Media Update: TV Usage Stats, CFB Viewership Soars, Google Experiments

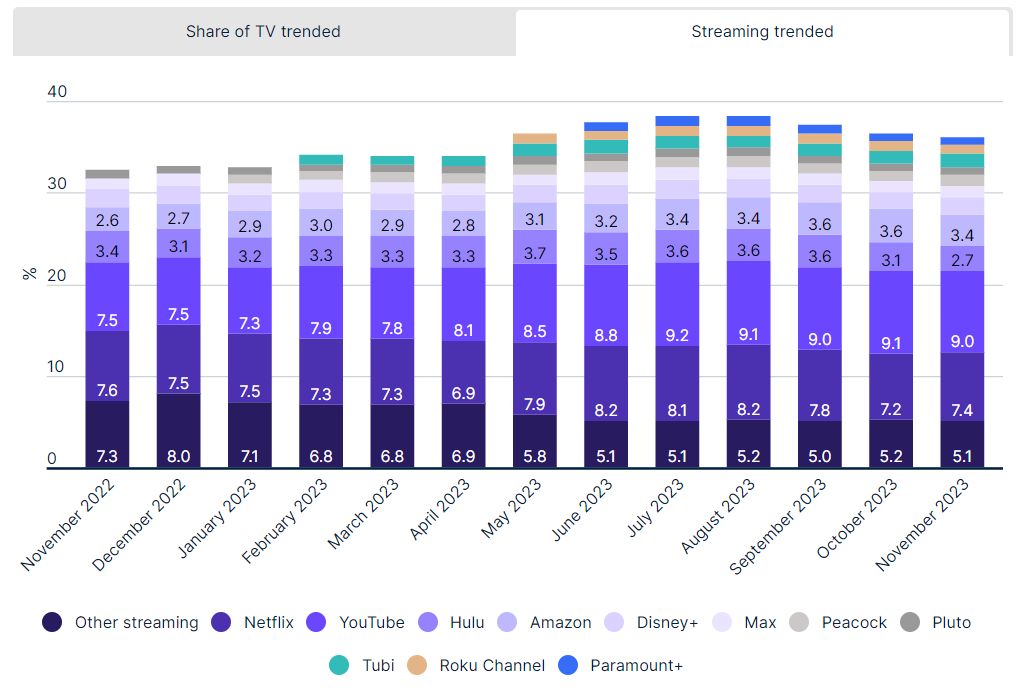

Ad-supported video supply has been somewhat volatile over the holidays, but remains on a clear upward trend over the past several months.

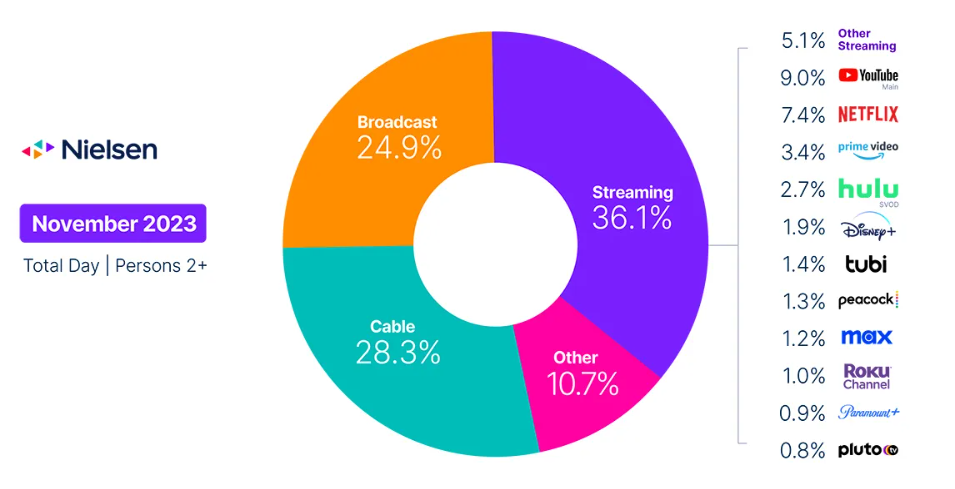

1. Total TV usage rose by 5.7% in November, with broadcast’s share increasing for the fourth consecutive month, peaking during Thanksgiving week. This surge was driven by significant college football rivalries and an expanded NFL lineup, leading to an 18.4% rise in broadcast usage and a 21% increase in sports programming viewership. While overall broadcast viewing dipped year-over-year, sports viewing on broadcast channels grew by 2.8%. Cable saw a 26% rise in holiday movie viewership, overtaking cable news as the top genre. However, cable’s overall share dropped due to declines in news and sports viewing.

In streaming, a 4.3% increase didn’t prevent a half-point share loss, despite gains from Peacock and Netflix, the latter buoyed by the miniseries All the Light We Cannot See.

2. We told you last time about Netflix’s viewing data dump, and the implied dare it contained to its streaming rivals to keep hoarding (and thus under-monetizing) their content. In Netflix CEO Ted Sarandos’ words,

“As the competitive environment evolves, we may have increased opportunities to license more hit titles to complement our original programming. We believe this will deliver additional value for our members (i.e., engagement), as well as for rights holders who benefit from the increased awareness and revenue that Netflix delivers, in addition to the new life that success on Netflix can drive.

Translation: don’t be stupid, take the money, and get your expensively-produced content seen by more viewers.”

This now seems to be happening in fairly short order; though to be clear, licensing never really stopped, it just slowed way down as entertainment executives confronting a new landscape felt that licensing to Netflix was “selling nuclear weapons technology” to a powerful rival. In the coming months, Disney, Paramount, and Warner Bros Discovery will all license major titles to Netflix, injecting cash into their strained balance sheets and fueling Netflix’s algorithmic machine with even more content. Films like Dune and Prometheus, as well as shows like Young Sheldon, This Is Us, How I Met Your Mother, and Lost will all be landing on Netflix in the coming months.

As we’ve often discussed in these pages, it makes no sense in the long run to have a large number of vertically integrated content production and distribution players; the entertainment industry has not worked that way in the past (independent studios have always been part of the model), and nothing about the internet changes it (if anything, it pushes in the other direction). What seems much more logical is a small number of vertically integrated players, augmented by a larger number of content producers who sell to the highest bidder; in other words, the same model as always! But with different names this time, and Netflix sure to be one of them. Watch for more consolidation to come in 2024. | NY Times

3. Speaking of consolidation … Warner Bros Discovery and Paramount Global are reportedly discussing a mega-merger. A deal would combine significant Hollywood and cable assets, including Warner’s CNN, HBO, and streaming service Max, with Paramount’s MTV, Nickelodeon, Comedy Central, CBS broadcast network, and Paramount+ streaming service.

The rationale for a merger (and indeed, the rationale for the 2021 deal combining Warner Bros and Discovery) centers on the growing necessity for media companies to expand their scale to remain competitive. As a benchmark, Netflix has about 250mm global subscribers; that means it can amortize its $17b content budget across those users, spending about $68 per user. By contrast, Max has about 96mm global subs, and Paramount+ has about 63mm; this means Netflix has 3x – 4x greater leverage over its fixed costs, putting it at a major advantage when it invests in content. Hence the logic in combining WBD and Paramount.

Such a merger would face many challenges, including regulatory scrutiny and WBD’s existing debt from the 2021 Discovery-WarnerMedia merger. Additionally, the cable network aspect of the deal (both parties own significant cable assets) is less appealing due to the decline in traditional cable viewership.

Consolidation would likely lead to significant cost synergies and staff reductions, fitting the parsimonious environment in Hollywood the last couple of years. | WSJ

4. Yet more on the logic of consolidation and bundling … as more major streaming services have introduced ads and raised their prices in order to stem the flood of red ink their new offerings have generated, consumers are responding in a predictable manner: 6.3% of major streaming service subscribers canceled in November, an increase from 5.1% a year earlier. About a quarter of U.S. subscribers have canceled at least three services in two years, a marked increase from two years ago when that rate was about 15%.

Faced with the need for profitability and the high cost of reacquiring customers, streamers are experimenting with various retention strategies. These include introducing cheaper, ad-supported tiers; bundling services for discounts; and offering promotional rates. Interestingly, data from Antenna suggests a high resubscription rate, with up to half of the customers returning within two years. Ad-supported plans are emerging as an effective tool to attract new and returning customers seeking lower-cost options.

As we’ve dwelt on ad nauseam, bundling is a central part of the story here. Companies like Verizon are offering bundled deals, and platforms like Warner Bros Discovery recognize bundling as a crucial part of the future strategy. The Disney bundle, for example, has shown lower cancellation rates than its standalone services, supporting the logic of bundling as an effective approach to customer retention. | WSJ

Linear viewing trends are a little wonky for sports networks. This year’s college football semifinals (more detail below) took place on January 1st, while last year’s semifinals took place on Dec 31st. This is why you see a big YoY dip in the week of the 25th and a big YoY spike the week of the 1st. Other programming genres continued their downward YoY trends, apart from the broadcast networks which benefited from strong NFL viewership the week of Christmas.

Industry Notes

1. We’ve often discussed the trend toward linear TV becoming an ever more sports-dominant medium – in 2023, the top 14 telecasts, and 44 of the top 50, were sports programming, with the NFL way out in front.

This is why major sporting events, like the college football playoffs, are so highly anticipated by broadcasters and advertisers. And the New Year’s Day games delivered some reasons for cheer – the two CFB semifinals on the 1st averaged 22.6 million viewers, the highest average since 2017 and third-highest in the decade since the new playoff format was introduced.

The pick of the matches was the Rose Bowl, which averaged 27.2 million viewers, the largest college football audience since the 2018 national championship game and second-largest since the inaugural year of the playoff in 2015. The Rose Bowl benefited from a matchup of two glamor teams – perennial powers Alabama and Michigan – and the more favorable timeslot, kicking off at 5pm ET. On top of that, the game itself was a barn burner! The peak audience for the game was 32.8 million, a 21% increase over last year’s TCU – Michigan semifinal.

The other semifinal was the Sugar Bowl matchup between Texas and Washington. The game delivered softer audience numbers, averaging 18.4 million viewers, down 18% from last year’s comp and the least-watched semifinal to date. The game’s audience was undermined somewhat by a worse kickoff time (9pm on the East Coast) and a somewhat less glitzy matchup (sorry Husky fans … at least you won!). But it too was a classic, coming down to the very last play of the game.

This year marks the end of the four-team CFB playoff format, with an expansion to twelve teams commencing next season. | SMW

2. Another football game that drew a lot of eyeballs was a Monday Night Football game that actually took place on a Saturday. The special Saturday edition, featuring the Dallas Cowboys and the Detroit Lions, averaged 25.66 million viewers, ranking as one of the highest regular season MNF audiences since 1997. As we’ve frequently noted, matchups really matter in driving audience interest, and the Cowboys in particular are catnip to NFL viewers; an exciting game, coupled with a very controversial Cowboys win, also contributed to this high viewership. MNF is now averaging 17.1 million viewers this season, up a third from last year and the first season in 20 years to average an audience of that size. | SMW

3. The second season of NFL Thursday Night Football on Amazon Prime Video notched significant viewership gains, growing by 24% to average 11.9m viewers. The double-digit YoY growth is significant, although the 11.9m average still falls short of the 12.9 million from two years ago when TNF aired on FOX and NFL Network.

Growth was somewhat slower in younger adult demographics, and the audience’s median age increased slightly, from 47 to 48.5 years old. This is still quite a bit younger than broadcast NFL audiences (55) or primetime broadcast TV (62). Female viewership notably outpaced overall growth, rising by 30%.

Both Amazon and the NFL knew they were going to take an initial audience hit when TNF went streaming-only, and they accepted this as part of the investment in the sport’s streaming future. Such significant growth from the first to the second season will be very encouraging – now they just need better matchups than some of the stinkers TNF has had this year (Panthers – Bears anybody??). | SMW

As you’re undoubtedly aware, we’re mere months away from the last gasp of the third-party cookie – the building block of internet advertising for three decades – when Google will fully deprecate 3P cookies from the Chrome browser. Indeed, as of the 4th of this year, Chrome has already taken a meaningful step by blocking cookies on 1% of Chrome browsers in order to allow for testing of its new Privacy Sandbox APIs.

The public reaction to Privacy Sandbox testing has been markedly skeptical. The Trade Desk – a longtime champion of the open web – has been particularly critical. Their concern is that the Privacy Sandbox might obscure vital identity data, complicating cross-device advertising coordination, and impacting ad performance measurement and optimization. TTD’s own solution, Universal ID 2.0, seeks to address these issues by gathering data with user consent, a radically different approach from the user-cohorting model underlying Google’s post-cookie architecture.

Google has, unsurprisingly, pushed back forcefully on the criticisms. In a recent blog post, the company emphasized that the Privacy Sandbox’s aim is to balance privacy with economic functionality. It’s a response to the growing demand for consumer privacy, intending to obscure individual user data through aggregated information, without stifling the online economy. Google asserts that its approach, which includes APIs to replace cookies, is a significant step towards privacy without compromising the effectiveness of digital ads.

Regulatory scrutiny adds another layer to the debate. The U.K.’s Competition and Markets Authority, for instance, is closely monitoring Google’s moves to ensure a balance between privacy and industry competition. For those of you who see that as a potentially insoluble tension … it is!

With under six months left in the life of the cookie (unless the competition authorities force a stay of execution), we can expect a lot more debate from interested parties. But the brute fact is that Chrome has a ~49% share of the U.S. market; any advertisers wishing to reach those users will have to play by the Privacy Sandbox rules. | AdAge

1. We’ve been on the inflation beat for coming up on three years now, ever since the spring 2021 outbreak of the worst price inflation the U.S. had seen in 40 years. In that time the news has generally been pretty grim – with fiscal deficits as far as the eye can see, and no indications of any change in the fiscal path, many analysts predicted huge difficulties for the Fed in unwinding the most rapid increase in the monetary base since records began.

Happily, those analysts seem to have been too pessimistic – November witnessed the first MoM decline in prices since April of 2020, and YoY inflation for the month was 2.6%, within striking distance of the Fed’s 2% target.

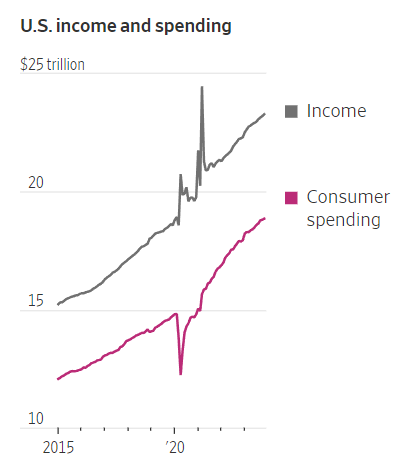

Encouragingly, the U.S. economy has sidestepped a widely predicted recession, largely thanks to surprisingly resilient consumer spending in the face of disinflationary policies (i.e. large interest rate increases). This so-called ‘soft landing’ scenario, where inflation aligns with the Fed’s target without triggering a recession, appears increasingly likely.

Consumer spending and personal income have also seen a rise, further signifying economic confidence. This consumer behavior, coupled with strong labor market performance, indicates a balanced recovery where wage increases don’t excessively fuel inflation. | WSJ

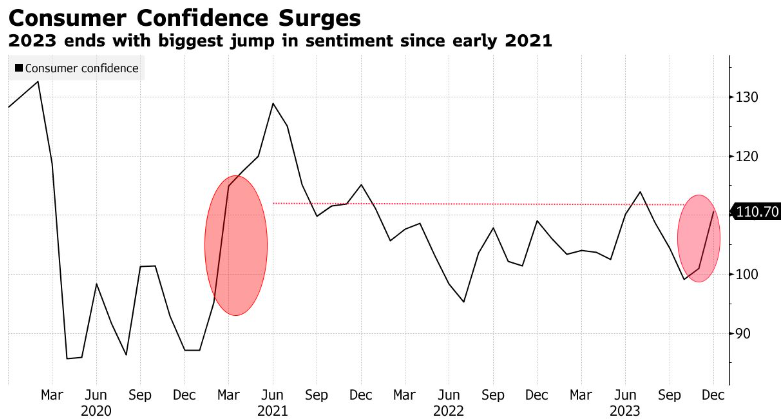

2. In a development that is almost certainly linked to the aforementioned inflation news, U.S. consumer confidence rose in December by the most since early 2021, as sentiment improves regarding both the labor market and the inflation outlook.

The optimism extends across multiple economic dimensions, including current business conditions and future income. Americans’ plans for major purchases and vacations are on the rise, signaling robust economic engagement going into 2024. Despite ongoing concerns about inflation, it’s noteworthy that worries about politics, interest rates, and global conflicts have diminished.

Improvements in labor market sentiment are particularly striking, with a notable increase in the number of consumers perceiving job availability. Additionally, the expectation of lower interest rates and a decreasing perceived likelihood of a recession in the near term highlight growing optimism about the economy’s trajectory.

Score another point for team #SoftLanding. | Bloomberg

3. The other key macroeconomic data point is the labor market, which seems to be cooling (but that’s broadly perceived as a good thing in context). In November, US job openings declined to their lowest level since early 2021; the drop to 8.79 million vacancies, along with fewer voluntary quits and a decrease in hiring to April 2020 levels, suggests a shift in labor demand.

Key sectors like transportation, warehousing, government, and leisure saw notable declines. This easing might reassure the Federal Reserve, as it could reduce upward wage pressure and slow inflation.

In broader context, the labor market remains extremely healthy. November unemployment was 3.7%, which is extraordinarily low by historical standards; labor force participation was 62.8%, which is just fractionally below where it was pre-pandemic; and the number of unemployed persons per job opening is 0.7, which is extremely low (for context, that figure was about 6.5 immediately following the 2008 financial crisis). This underlying health is sustaining consumer spending, and ultimately allowing for a much less painful correction to the economic dislocations of ‘20 – ‘21.

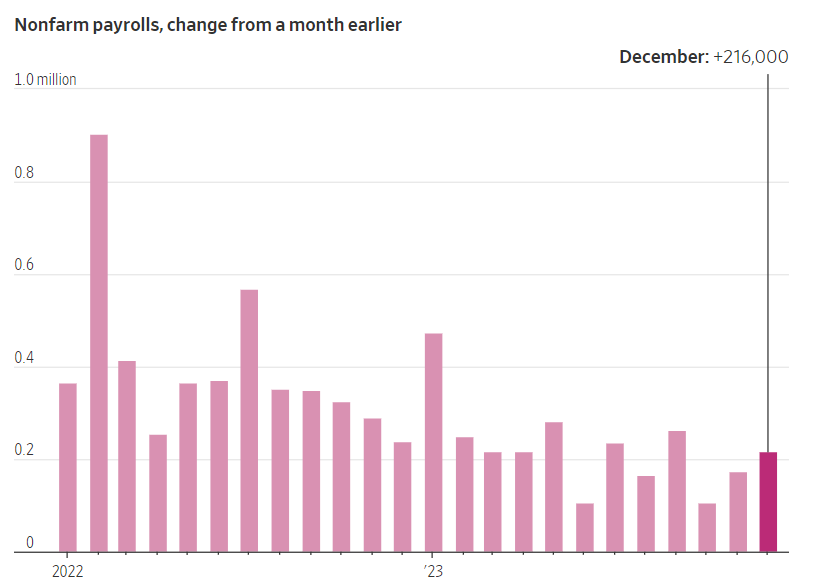

UPDATE – Those indications of labor market cooling may have been premature. December hiring figures are now in, and they show 216k jobs added last month, well ahead of most analysts’ forecasts. The unemployment rate held steady at 3.7%.

The rude health of the labor market is undoubtedly good news. It has, however, complicated the Fed’s calculations somewhat: weaker job figures would have made interest rate cuts, which numerous sectors are clamoring for, a more straightforward decision. But with the labor market as strong as it is, reducing rates would now seem to carry more risk of premature monetary easing. | Bloomberg, WSJ