Media Update: YouTube TV Price Increases, March Madness Coverage, and Impact of Layoffs

Ad-supported video supply has continued to tick up in recent weeks, surpassing the peaks we last saw in Q1 of last year.

Industry Notes (Video)

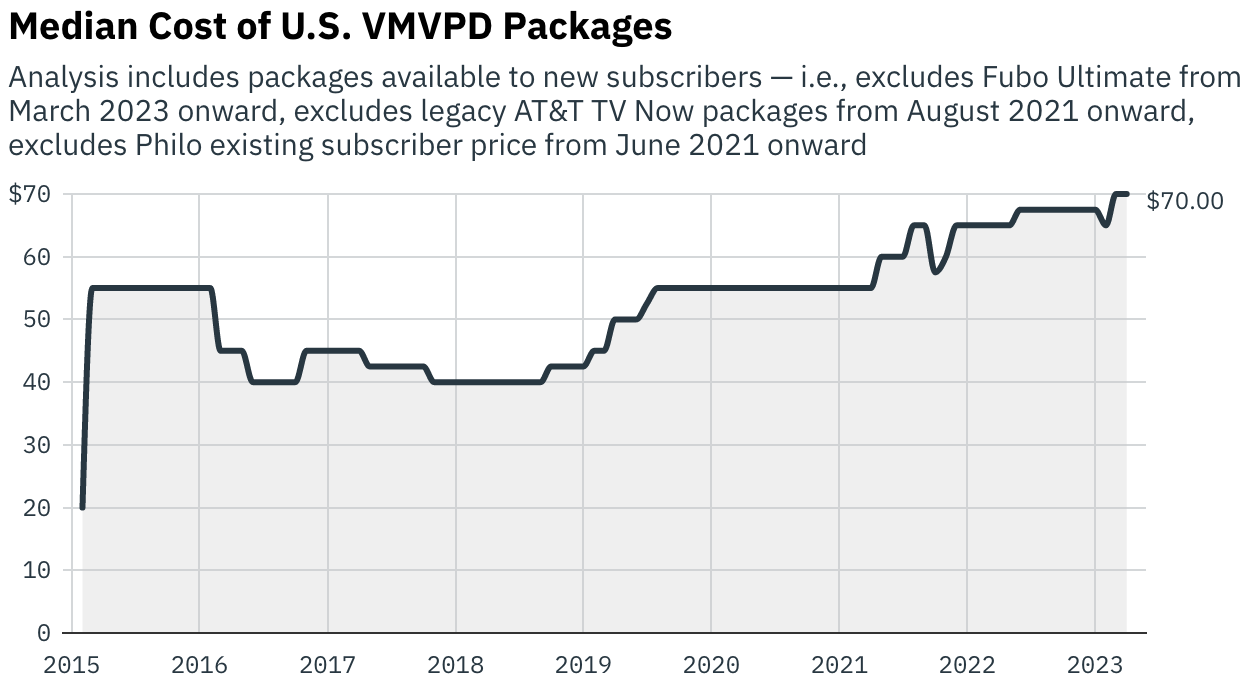

1. Another week, another price hike. Google’s YouTube TV is raising its monthly subscription price by $8, from $64.99 to $72.99, citing rising programming costs after spending more than $14 billion to acquire NFL Sunday Ticket. The vMVPD has yet to announce pricing for Sunday Ticket, but reports have speculated that the service may charge as much as $300 per season for the option. However, it is offering some consolation by reducing the price of its 4K Plus package from $19.99 to $9.99 per month. YouTube TV is following in the footsteps of other vMVPDs like Fubo, Hulu Live TV, and Sling TV, which have also increased their prices recently due to the high cost of content. YouTube TV has over 5 million subscribers and has seen significant growth in recent years, doubling its subscriber base in just over two years. This puts it ahead of competitors like Sling TV with its 2.3m subscribers and Hulu Live with 4m.

Price hikes across the vMVPD sector reflect the challenge that all pay-TV operators face: as streaming services have siphoned off subscribers who don’t care about sports and are mainly interested in general entertainment programming, those subscribers are no longer around to cross-subsidize the cost of pricey sports content. The leading edge of this phenomenon is the meltdown of the RSN business model, but it applies to pay TV more broadly.

It is somewhat ironic that services like YouTube TV and Fubo find themselves charging as much as the services they replaced, but as we have discussed at length, sports rights are more expensive than ever. Offering Sunday Ticket as a separate product (not requiring a full YTTV subscription) is a crafty way for YouTube to maximize revenue and hone its live sports vertical whilst giving consumers more options than traditional cable. As the competition between vMVPDs heats up, streamers will have to focus on creating bundles that match the wide variety of consumer interests, thereby enabling cross-subsidization that works in the new streaming landscape. | Media Post

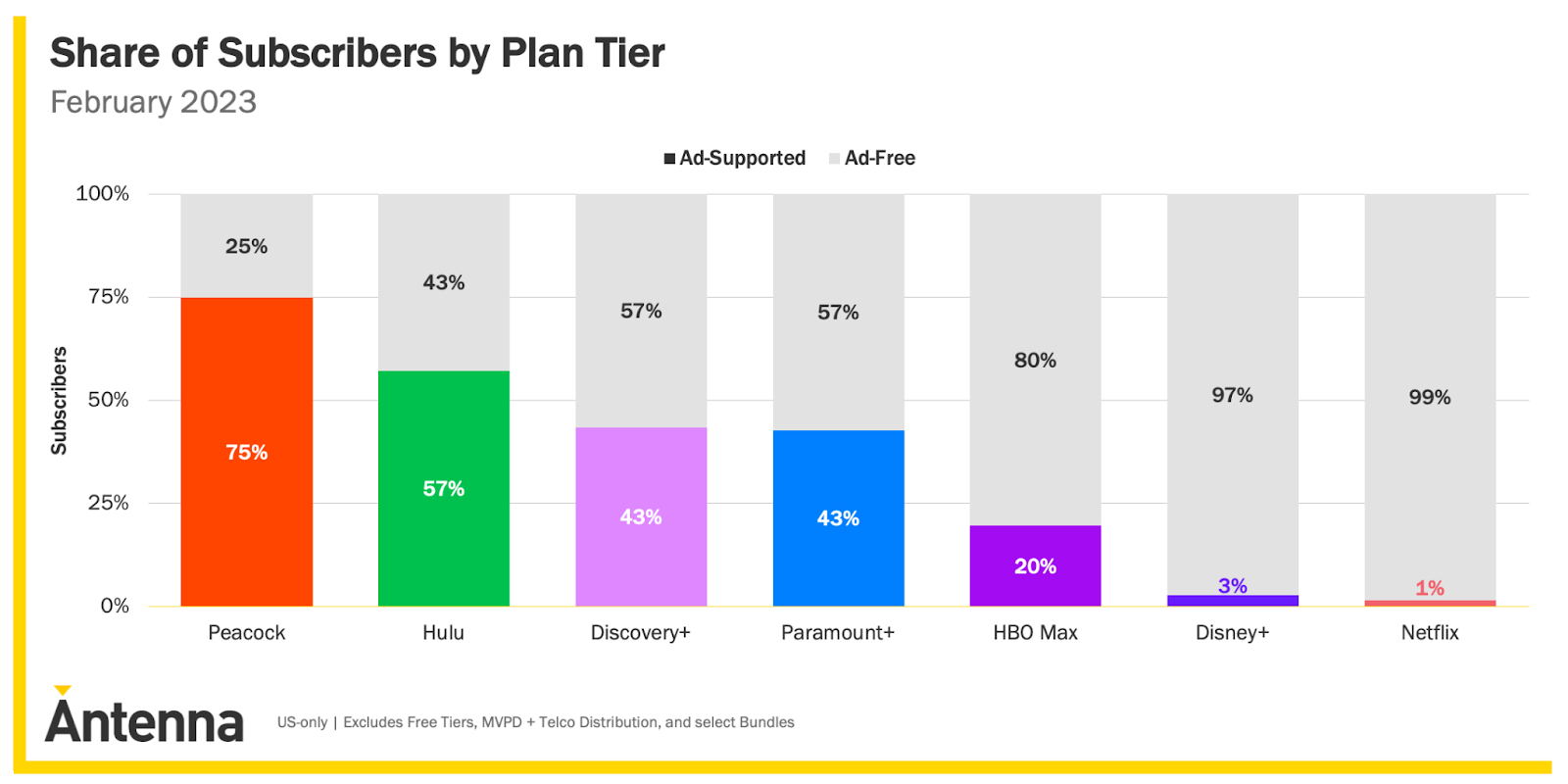

2. When Disney+ and Netflix announced that they would be raising prices and implementing ad-supported offerings, there was well-founded concern that churn would rise. Particularly in the case of Disney+, where the ad-supported tier was assuming the place (in price) of the ad-free tier, analysts were projecting a non-negligible loss. Despite these expectations, 94% of Disney+ subscribers have accepted the platform’s recent price increase with relative equanimity (i.e. without downgrading to a cheaper tier), and its ad-supported video on demand (AVOD) tier is outpacing its rivals in new sign-ups. In February, Disney+’s ad tier (including subs sold as part of a bundle with ESPN+ and Hulu) represented 36% of new subscribers compared with 20% for Netflix and 21% for HBO Max. It was also revealed that Hulu’s ad-supported service is driving growth for the platform, with more than half of new sign-ups opting for the cheaper, ad-supported version. Antenna suggests that Disney+ services are “headed toward accumulating meaningful audiences for advertising.”

This sentiment rings true for Netflix as well: the streaming king surpassed one million ad-supported subscribers, gaining momentum after a slow start in November. Initially, analysts feared that this new tier would lead viewers to downgrade, but most of the people signing up for the ad tier are new customers or lapsed customers. Ultimately, the new ad tier could bring in between 15m and 30m customers in the US – the true test will come as Netflix cracks down on password sharing and forces millions of people to stop using their friends’ account. | WSJ, Media Post, Bloomberg

News viewership remains depressed on a YoY basis (because of the invasion of Ukraine last winter). Sports network viewership continues to show buoyancy, while Spanish language popped last week on account of the World Baseball Classic.

Industry Notes

1. March Madness is officially underway. As usual, brackets are in shambles (looking at you Purdue), and the tournament has brought a variety of exciting games. The first round of the NCAA men’s tournament averaged a combined 8.4 million viewers on Thursday and 9.3 million viewers on Friday; Thursday’s showing was the best since 2015, and Friday’s the best ever. This is the third year that Nielsen has counted out-of-home viewership, which could be skewing numbers slightly upwards, but there is a distinct increasing trend in viewership. Last year, Kansas’ win over North Carolina drew 18.1 million viewers on Turner sports, the most viewership for an NCAA title game in history. If viewership in the first round is indicative of viewership for the bigger games over the next weeks, we should expect to see strong results all the way through the end of the tournament. | SMW, SMW

2. On the topic of basketball, the NBA is reportedly looking to increase the value of its broadcast rights deals by billions of dollars. The NBA’s deals with ESPN and Warner are set to expire in 2025 and the league is hoping to earn between $7 and $8 billion per year – that’s a huge step up from the $2.6 billion per year it’s making right now. The NBA’s expectations are not completely unreasonable; as we have observed with Thursday Night Football on Prime and MLS on Apple TV+, tech/streaming companies are willing to pay exorbitant amounts for exclusive sports broadcast rights. However, most of these companies have indicated that they are looking to rein in spending and see how their huge investments pan out before committing billions more to sports rights.

Another point in negotiations – national TV ad spend for the regular season is up 28% over last year, with just one month of play left. According to iSpot, spend has reached $656.9 million and impressions have risen 22% over last year. But what the rights may be worth, as a function of advertising revenue and revenue from carriage fees, and what Disney and Warner are able to pay, are two different numbers. Consider that the entire sports division of WBD earns about $2 to $3 billion in advertising revenue. If the cost of rights escalated 2x to 3x, profitability would not just be a concern, but an impossibility. Not to mention, WBD is struggling with a debt load of around $50 billion – CEO Zaslav has made cuts across the media empire and even suggested that the company does not need to keep the NBA. Disney is similarly saddled with debt, so the picture is not much better for ESPN. At the end of the day, the NBA will be fighting to secure the best deal and capitalize on the fact that money is being pumped into sports … and media companies will be fighting to keep costs low and maximize margins. Unless one of the major streaming companies decides that the NBA is a must-have and is willing to treat it as a loss leader, we will likely see rights increase just a modest amount come 2025. | The Information, Media Post

1. It’s safe to say that a lot has changed at Twitter in the last half year – the company was bought for $44 billion despite its new owner’s best attempts to get out of the deal; Trump’s infamous account has been restored (though he’s not tweeting); almost three-quarters of the company’s workforce has been let go; and the company is offering advertisers juicy incentives to spend money on the platform. Another major difference is the type of advertiser users are now seeing in their feeds – Twitter has historically skewed heavily toward brand advertisers, who made up about 85% of its revenue. This, frankly, was Twitter’s problem: it catered almost exclusively to brand advertisers but it is not a very good branding platform (content moderation and brand safety being one major reason). Now, with major brand advertisers having abandoned the platform (temporarily at least), direct response advertisers have begun to identify opportunities in Twitter’s less competitive ad auction market, and Twitter in turn is catering to these advertisers with more resources and better tools.

New CEO Elon Musk addressed the company’s ad strategy at a recent conference: “Twitter did not consider relevance in advertising until three months ago. How many products have you bought off Twitter? Probably zero. Performance-based advertising is really just advertising that is relevant.” For proof, look no further than Facebook: the company has been able to offer advertisers unparalleled scale, with almost 3 billion monthly active users, as well as precision targeting capabilities based on its extensive knowledge about those users (notwithstanding the impact of App Tracking Transparency). It is, or at least was, the ultimate performance marketing machine for the upper funnel.

In recent months, as big brands have stayed away, Twitter CPM’s have dropped about 20%. This creates new opportunities for performance advertisers, but it also raises questions about the sustainability of investment in the channel for such brands – Twitter’s ad targeting capabilities are still relatively rudimentary because of the paucity of individual information it collects on its users as compared to other platforms; and as other advertisers copy the methods of the early adopters, increased demand could wipe out those recent CPM reductions if Twitter can’t ramp its engagement levels. The imperative for Twitter now is to develop better targeting and optimization tools for performance advertisers so that they have a reason to stick with the platform even if the bigger players come back in. | WSJ

2. Blink and you might think it’s 2020 all over again – while this year hopefully won’t be quite as eventful, we are once again witnessing the federal government seriously threatening to ban viral video sensation TikTok on national security grounds. The presidents may change, but as so often, the policies rhyme.

The position of the U.S. government, led in this case by the Committee on Foreign Investment in the U.S. (CFIUS), is that Chinese law would require ByteDance (TikTok’s parent) to help Chinese authorities in intelligence and national-security matters if asked (somewhat ironically, major American tech companies are currently pushing to limit Section 702 of the Foreign Intelligence Surveillance Act, which allows the U.S. government to spy on the internet and telephone communications of people both in the U.S. and abroad without a warrant). Specifically, the worries are:

Based on these concerns, CFIUS has demanded that TikTok’s Chinese owners sell their stakes or face a U.S. ban. Deputy Attorney General Lisa Monaco said, “Our intelligence community has been very clear about China’s efforts and intention to mold the use of this technology using data in a worldview that is completely inconsistent with our own.”

TikTok has countered that “If protecting national security is the objective, divestment doesn’t solve the problem: a change in ownership would not impose any new restrictions on data flows or access.” Moreover, TikTok has already invested $1.5 billion in ‘Project Texas,’ an initiative to onshore all data storage and control with independent oversight.

So what does all this mean for advertisers? A lot of uncertainty. The app has revolutionized the landscape, pushing behemoths like Instagram and YouTube to completely overhaul their product strategies to stay competitive. TikTok will represent ~2.5% of the U.S. digital ad market this year, making any sort of ban highly disruptive to a large number of advertisers (not to mention the app’s users!). TikTok is reassuring its advertisers that a ban is very unlikely, but they are understandably making contingency plans – our chief client officer Diana DiGuido noted that brands “can’t have any gaps in performance, so they are looking at where they can replicate the performance they are getting from TikTok.” | WSJ

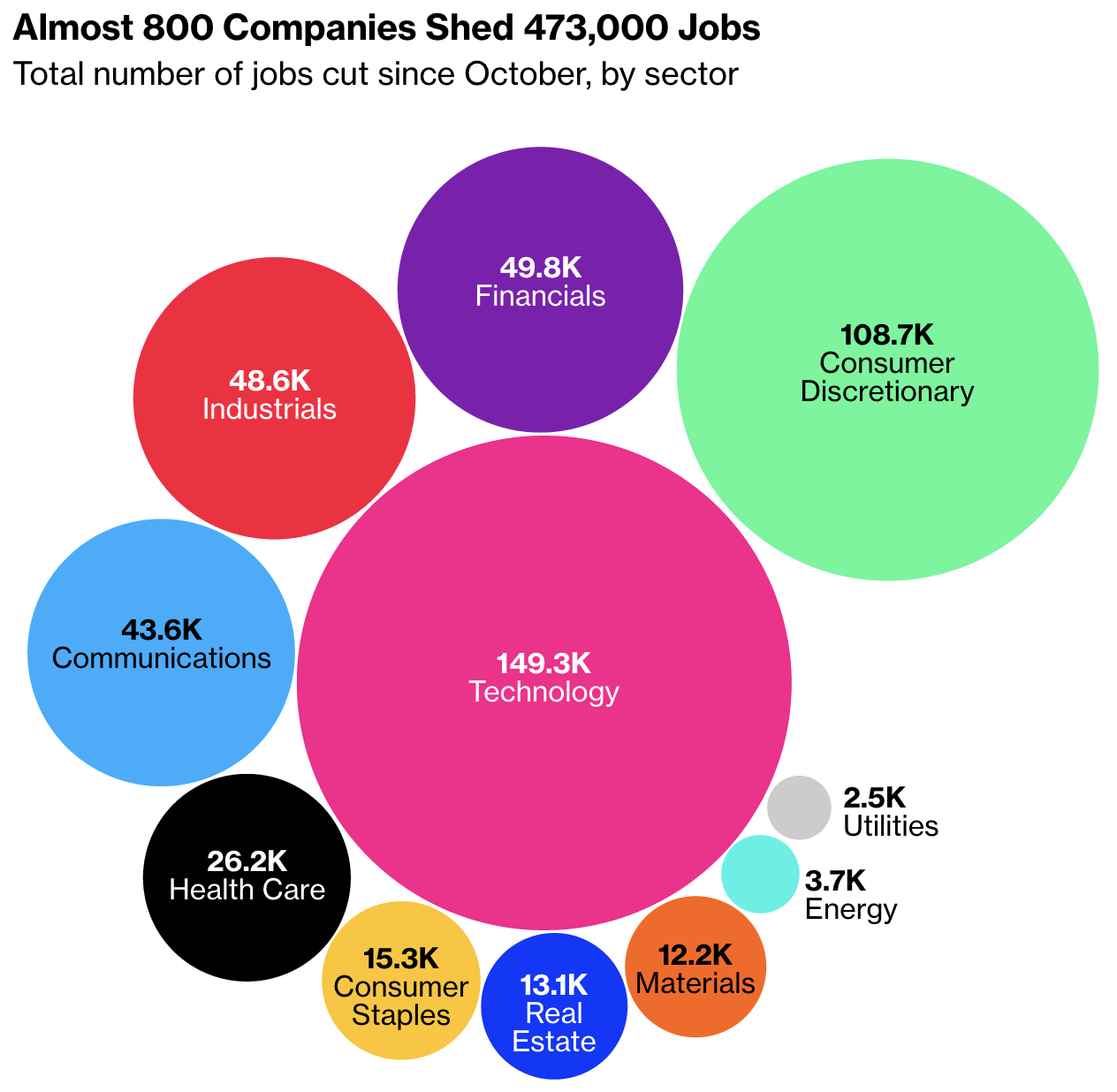

As data from the Department of Labor indicated last week, the job market is strong, if cooling slightly. Indicators of moderation included a decline in available jobs and increase in layoffs, though with unemployment historically low, those had little impact on the big picture. In the tech sector, layoffs continue: Amazon and Meta recently announced that they will be going through additional rounds of layoffs, letting go of 9,000 and 10,000 employees respectively.

The question weighing on economists, policymakers, and employees is the same: are layoffs limited to tech? On a global scale, the answer is obviously “no.” Ikea laid off 10k employees in Russia, Credit Suisse laid off 9k across Europe, and FedEx laid off 12k in the United States. About 20 companies are responsible for half of the firings since October of last year, and they span industries from tech to real estate. But in the United States, the biggest layoffs are more limited to tech, with Amazon, Meta, Alphabet, and Microsoft all cutting more than 10k jobs. As we have discussed at length in this newsletter, the majority of those layoffs appear to be a corrective to aggressive hiring in tech during the pandemic, spurred by extraordinary consumer demand in the ‘20 – ‘21 period.

However, it seems clear now that these labor market adjustments are not confined to Silicon Valley. There are layoffs occurring throughout industries in the United States, which seems indicative of a slowdown in the macro economy as opposed to an industry-specific correction. As the Fed raises interest rates again, we could see a greater cooling of the labor market as the economy slows down. | Bloomberg