Media Update: Sony’s Acquisition Moves, SSP Concerns, Ad Platform Trends, and Slowed Wage Growth

Sports viewership fell year-over-year as we moved into May. While the Kentucky Derby did set audience records amid a photo finish, a lackluster first round of the NBA playoffs was unable to keep up with 2023 figures. Meanwhile, news viewership remained elevated as former President Trump’s New York trial continued. In a further sign of the uncharted media waters we are entering, President Biden accepted an invitation to debate former President Trump in June, ahead of the typical schedule, accelerating some of the most-watched broadcasts of an election year.

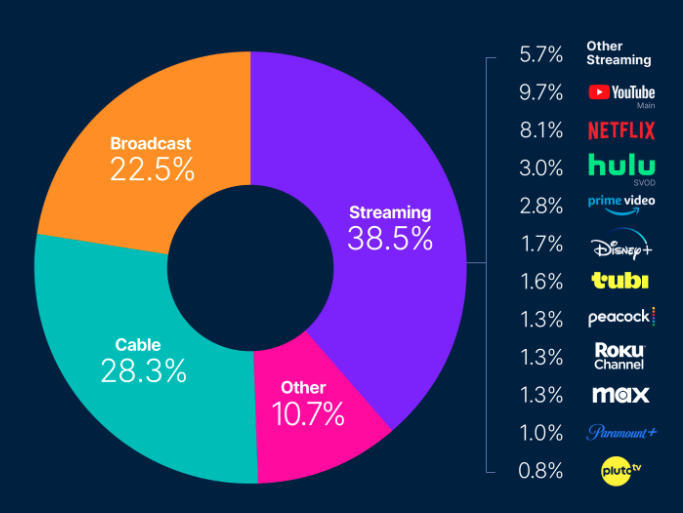

Consolidation has been the name of the game for streaming publishers lately, with recent weeks seeing major developments. First up – Paramount Global, which has become a hot acquisition target. While Paramount looked close to a merger with Skydance just weeks ago, negotiations have reopened with other bidders, and now Sony and PE firm Apollo are at the table. The legacy media giant holds many highly regarded properties and pieces of IP, but its Paramount+ streaming service hasn’t achieved the highs of its competitors, trailing services such as the Roku Channel and Peacock in viewership and lagging far behind Netflix, Hulu, or Prime Video.

Time will tell in whose hands Paramount ends up, but the industry trend towards consolidation & acquisition is obvious. This was further evidenced by an announcement that Disney and Warner Bros Discovery will offer their streaming services as a bundled package. Per the companies, audiences will be able to subscribe to Hulu, Disney+, and Max on a single purchase with both ad-supported and ad-free options.

While this deal is not quite so aggressive as an outright acquisition or platform unification, it shows both growing partnership between these legacy media giants (already teaming up on a new streaming sports venture) and an emphasis on simplifying the streaming space for consumers. As if in response, Comcast announced just days later a bundled offering for Peacock, Netflix, and Apple TV+. The consolidation era is here, and while more details on these specific partnerships are still to come, it does suggest that after years of increasing streaming diversity, we may soon be in an environment with fewer-yet-larger players. | LA Times, Variety, Variety, WSJ

Spotify may be the world leader in streaming audio with 30% market share, but the Swedish giant seems less-than-content reaching audiences through their ears alone. Appearing at NewFronts, Spotify put its video podcast content front-and-center. The service announced that over 500K video podcast episodes have been added to Spotify’s library in 2024 alone, bringing the total figure to over 2.5 million; video engagement time rose 48% year-over-year as well, showcasing increasing audience appetite for a blended experience. Spotify’s Head of Sales Ann Piper was unequivocal in framing Spotify’s place in the video space: “We’re ready to play in the digital advertising pool and compete for more than audio budgets… Now that there is more video being created on the platform, we want to connect brands with users when they are looking at their screen.”

We at Tinuiti have long touted the value of “see-say” elements in advertising, as blending aural and visual elements is a way to improve audience attention and reinforce key ideas. By increasing their focus on video content, Spotify is signaling that it wants to be considered as viable an advertising medium as any CTV-based property; to do so, the platform is promoting video formats such as video takeovers, sponsored sessions, and opt-in video ads. As we called out here just two weeks ago, the lines between advertising mediums are becoming ever more blurry, and Spotify’s video emphasis is further proof. Advertisers looking to expand their video presence beyond traditional streaming platforms should pay close attention. | AdWeek, MediaPostThis forum has covered streaming sports’ rise at length in recent weeks, so we’ll keep today’s update brief. In the NFL, Netflix is slated to broadcast two of the league’s Christmas Day games this winter. This represents the leading streamer’s first foray into the nation’s most popular sports league, following in the footsteps of Prime Video, Peacock, and Paramount+. Meanwhile, Roku looks set to begin broadcasting Sunday baseball games after coming to a multi-year agreement with the MLB. With this announcement on the heels of Roku’s launch of an NBA FAST channel, we continue to see almost every streaming platform clamoring for a place at the sports table. | NBC Sports, Variety

An Adalytics report has once again become the topic du jour. In a study of 16 supply-side platforms (SSPs), Adalytics claims that Colossus SSP, one of the largest DEI-focused SSPs, misrepresented user IDs in ad auctions. For those not familiar with Adalytics, they are an ad quality and transparency platform which has received attention for their investigations into media buying practices, including several reports that delve into the Google advertising landscape.

Within the SSP analysis, Adalytics claims that the misdeclaration of user IDs happened in the majority of observed Colossus SSP impressions. There are a couple reasons why misdeclaring user IDs is an issue. First, these IDs are used to build audience profiles based on a user’s past behavior. If the ID provided by the SSP to the DSP is inaccurate, advertisers won’t be able to deliver ads to the intended audience or execute proper frequency capping.

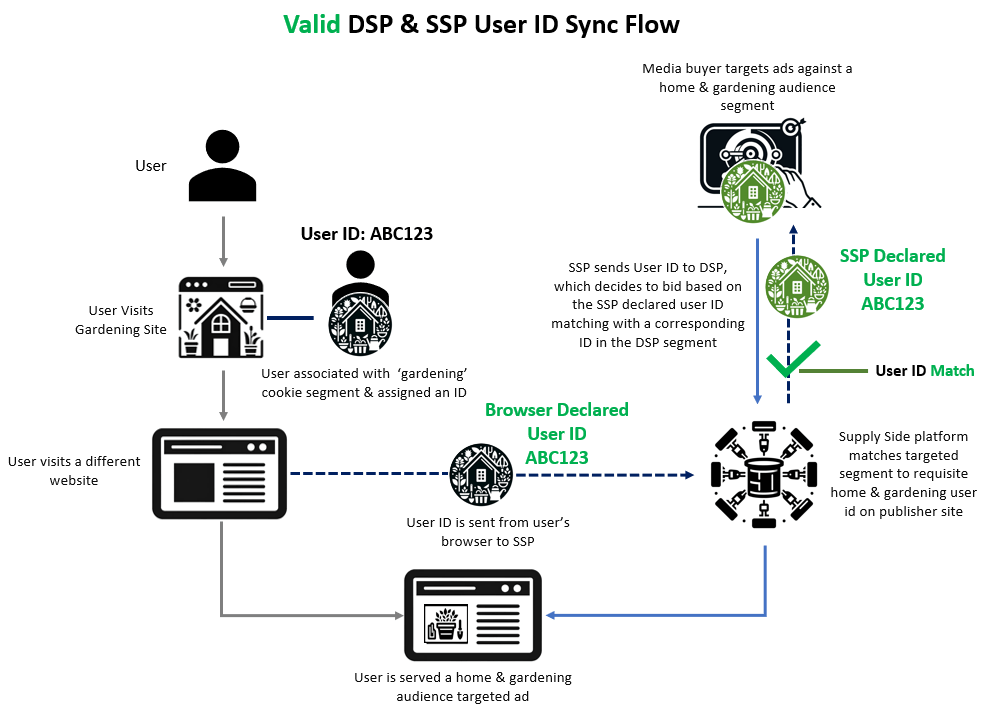

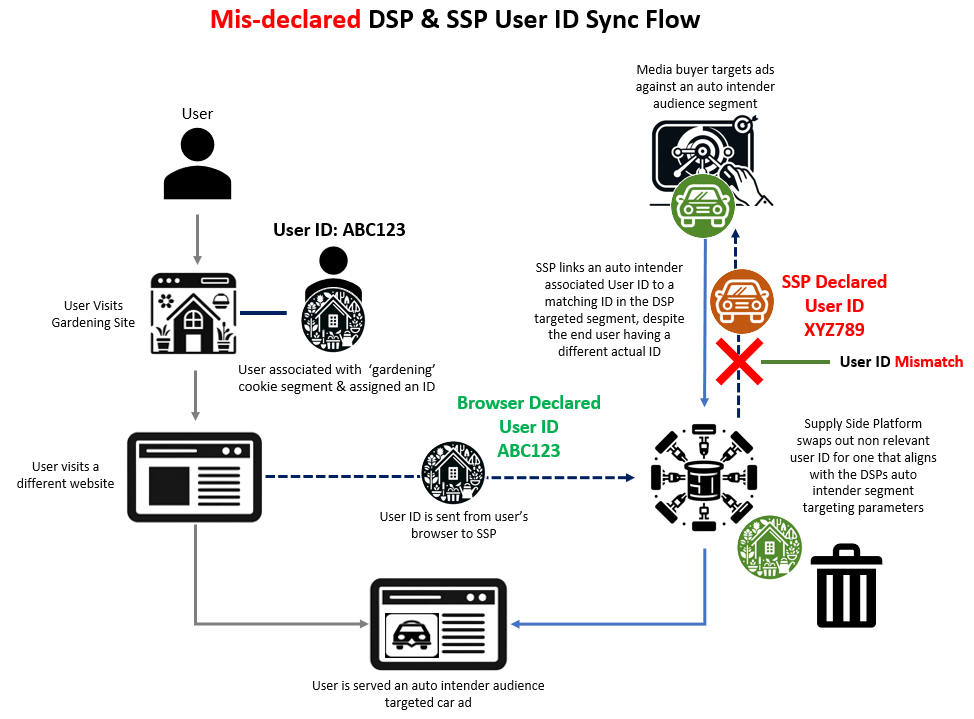

As an example, let’s say we have a gardening consumer known as user ABC123. In the illustration above, we see when the ID is properly declared from the SSP to the DSP, advertisers targeting a home and gardening audience may show an ad to user ABC123. However in the illustration below, we see that the SSP has declared a different ID (XYZ789) to the DSP for our gardening consumer. This then causes an auto advertiser to serve an ad to the user, creating a wasted impression for the advertiser and a poor experience for the user.

Another issue of misdeclared IDs is the potential impact of users’ “right to know” privacy rights under Europe’s GDPR or California’s CPRA legislation. Due to the misdeclared IDs, users may be unable to verify the information being collected about them.

Within the report, Adalytics highlights that Colossus works with numerous ad verification vendors, including Oracle Moat and HUMAN to filter out fraud. While the misdeclared IDs from a large SSP are cause for concern, the inability of ad verification vendors to prevent or flag the irregularity is equally alarming, raising questions around the efficacy of these partners and warranting a further review of their capabilities.

Adalytics does note the analysis was done using publicly accessible data and cannot confirm if there is a specific use case or technical reason for the misdeclared IDs nor do they know if there are any post-ad impression corrections or reconciliations. That means while an ad was served, the impression may not have been charged, limiting the monetary impact.

While this story will continue to evolve, the report reinforces the need for advertisers to deploy a robust supply path optimization (SPO) program centered around building close relationships with a limited number of quality-supply partners. At Tinuiti, we focus on three elements to ensure we are optimizing the supply chain. First, we leverage pre-bid filters in the DSPs to negate any questionable partners and inventory. Next, our teams run SPO tests to refine inventory sources and drive performance. Lastly, we build and maintain strong relationships with supply partners and tools, allowing us to identify & curate quality inventory across supply sources on relevant content that drives business outcomes. | Adalytics, The Drum

First it was the major streaming players that looked to augment their branding by adding a Plus or a Max, now it’s the advertising platforms taking this uninspired approach toward branding for their campaign types. First we had Google with Performance Max (or PMax as we’ve come to call it), then Meta launched Advantage+, soon followed by Microsoft launching their own iteration of PMax, and most recently, Amazon announced the official launch of their AI-driven campaign type, Performance+. Regardless of the branding, it’s clear that we are well and truly in the era of AI-driven advertising. While the advent of AI-driven campaigns was initially met with skepticism and even dissent from the lever-pulling AdWords-til-I-die purists, we’ve seen the tides of sentiment turn as advertisers have come to appreciate the performance gains associated with AI-driven campaigns.

The reality of AI-driven campaign types is that they learn & adapt over time. This is the nature of machine learning, thousands of permutations are tested rapidly, winners win, and losers are left in the dust. At a fundamental level, the learning is guided by reward & punishment feedback mechanisms akin to B.F. Skinner’s theory of Operant Conditioning, but how sure can we be that those signals are accurate? Given the convergence of AI-driven campaigns along with the increasing fragility of deterministic signals, it seems only natural to be skeptical – but, therein lies the power of other AI solutions to estimate conversion signals in order to power other AI solutions. Yes, the future of agents interfacing with agents is already here and we are their humble servants assisting them on their journey towards AI-marketing nirvana. While some look at this moment with desperation & fear, others are seeing the opportunity to shift their capabilities towards these new levers of control. Much like a soccer player that no longer has the legs to run up & down a field for 90 minutes, yet, still has the mindset, we are seeing a rapid shift from media managers as players, to media managers as coaches.

“Will everything become PMax?” – a question posed to our team during a recent analyst briefing. It would seem almost inevitable that all advertising platforms will lean in this direction, however, it is simply not possible for all advertising platforms to do this well. Critically, the amount of data required for accurate modeling and decisioning is a major line in the sand between the haves & have nots. While we can be sure that eventually everything within the Google, Microsoft, Meta & Amazon walled gardens will take on PMax characteristics, the same cannot be said across the open web. The ramifications here, just like the inevitable death of the 3P cookie, are a disproportionate advantage to the large platforms that will only continue to accelerate.

As Google prepares for their annual Google Marketing Live event next week, it is almost certain that PMax will take center stage once again.. If you are still on the fence about embracing the power of AI-driven campaigns, now may be the time to look in the mirror and question why you still hold this view. Google et al. are clear in their intentions – we’re on the highway to Pmax and they are burning the boats. | WebMD, Google, Meta, Microsoft, Amazon

One of the remarkable features of the American economy in the 2020s has been the seemingly imperturbable health of the labor market. For comparison, consider the 2008 Great Financial Crisis – unemployment peaked at 10%, and it took 94 months for unemployment to come back down to pre-recession levels. By contrast, unemployment peaked at a terrifying 14.8 percent in April 2020, and it took only 29 months to come down to pre-recession levels that were already absurdly low by historical standards. Very different contexts to be sure, but by any measure it was the most rapid labor market recovery in American history.

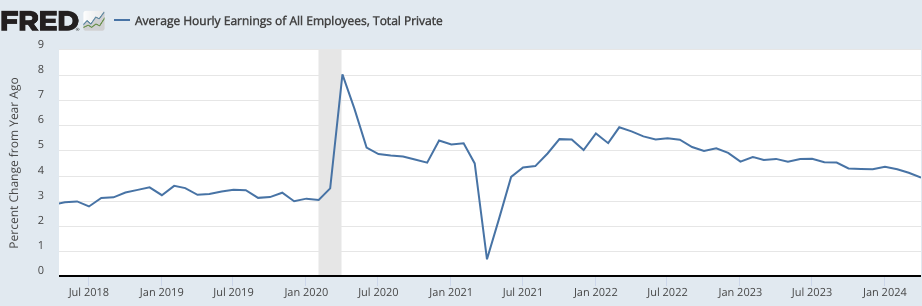

This has become, somewhat oddly, a bit of a problem in the inflationary, high-interest-rate environment in which we find ourselves. American businesses’ and workers’ continuing ability to find profitable trades (i.e. jobs), and to continue raising wages much faster than the pre-pandemic norm, has made it harder to put the inflation genie back in the bottle and to begin lowering interest rates, something many businesses and consumers are eager to see. This dynamic may now be changing.

In April, average wage growth dipped to its lowest level since May 2021 (recall that price inflation spiked up in summer 2021), signaling cooling in the underlying labor market.

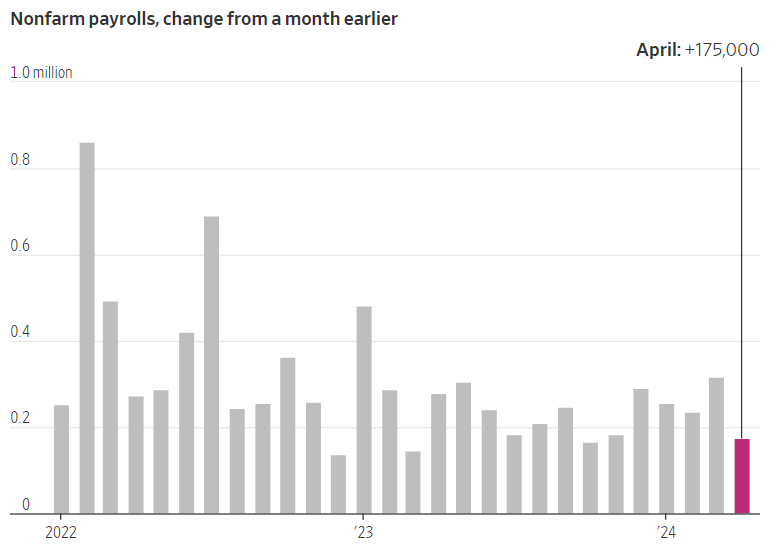

We also have several other data points that reinforce this image of labor market cooling. Job growth slowed and unemployment ticked slightly higher in April, a break from the rapid job gains in recent months.

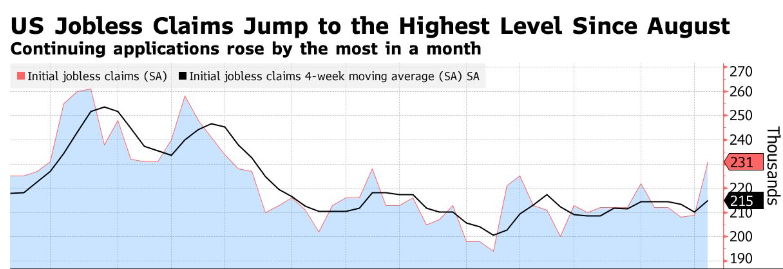

We’ve also seen initial jobless claims spike significantly in April, to their highest level since last August:

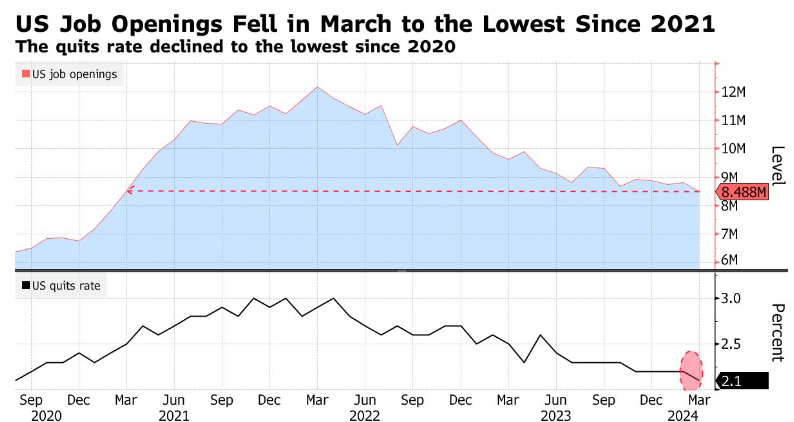

And job openings fell in March to the lowest level in three years, while quits and hiring slowed:

Any individual data point is far from dispositive, and we should always remain cautious about over-interpreting micro-trends in high-frequency data. Nevertheless, the multitude of independent data points all suggesting labor market softening indicate a genuine underlying shift. Please don’t go buying any interest rate futures based on what you read here, but these look like the signals rate-cutters have been hoping for. | TheMoneyIllusion, WSJ, Bloomberg, Bloomberg

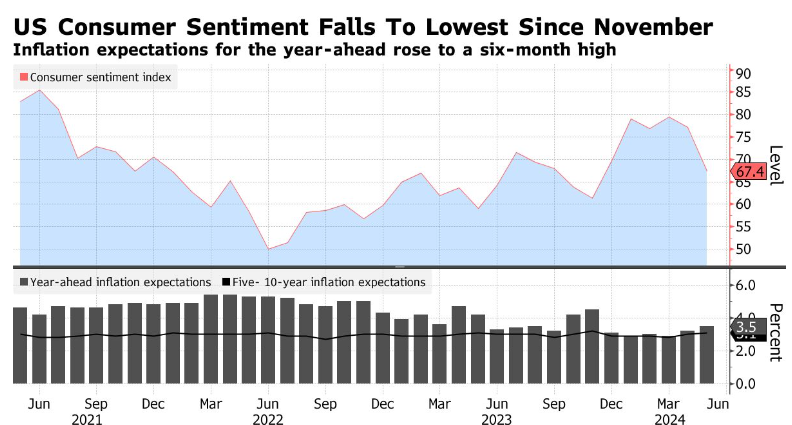

We told you last time that consumer sentiment had fallen somewhat in April, but cautioned not to read too much into what may just be noise in the signal; newer data on consumer sentiment show a precipitous drop in early May, reaching a six-month low, suggesting this isn’t just noise:

The decline in sentiment was broad across age, income and education groups, and across political affiliations. The deterioration in sentiment seems to correlate with rising short-term inflation expectations and concerns about the labor market. On the first point, consumers may be pleasantly surprised if, per the story above, wage disinflation leads to price disinflation; on the second point, things are unlikely to get much better because they can’t get much better – unemployment is at historic lows, and real wages are near all-time highs. Absent massive supply-side reform – and all political trends are moving in the opposite direction – wage and employment growth are very unlikely to accelerate in a significant way. | Bloomberg