Media Update: Election-Driven CTV Spend Surge, Snap's AI-Powered Spotlight, and Google Faces Antitrust Pressure

We’re now in the home stretch of the political season, with fewer than seven weeks to go until election day. Unsurprisingly, news viewership remains strong, with a huge audience increase the week of the 9th as over 67M viewers tuned in to watch Kamala Harris debate Donald Trump. That figure is a substantial increase from the 51M who watched Trump debate Joe Biden in June, though it is a bit below the marks from the past two cycles’ debates. Broadcast has also benefited from the start of the NFL season, which set a week-one viewership record with an average of 21M viewers per game.

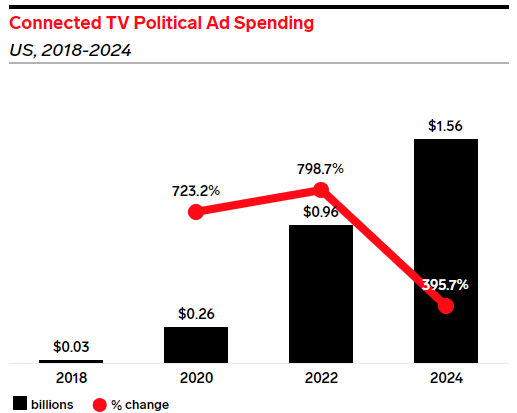

1. Election years are essentially synonymous with TV advertising. As seen above, a presidential race draws massive attention from all corners of the population, and naturally, the campaigns follow by pouring dollars into the ad market to grab any incremental votes possible. In the 2020 cycle, traditional linear TV received north of $6B of political spend, and 2024 is likely to see an increase of ~8%, per a projection from eMarketer. However, the big change compared to prior cycles is the growth of streaming as a medium for political advertising. A non-factor as recently as the 2018 midterms, it has exploded in the last few years, with CTV expected to go from ~$260 million in the 2020 cycle to $1.56 billion this year.

This huge growth has made CTV a major factor in the political ad economy, with it now accounting for almost half of digital political ad spend and ~13% of total political ad spend. There are many causes for this increase – the rapid growth of streaming’s audience as well as expectations that digital tools, like frequency capping and audience targeting, will help campaigns more efficiently reach viewers. To illustrate that point, the Harris campaign recently announced a $200M+ ad buy across digital platforms including Hulu, Roku, YouTube, and Paramount (as well as audio platforms such as Spotify, which began allowing political ad spend again in 2022 after pausing in 2020).

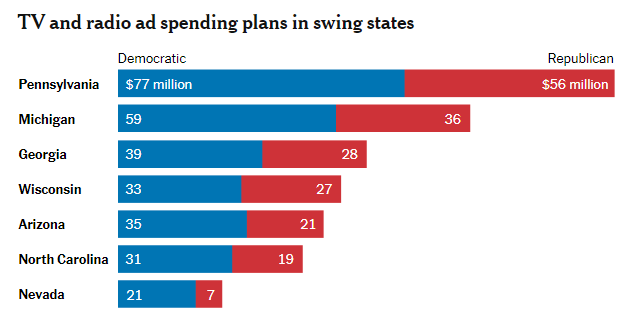

Though this growth has been dramatic, it has also been targeted. Spend has been heavily focused on the major swing states of the presidential cycle, as the latest buys from September reflect.

This shift towards CTV creates a dynamic environment that non-political advertisers will have to navigate. On streaming, some variable CPMs could see increases of 15-50% in battleground states, while increases of up to 75% are possible on certain pockets of linear. The Tinuiti team has been well aware of this dynamic, and has both taken actions to safeguard against cost increases and shared guidance with affected advertisers on necessary next steps. Specifically, we access the majority of our CTV inventory at pre-negotiated rates which are not subject to the projected cost increases, and we encourage national linear advertisers to book on a slightly advanced cadence to ensure successful delivery. We only expect major impacts to true-local linear advertisers, for whom we have advised an accelerated booking schedule and a shift towards cable inventory, where network diversity is plentiful and cost-effective opportunities remain. Overall, these changes in the political ad landscape are a harbinger of a new era for media, but one that advertisers can be well-prepared to meet. | NYTimes, eMarketer

2. DirecTV customers’ sports and entertainment nightmare has come to an end – the service provider announced Saturday that it had reached an agreement with Disney to bring its channels back to air after a two-week interruption. As we discussed at length in our last update, the two sides were at odds over the carriage fees Disney charges DirecTV for its programming and the requirement that its channels be included in many subscribers’ packages. The new agreement between the media companies maintains “carriage at market-based terms”, though some DirecTV customers will now be able receive Disney+, Hulu, and ESPN+ directly through their DirecTV package. While financial terms were not disclosed, expectations are that this new agreement will, unsurprisingly, be financially beneficial to the House of Mouse. For advertisers, this is a very positive development, as it means DirecTV’s 11 million customers are once again part of Disney’s linear audience, returning ads placed there to normal efficacy.

Though the dispute has ended for the time being, a resolution that seems largely favorable to Disney and that prioritizes making streaming platforms available to consumers is a clear knock on linear TV’s standing. Audiences continue to move away from traditional satellite mediums and into streaming platforms, threatening DirecTV’s long-term viability. Perhaps not coincidentally, Bloomberg reported last week that DirecTV and Dish are in the early stages of merger negotiations. With the news breaking late Friday, both Dish parent EchoStar and DirecTV parent AT&T saw their stock values jump at Monday’s open.

While this could be subject to regulatory concerns over the resulting 20 million subscriber combination, it represents the most obvious path forward for linear providers facing the massive pressures of a changing audience. For now, no changes are expected, but should this deal proceed to completion, it could help preserve some of linear carriers’ negotiating ability with publishers. | NYTimes, Bloomberg, CNBC, CNBC

This week Snapchat announced a range of new updates to its platform, some of which give a glimpse into what is to come for advertisers in the future. One of the biggest platform shifts came by way of a new Spotlight page, which features a full-screen feed of recommended content, very similar to the feeds of Facebook, Instagram, and TikTok. Advertisers are already able to buy this inventory today with existing ad units. Snap’s shift to providing an AI-powered feed instead of a reliance on followership will likely be a welcome addition for users with public profiles, as well as for brands looking for more efficient CPMs. In addition to the updated user experience, Snap also showcased new AI tools that require fewer inputs and offer faster outputs.

While it’s not groundbreaking, it will be another welcome change for users, and sits on the heels of multiple AR and AI innovations that Snap is rolling out. For marketers and developers alike, Lens Studio will now feature “Easy Lens,” which is a turnkey solution for building new AR lenses by simply by plugging in a prompt in Lens Studio or tapping into an existing template for easy generation. This new innovation will make it easier than ever for brands to develop their own AR experiences to engage with consumers.

Additionally, developers will have the opportunity to develop branded apparel and accessories for Bitmoji so that users can sport their favorite brands on their Bitmoji and share with friends. These brand partnerships are not new, with the Valentino example above coming at a cost of $1 – $10 last November, but this is the first time that Snap has fully opened up the development capabilities that the likes of Crocs (featured above) and Prada have already tapped into.

Lastly, we need to mention the latest generation of Spectacles. They feature a built-in screen with a wider field of view, an expanded library of applications, and their first ever owned operating system, Snap OS. This is a big deal for Snap as it aims to stand out amongst other technology companies and establish itself as more than just a social platform.

Today, Spectacles are only available to developers on a monthly subscription model, and there is no timeline for when or if they will become available to consumers. Despite this, brands like Lego and Luicasfilms have already gotten involved by creating immersive experiences for brand fans. For brands already leaning into AR on the Snap platform, this presents even larger future opportunities for how consumers can connect with your brand and product prior to, and even after, becoming a customer. The latest iteration of Spectacles marks the fifth generation of the product, which was first released in 2016. With future generations likely to come, Snap is relying on developers to help further build out the application library so a future consumer launch will be more successful. | Social Media Today, Snap Inc., Snap Inc., Vogue

The connected TV OS space could welcome a new player as The Trade Desk (TTD) is reportedly gearing up to enter the marketplace next year, a move confirmed by AdAge and initially reported by Lowpass. The move would affirm the company’s aspirations to be a more prominent CTV player, competing against Amazon, Google, Roku, and Samsung.

The strategic push into CTV isn’t surprising. CTV advertising has been a growth avenue for The Trade Desk, accounting for 40% of its revenue. And with eMarketer projecting CTV spending to reach $44 billion by 2028, it’s clear why TTD has made CTV a primary focus, even dedicating a section to it in its Q2 2024 investor presentation.

However, given the highly crowded CTV OS marketplace, you wouldn’t be alone in wondering why TTD would choose to develop an operating system. The decision boils down to two factors: first, creating its own CTV OS could streamline the programmatic supply chain and provide more transparency – an approach that The Trade Desk has taken in the programmatic space with initiatives such as the Sellers and Publishers 500, OpenPath, and UID2.

The second reason is even more compelling: data. By rolling out its own OS, TTD could harness its own Automatic Content Recognition (ACR) data, reducing its dependence on licensing deals. This move would also provide access to vital device-level data and IP addresses, allowing TTD to preempt signal loss and ensure better addressability across CTV platforms.

Breaking into this saturated marketplace won’t be easy. TTD will either need to forge partnerships with several smaller manufacturers without their own OS or consider acquisitions to make a material impact. With many details still under wraps, this will be a topic we stay close to as it can open up more CTV opportunities for advertisers buying across The Trade Desk. | eMarketer, AdAge, Lowpass, The Trade Desk Investor Relations, PRWeb

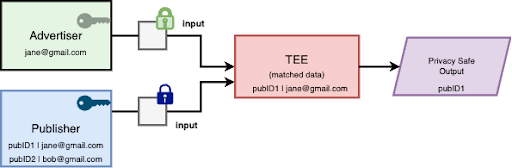

Google announced last week that it is beginning to incorporate a new type of confidential computing, called confidential matching, into its Ads products at no additional cost. This news was a breath of fresh air that was met with resounding positivity within the digital measurement community.

Now used as the default process within data connections made for Google Ads’ Customer Match, confidential matching is a new, privacy-conscious way for advertisers to connect their first party data to Google’s measurement and audience solutions. It provides a user-friendly method for advertisers to match audience data without exposing individual identities by encrypting and processing data within trusted execution environments. Together, these innovations offer improved data security and accuracy for advertisers, while prioritizing user privacy to ultimately enhance trust.

The announcement was particularly welcome news for smaller and medium sized businesses on tight budgets, since confidential matching offers advanced privacy protections without additional costs, technical expertise or complex resources. It removes the need to go through third-party clean room providers, since this is now automated directly within the Google Ads ecosystem.

Google also mentioned that over the next few months “enhanced conversions implemented with the Google tag will start rolling out first-party data processed with confidential matching”. We expect these developments could unlock potential performance gains for Google advertisers who were previously hesitant to fully embrace first party audience solutions like Customer Match and/or Enhanced Conversions due to sensitive data and privacy concerns.

For a deeper dive on what advertisers should know about TEEs, check out Tinuiti’s full blog post. | Google Ads blog, Tinuiti, Search Engine Land

1. Previously we told you that Google was found to have acted illegally to maintain a monopoly in online search, and provided coverage regarding some of the novel scenarios that may await them in the year ahead. While the plans for remediation remain speculative for the moment, we now know the timeline to provide details regarding Google’s punishment will be delivered by August 2025. While the wheels of justice do indeed turn slowly, this trial was just the opening act for Google’s next appearance the following month.

Nothing about this trial has flirted with the possibility of being par for the course. Before the trial even started, it was reported that Google paid the US Department of Justice ~$2.3MM in order to avoid a jury trial. Why $2.3MM? Well, this is the amount in damages that, according to the count, was overpaid on Google’s marketplace by eight federal agencies between 2019 & 2023. An obscure admission of guilt, but it’s clear Google knew its chances of prevailing on these counts would diminish were a jury trial to take place.

The counts that have been leveled against Google, in the most basic terms, accuse it of anti-competitive behavior (be sure to review this article by Digiday if you’d like a deeper dive than this truncated surface scratch) by way of:

It’s important to acknowledge the scope of this trial is focused on the impact of Google’s actions on publishers. While there are many voices within the demand-side (advertiser) community sharing public dissent for Google’s activities, we should note that DV360 and Google’s auction dynamics for advertisers are not on trial here.

While Google has denied all allegations, given their pre-emptive payment for damages combined with the mountains of evidence being presented, many industry voices are suggesting that it’s likely Google will be found guilty on at least some of the counts. For the moment, we shall look to remain impartial and not draw any conclusions, but that hasn’t stopped industry leaders speculating about remediation mechanisms, led by a chorus of voices including the Trade Desk’s CEO, Jeff Green. It’s unlikely there is anyone more excited than Jeff regarding a potential breakup of Google. Of course, it wouldn’t be a modern trial if we didn’t have a great selection of memes being generated:

If you aren’t already a daily follower of this trial, the evidence being presented is akin to a soap opera. The personalities, the conflict, the drama, the egos, the emails all give rise to an incredible story of villains, heroes and a ruthless desire to suppress competition at all costs. One can only imagine the excitement on the faces of Netflix execs as they think about docu-drama content to greenlight for 2025. | NY Times, Business Insider, Digiday, Digiday

2. In an alternate timeline, TikTok’s proposed ban wouldn’t receive second billing, but here we are. Following the bipartisan passage earlier this year of a law that would require TikTok to be sold or be banned, TikTok is finally having its day in court as it argues to continue operating after the law comes into effect on January 19, 2025.

Drawing on examples of other foreign-owned companies such as Spotify (Sweden) and Al-Jazeera (Qatar), TikTok is seeking to argue that it is being unfairly singled out by this law. The point of contention here, of course, is that China is considered by the US government to be a foreign adversary.

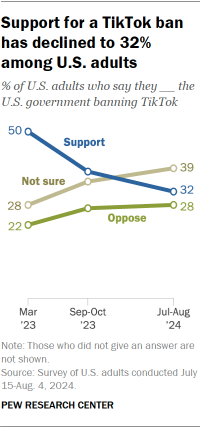

Since the initial passage of the law, when it was reported half of US adults supported the ban, the general sentiment of the public appears to be cooling with the plurality simply not sure if TikTok should be banned – a fitting parallel of US political sentiment in general.

For now, with no acquirer apparent, nor a willingness from ByteDance to divest, TikTok is on the clock, and according to them, the party won’t stop. | NPR, Pew Research

1. As we’ve foreshadowed here for a couple of months now, the Federal Reserve on Wednesday lowered its benchmark interest rate by 50 basis points, the first rate reduction since the spring of 2020. This brings to an end the Fed’s cycle of monetary tightening that began in spring 2022, when inflation became the singular macroeconomic challenge.

The reduction in the Fed’s benchmark rate will cascade throughout the economy, in particular lowering the price of many forms of credit. Mortgages, auto loans, credit card debt, and business loans should all become somewhat cheaper over the coming weeks and months, bringing relief to many sectors that have been struggling with more expensive financing. In addition, the value of any assets that produce cash flows over time – such as fixed income instruments and equities – will, all else equal, become more valuable as the discount rate on those cash flows falls.

The major question now is how much and how fast the Fed might further reduce rates. The market is now pricing in another 70 basis points of rate reductions across the Fed’s two remaining rate-setting meetings this year. Fed officials, meanwhile, are stressing that further rate cuts are not already planned, and will depend on other indicators, in particular the state of the labor market, in the coming months. | WSJ

2. New data from the Census Bureau show American households’ real (inflation-adjusted) income rose last year for the first time since 2019, drawing back level with the all-time peak reached the year before the economic shocks associated with Covid-19.

The pandemic itself was of course a massive negative supply shock – reduced freedom of movement (voluntary or otherwise), closure of national borders, large numbers of people’s health damaged by the virus, and myriad other factors just made the economy less productive. This reality was somewhat papered over by huge increases in fiscal intervention,

And unprecedented monetary easing:

Alas, all that fiscal intervention was just more debt, which taxpayers are ultimately on the hook for; and since money is neutral in the long run, all the monetary stimulus got us was inflation. Where it really matters – households’ ability to consume goods & services – the last few years have been rough. This is fully consistent with what we told you last week, namely that consumer confidence remains well below its pre-pandemic level. | Bloomberg, WSJ

3. Speaking of consumers’ mood, the University of Michigan’s consumer sentiment index rose to a four-month high in early September, aided by lowering inflation expectations and anticipation of falling interest rates.

Notably, a larger share of consumers in the survey viewed unemployment as potentially more worrisome now than inflation, a significant reversal from the norm of the past 24 months. There also seems to be some political contingency in how consumers view the near future – sentiment among Democrats rose in September but fell among Republicans as a growing share of voters from both parties anticipated a win by Vice President Kamala Harris, according to the report. Those downcast Republicans may console themselves by consulting the prediction markets, which have it pretty neck and neck! | Bloomberg