with over $1 billion in national TV advertising revenue, as it is a solid opportunity for major brand campaigns. | Media Post

1. With Twitter having cracked the door to charging users for social media, Meta is now taking the opportunity to offer paid subscriptions for verified accounts on Facebook and Instagram. In addition to verification, the main features of the paid product include enhanced security features, access to dedicated user support, and increased visibility and reach; the latter feature in particular suggests the offering is geared mainly to content creators, one of the major planes of competition in the social media landscape. There is, as yet, no detail on whether and how paid subscriptions will influence those users’ ad experience; with Snap, Twitter, and Meta now experimenting with subscriptions, advertisers (and the platforms that depend on them) have to grapple with the issue that paid subscriptions will generally skim off the least price-sensitive users, walling off the users many advertisers most want to reach. Testing of the service will begin in Australia and New Zealand this week, with U.S. rollout coming in the next few months. | WSJ, Bloomberg

2. You may recall that Roku sent shivers through the industry with its Q3 earnings report last November: growth was slowing and revenue contracting as advertisers pulled spend amidst macroeconomic uncertainty. Although not the first to report soft growth numbers (Google and Meta preceded Roku on the digital front), Roku’s forecast was a sober reminder that the industry might be facing an “advertising recession.” Fast forward to last week – Roku has reported that it saw better than expected earnings in the fourth quarter, beating its lowered expectations. In particular, ad spend beat the overall ad and traditional TV markets in the United States. To be clear, Roku is still suffering from a decline in growth in its platform segment, growing just 5% YoY this quarter versus 15% in Q3, 26% in Q2, and 39% in Q1. This is most certainly due to the weak TV ad market, which may be slowing its descent in 2023

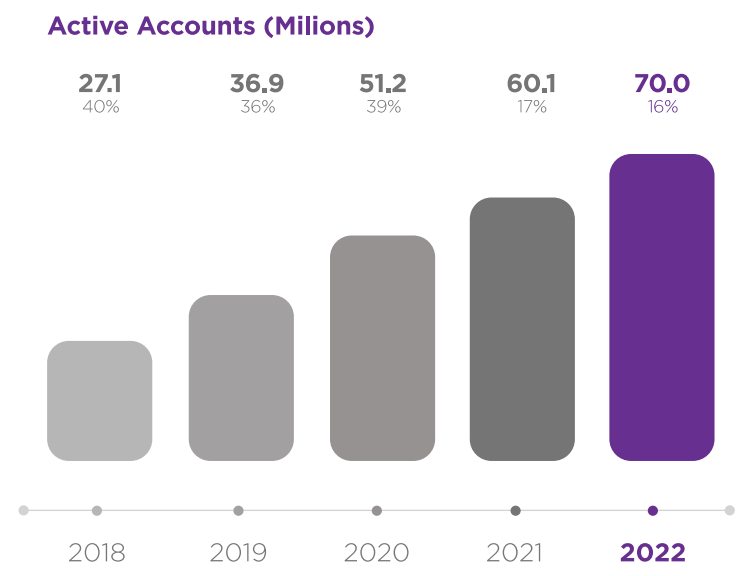

On the bright side, Roku recorded another year of steady growth in its active accounts, adding 4.6 million in Q4 to bring the global total to 70 million. But Tubi is hot on its trail with 64 million accounts, and despite the consistent and impressive growth of free ad-supported TV (FAST) viewership, the addition of several new ad-supported offerings, such as Netflix and Disney+, could present a challenge in the form of increased competition for advertiser dollars. | WSJ, Variety

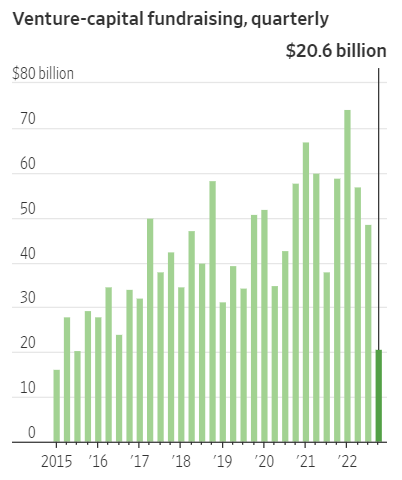

3. As technology valuations have imploded over the past year, one of the major correlates of tech value has imploded right alongside – venture capital fundraising has plummeted recently, reaching a level in Q4 last seen in 2013. To avoid confusion, note that this refers not to funding, i.e. money committed to startups, but fundraising, i.e. money committed to venture capital funds by limited partners (pension funds, endowments, etc.).

The reasons for the downturn in capital allocation to venture capital are not difficult to discern. First, the rapidly falling valuations of public technology companies drag down “comps,” i.e. what comparable companies are valued at and thus what private technology companies can hope to achieve at exit. Second, the Federal Reserve’s rate-raising program of the past year is explicitly designed to take capital out of the economy (e.g. by parking it in bonds rather than investing it in startups). Third (and related to both previous points), expectations of the interest rate path have increased dramatically over the past year:

Since many startups are at least a few years away from significant cash generation, higher interest rates mean much higher discount rates on future cash flows, depressing current valuations.

So why is this a story about the ad economy? Because many startups spend a lot of the money they raise buying advertising. Some estimates place the rate as high as 40 cents of every VC dollar going to Google, Facebook, and Amazon. So to the extent venture funds are raising less money and deploying less capital, a significant source of demand for the major ad platforms may be drying up for a while. All else equal (and let’s not reason from a price change!), this would seem to dampen demand and remove some upward pressure on the price of digital ads, which have crept ever upward in recent years. | WSJ

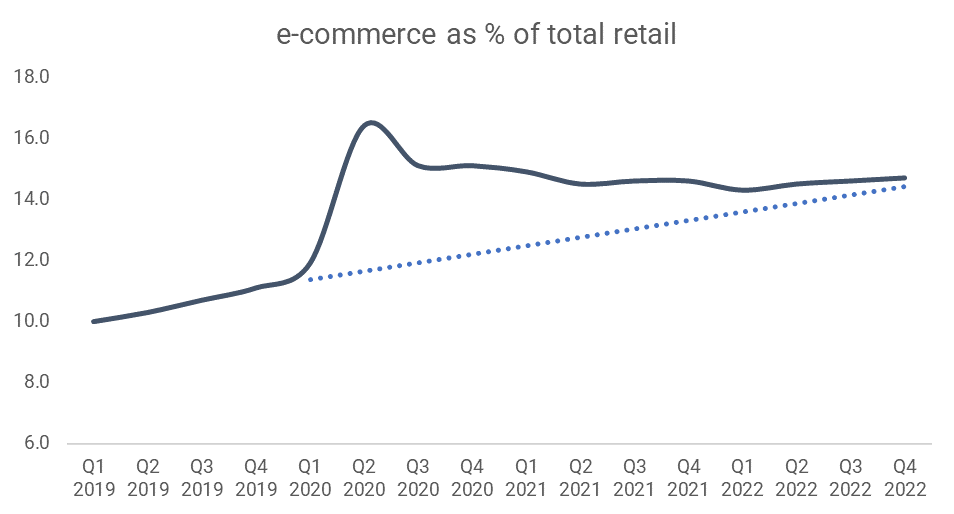

1. Following several years of consistent growth, ecommerce’s share of total retail flatlined in 2022, as post-pandemic adjustments in consumption patterns failed to favor online merchants.

The average share for 2022, at 14.5%, was actually slightly lower than in 2021. Notably, the Q4 2022 rate of 14.7% is almost exactly what it would have been had pre-pandemic penetration growth continued in a linear fashion for the past three years (see dotted line above). For e-commerce merchants, the glass-half-full perspective is that penetration has increased by 3.5 points in the past three years; the glass-half-empty perspective is that shipping rates are about 25% higher, and many online merchants overbuilt capacity during the pandemic, which has been very expensive to unwind. | The Information, U.S. Census Bureau

2. Another important bellwether of the online economy is Shopify, which posted healthy ~25% YoY revenue growth, yet disappointed investors with forward guidance signaling caution. The company said it’s expecting “high teen percentages” growth in the first quarter, which is inclusive of across-the-board price increases the company has implemented. An equity analyst said the company’s outlook “… suggests a slowdown in transaction volume … it appears that management is assuming a deceleration in economic activity.” | Bloomberg

3. On the retail side, both Walmart and Home Depot are reporting that consumer demand for apparel, electronics, and home improvements is declining in favor of food and travel. Home Depot is projecting roughly flat sales and a decline in profit in 2023, citing a decline in DIY customers, a segment that boosted sales during the pandemic. Similarly, Walmart made revenue gains last year, posting 8.3% sales growth in the quarter ending January, but is cautious about 2023. The general consensus from retailers is that the economy is still moderating from the pandemic boom, and that consumers will continue to cut spending on non-essential goods in favor of services. | WSJ