Media Update: Amazon and Apple Bet Big on Cinemas, YoY U.S. Advertising Investment Down, and Inflation Trends

Ad-supported video supply continues to trend gradually up, as incremental sources of supply (Netflix, Disney+) come online and begin to make a dent in the macro picture.

Industry Notes (Video)

1. After Amazon announced its $1 billion/year venture into cinema last November, Apple is following in lockstep and investing $1 billion/year to produce original films for theatrical release. While Apple has had commercial and critical success with its original series like The Morning Show and Ted Lasso, it has yet to build a strong library of movies. Why are Apple and Amazon now embracing theaters? While the film industry is highly competitive, successful movies can generate billions of dollars in revenue, with some of the highest-grossing movies of all time earning over $2 billion worldwide. Apple TV+ also has a much smaller subscriber base (presumably – Apple won’t say) and thus a theatrical release ensures more eyeballs. Similarly, Amazon Prime reaches less than half the viewership of Netflix, and has acquired properties like MGM that can be leveraged for theatrical releases and more eyeballs. Outside of a motivation to reach profitability on an individual project basis, theatrical releases are also a valuable marketing opportunity – the press that’s generated can help build awareness ahead of a film’s release on streaming. Additionally, a film needs to meet certain requirements (such as premiering in a physical theater) in order to be considered for awards like the Oscars. Amazon and Apple are spending as much on original content as traditional studios, so being recognized among the biggest players in Hollywood boosts profile, which in turn could push a new set of subscribers to the service.

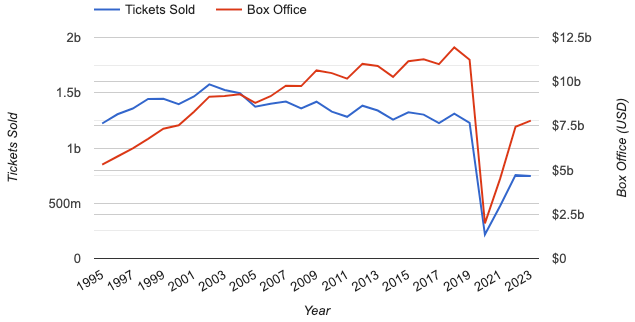

Of course, Apple and Amazon’s strategy to move to theaters is still dependent on the viability of the struggling movie theater industry. Back in November we noted the irony of streamers producing movies for theatrical release, much like how Amazon opened book stores after destroying the book store market. Well it appears to be exactly like that, as there are rumors that Amazon is looking at acquiring the largest movie theater chain, AMC. We’d like to stress that this is a rumor for now, and no offer has been made. However, if Amazon follows through, it would be taking over a struggling business: as you’ll note in the chart below, movie theaters have languished, with attendance down about 50% from the pre-pandemic level. (Note: 2023 is shown on an annualized basis.)

Bottomline, streamers have made large investments in original content, and revenue from subscriptions is not a sustainable solution. We have frequently discussed how adding advertising into SVOD was the first step in rectifying this issue, immediately generating more revenue from subscribers. Theatrical releases are also an additional revenue source that helps amortize programming costs across as many eyeballs as possible. The windowing strategy, in which films appear on the silver screen before hitting streaming, allows for effective price discrimination, following a tried and true model. Like traditional studios, streamers will be experimenting with distribution strategies to find that which is maximally effective in driving ticket sales and subscriptions. | Bloomberg, Bloomberg

2. It’s opening week for MLB, and we have a number of interesting baseball and streaming stories for you. Firstly, Fubo and Apple TV+ have added additional MLB content to their channel lineups for the 2023 season. Fubo is including MLB.TV as an add-on for $25 per month, which is the same price a viewer would pay if they bought the service independently. This model, allowing users to stack services on a singular platform, has become increasingly popular for vMVPDs as a means of centralizing the fragmented streaming space for consumers. The move comes as Fubo strengthens its position as a sports-centric platform, and drops the word “TV” from its name (in case you hadn’t already been lopping off that part). The MLB.TV add-on gives users access to out-of-market regular-season games, select spring training games, and regional sports networks (including the beleaguered Bally Sports). Fubo now offers the most baseball coverage of any streaming company.

Baseball remains one of the most popular sports in the United States with a large, dedicated following of viewers. During the 2022 season, MLB.TV recorded 11.5 billion minutes watched, marking a 9.8% increase over 2021 and the first time minutes watched surpassed 11 billion. Despite the popularity, streaming platforms are learning that sports are not an effective loss leader – viewers rarely “hang around” and watch other content, meaning that the streamer can’t make back their investment. This explains why Apple TV+ is now making users pay for its 30+ Friday night MLB games. These games were free to view during the 2022 season as Apple made its foray into live sports streaming. In general, streaming platforms now charging for once-free content is a trend that will likely continue as these companies focus on bottom-line profitability.

As regular readers of this newsletter are well aware, we are nearing the event horizon of traditional regional sports networks with Bally Sports (the largest group of RSNs) declaring chapter 11 bankruptcy, and Warner Bros. Discovery announcing that it would be getting out of the RSN business with AT&T SportsNet. It is still unclear how rights will shake out, but if the system of RSNs breaks down, it is likely that MLB will regain control and the DTC model will proliferate. The core issue of this debacle is that RSNs are very expensive. Take for example the Pittsburgh Pirates: the team is supposed to receive $60 million annually from AT&T SportsNet, but its games average just 55k viewers. This means that each fan would have to pay $1,090 per season for the Pirates to reach the same amount of revenue in a DTC model. This is not to say that DTC can’t work as a replacement, but to demonstrate the challenge that teams will face with the decline of traditional television and the RSN system. | Fierce Video

Sports viewership continues to trend very strongly on a YoY basis. All other programming genres are down materially.

Industry Notes

1. As the March Madness tournament approaches its end, we are left with a very surprising field for the Final Four. Three of the four teams (SDSU, FAU, and Miami) have never reached the semifinal stage and not a single one, two, or three seed will be playing. While Cinderella stories are great for ESPN 30 for 30 documentaries, they are not so great for live viewership – it is possible, and even likely, that viewership for the Final Four and the national championship game will be unimpressive because the teams involved have weak brands.

Generally speaking, specific matchups in sports can have a huge impact on viewership. The first casual factor is the popularity of the teams: you may recall that this year the Cowboys posted better viewership than the rest of the NFL – oftentimes regardless of the opponent – and were present in four of the five most viewed games of the regular season. Viewership for their games defies broader trends because their market is large and their fans loyal. The opposite example is the Bucks-Suns NBA finals in 2021, which drew 35% less viewership compared with the pre-pandemic 2019 finals, likely because the teams come from smaller markets. Secondly, the game needs to be close: look no further than the College Football Playoff title game this year, in which Georgia clobbered TCU and drew the smallest audience on record. For the CFP title games, the four least viewed broadcasts included losses by three or more touchdowns.

Of course, it could be the case that these Cinderella runs bring an equally magical rise in viewership – but based on historical performance, it seems unlikely. | The Athletic

2. Baseball season kicks off this week, and by all evidence there is a lot of momentum around the sport this year. The World Baseball Classic (WBC), an international competition in which players represent their countries, pulled in amazing viewership throughout the tournament. Four of the top ten all-time most viewed games of the WBC occurred this year, with the Japan-USA final drawing 4.97 million viewers on FS1 and Fox Deportes. That viewership represents a 69% increase over the previous high in 2017. For context, in MLB the only event that reaches over 5 million viewers consistently is the World Series – WBC final viewership was virtually on par with the NLCS and ALCS. This year’s WBC featured more teams and more games than any previous year.

Turning to MLB, viewership for spring training is up a notable amount; ESPN experienced its most watched preseason in seven years, averaging 378,000 thousand viewers for the four-game afternoon slate, likely a result of new rules that speed up the game. Beginning this season, MLB is instituting a 15-second pitch timer that can penalize a batter or pitcher for not being “set” and a rule against infield defensive shifts. Spring training games were 25 minutes shorter on average(!),cutting game time to 2 hours and 36 minutes per nine innings. This is most certainly a good thing for baseball broadcasts – MLB games have not averaged under 2:50 since 2006, and the length of games is a constant source of complaint for casual viewers. The shift rule should also help put more baseballs into play, thereby increasing scoring, excitement, and viewership. | SMW, ESPN, CBS

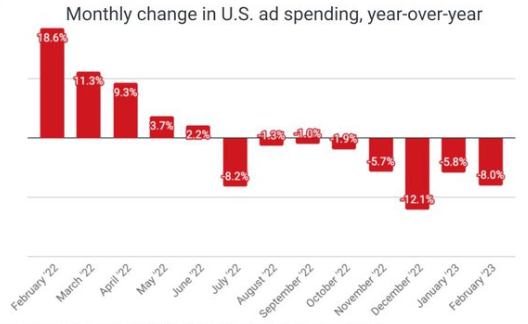

As 2023 continues, so does the decline of the advertising economy. February marked the eighth straight month that ad spending declined, falling 8% YoY. As has been the case over the past few months, February faced a tough comp in last year, where ad spending increased 18.6%. Going forward, that comp should be more reasonable, as it was in the second half of February 2022 that advertisers broadly began to pull back.

In related news, Manga has revised down its 2023 U.S. ad spending projection from 3.7% to 3.4% growth. The IPG unit expects investment to pick up in the second half of the year, fueled by the rise of ad-supported video streaming, such as Netflix and Disney+. According to Magna’s head of global market intelligence:

In a similar economic climate 10 or 20 years ago, the U.S. advertising market would almost certainly fall off a cliff. Things are different in 2023 because of media innovation fueling marketing demand.

This sentiment – that advertising has become a greater priority in the boardroom – is evident in the continued spending of major brands like Coca-Cola and P&G. | Media Post, Ad Age

1. We’ve spilled a lot of ink on the inflation situation over the past two years, nearly all of it bad, from the fact of prices increasing at rates not seen for forty years to the Fed’s inflation-fighting efforts inducing a banking crisis that led to even more federal intervention in the economy. So how about a little (potentially) good news – according to economists at the Cato Institute, Producer Price Index inflation has averaged just 1.1% since last June, and there are compelling arguments that it presents a better gauge of price changes than the standard CPI measure. From Cato:

[PPI] has one big advantage over the CPI—the PPI does not include the extremely misleading […] estimates of “ownerâ€â€‹equivalent” rent. Such “shelter” accounts for a third of the CPI, which makes it a very serious issue indeed.

Although market rents have been falling since last summer, BLS estimates of rents on old and new leases still keep soaring in CPI monthly reports—at a 9.6 percent annual rate for the past three months!

Once we exclude shelter from CPI inflation, the resulting “CPI less shelter” is about like the PPI.

This issue of lagged rents distorting inflation measures is one we’ve discussed previously. When we overlay the PPI with the Fed’s benchmark interest rates, it paints a picture of a much more effective monetary policy than we generally hear in the media.

Indeed, the tight negative correlation between PPI and interest rates lends some weight to the heterodox long and variable leads view, which argues that the macroeconomy responds rapidly to changes in the expected future path of monetary policy. We will refrain from weighing in on either side of a debate that is above our pay grade, but we’re crossing our fingers for a return to low, stable prices. | EconLog, Cato Institute

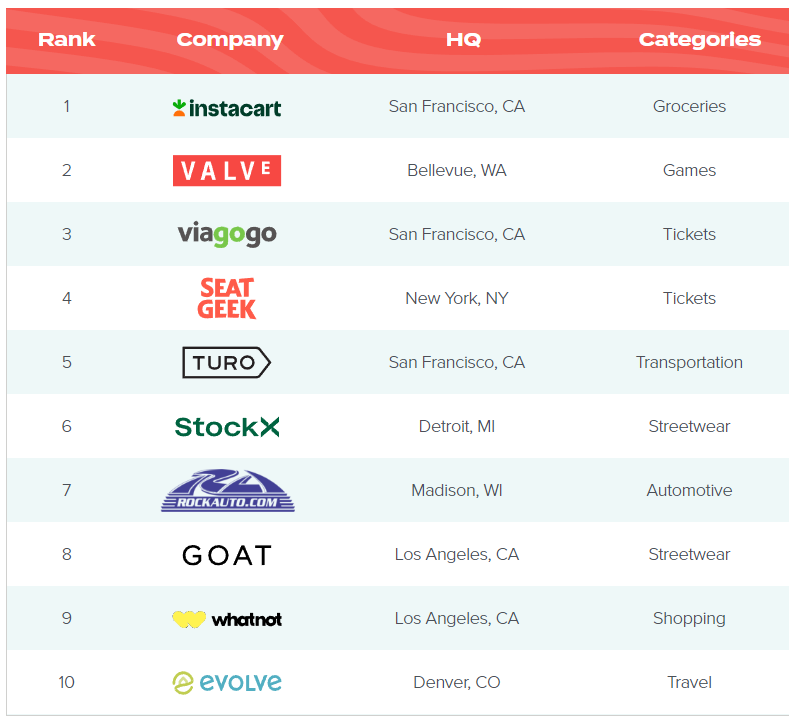

2. Andreessen Horowitz, the venture capital firm, released its popular “Marketplace 100” this week, highlighting some of the most important trends in the industry. This report looks at consumer-facing marketplace start-ups and private companies according to annual gross merchandise volume, with an eye toward where these markets are headed. Marketplace companies are an increasingly important segment of the consumer economy – incumbents of this list grew 114% YoY, while newcomers (of which there were 37) grew 174%. The fastest growing categories on this list reflect the enduring effects of the Covid-19 pandemic:

Also notable is the breadth of industries being made over by marketplace models – it’s not just one or two corners of the economy where novel business models are making an impact:

The a16z report distills six key takeaways:

There is much more of interest at the link. | a16z