Media Update: Warner Bros. Discovery Profits on DTC, EPSN Looks for Flexibility, and Writer's Strike Impacts Advertising

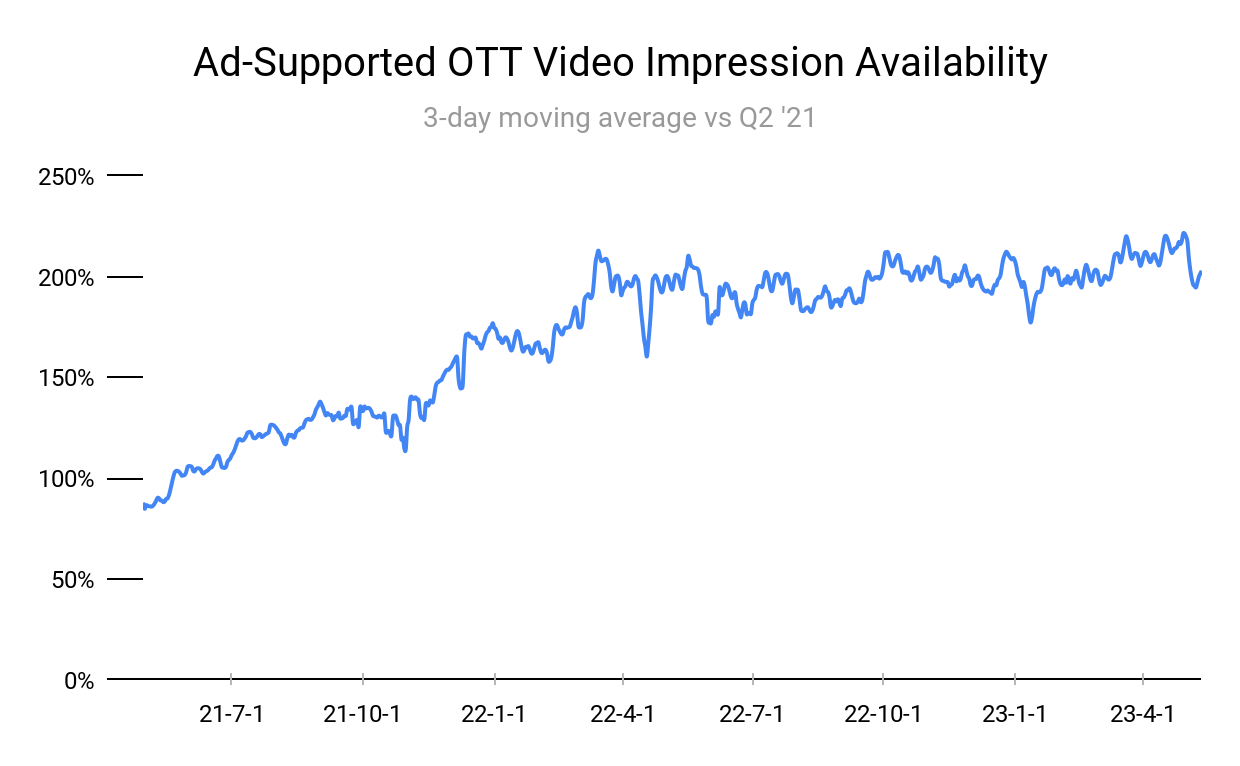

Ad-supported video supply ticked up in mid-May after falling in the previous weeks.

Industry Notes (Video)

1. Last November, Disney introduced bundling, packaging together Hulu/Disney+/ESPN and a smaller Hulu/Disney+ bundle. It shouldn’t come as a big surprise that Disney+ and Hulu will be merging into a single app, the latest step in the consolidation of the Disney bundle. To be clear, these services will still be offered stand-alone to consumers, so Disney is not forcing consumers into the bundle quite yet. The progression of its bundling strategy, working towards a comprehensive streaming experience catering to a broad spectrum of audience preferences, seems to imply that a cable-esque bundle is the endpoint. Across the industry, streaming companies are rolling out their bundles and beginning to sunset smaller stand-alone services, but there’s not one obvious strategy to minimize customer attrition. For example, Paramount+ will be incorporating Showtime into its platform and ending the stand-alone product by the end of the year. On the other hand, Warner Bros. Discovery reversed its decision to end Discovery+ in the merger with HBO Max. While there is still a strong appetite for streaming, we don’t have a ton of data on how consumers will react to concentrated streaming bundles – hence the different approaches across publishers.

Disney also faces the challenge of organizing its disparate content to cater to the distinct audiences of Disney+ and Hulu, as it attempts to properly balance content arrangement, personalized recommendations, and user-friendly interfaces. Moreover, there is a certain tension over brand identity in combining the family-friendly name of Disney with that of Hulu. As bundling progresses in the streaming industry, we can expect to see these media conglomerates continue to experiment with different pricing models and distribution methods to capture audiences. | Adweek

2. After acquiring MGM and its extensive library of original content for $8.5 billion in early 2022, Amazon will begin licensing its original movies and films on other sites. Previously, Amazon used this content to attract new subscribers and boost interest in its Prime Video platform – this strategy shift indicates a clear focus on profitability, aligning with a broader industry trend of streaming giants striving to balance exclusivity and revenue generation.

Amazon has faced financial challenges recently, with reports of layoffs and budget cuts surfacing. This move to license content could be seen as a response to these financial challenges, as the company seeks to boost revenue through streaming or advertising. This trend is also mirrored in the approaches of other major players in the space, such as HBO Max. This broader access not only invites new audiences but also enriches the overall content ecosystem available to viewers across various platforms. | Bloomberg

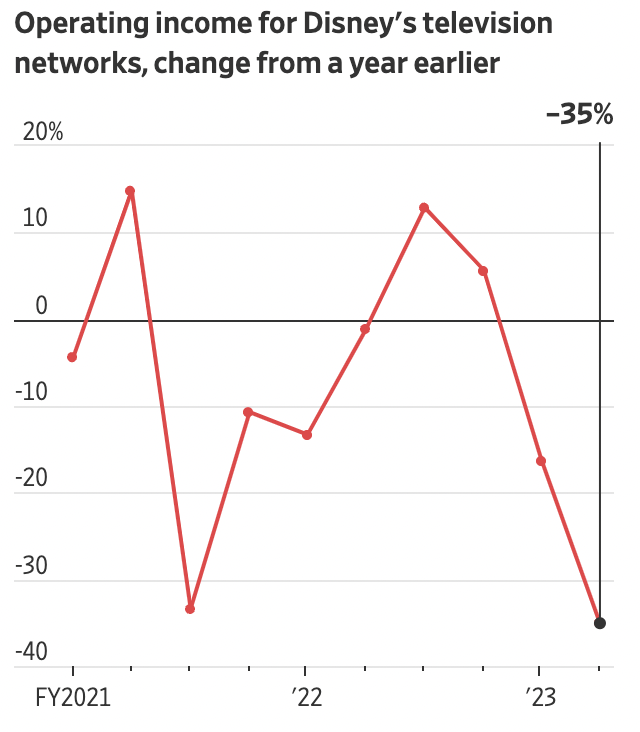

3. In Q1, Warner Bros. Discovery accomplished what few other premium streamers have – a profit in its DTC business. A year ago, WarnerMedia and Discovery posted a combined loss of $654 million. At the same time, their merger closed and CEO Zaslav wasted no time in trimming the fat, shuttering CNN+ just one month after launch. In the ensuing months, popular projects (like Batgirl) were canceled and staff were cut at HBO and CNN as the company pursued its target of $3.5 billion in post-merger savings over three years. Fast-forward to now – the media company cut expenses in its DTC unit by $764 million YoY and earned $50 million in profit. Overall profit for the company was not as great because of a weak ad market, but this is nonetheless an important milestone for WBD. More than that, it proves that the streaming business doesn’t have to be a loss leader for the major media companies.

Although advertisers would like to hear that WBD’s success is coming from incredible growth in subscribers and increasing ad inventory, the truth is that it is largely the result of cutting expenses. The company did add subscribers in Q1 – as did Netflix, Peacock, Paramount+, and others – but rising revenues would not have got it to profitability alone. Indeed, almost unanimously across the industry, streamers are looking to cut costs. Just recently the Wall Street Journal reported that Netflix is planning to reduce spending by $300 million with a renewed focus on profitability. As subscriber gains narrow and churn increases, we are seeing streamers be a bit more discriminating in how they deliver content in order to maximize engagement. So, while moves to increase revenue (such as increased ad-supported offerings) may be beneficial, WBD has shown that reducing expenses contributes to profitability. | WSJ

4. In its latest move to compete in the television arena, YouTube will be bringing 30-second unskippable ads to select videos shown on TVs. This ad inventory was made available for brands at YouTube’s upfront, and will only be shown against the top 5% of the platform’s content, which has the most viewership and user engagement. According to the company, 70% of those impressions are served on connected TVs. In the past few years, we’ve seen YouTube aggressively push into the television space, chasing TV ad dollars, and for good reason – 45% of all YouTube viewership occurs on CTV and the streamer outpaces all others in TV usage. The company also introduced pause ads in its upfront presentation, following in the footsteps of competitors like Disney, Roku, Amazon, and NBCU. With these moves, YouTube is hoping to court advertisers and convince them that its ad inventory, which distinctly consists of user-generated content, is just as valuable as television content because the viewing medium is the same. | Ad Age

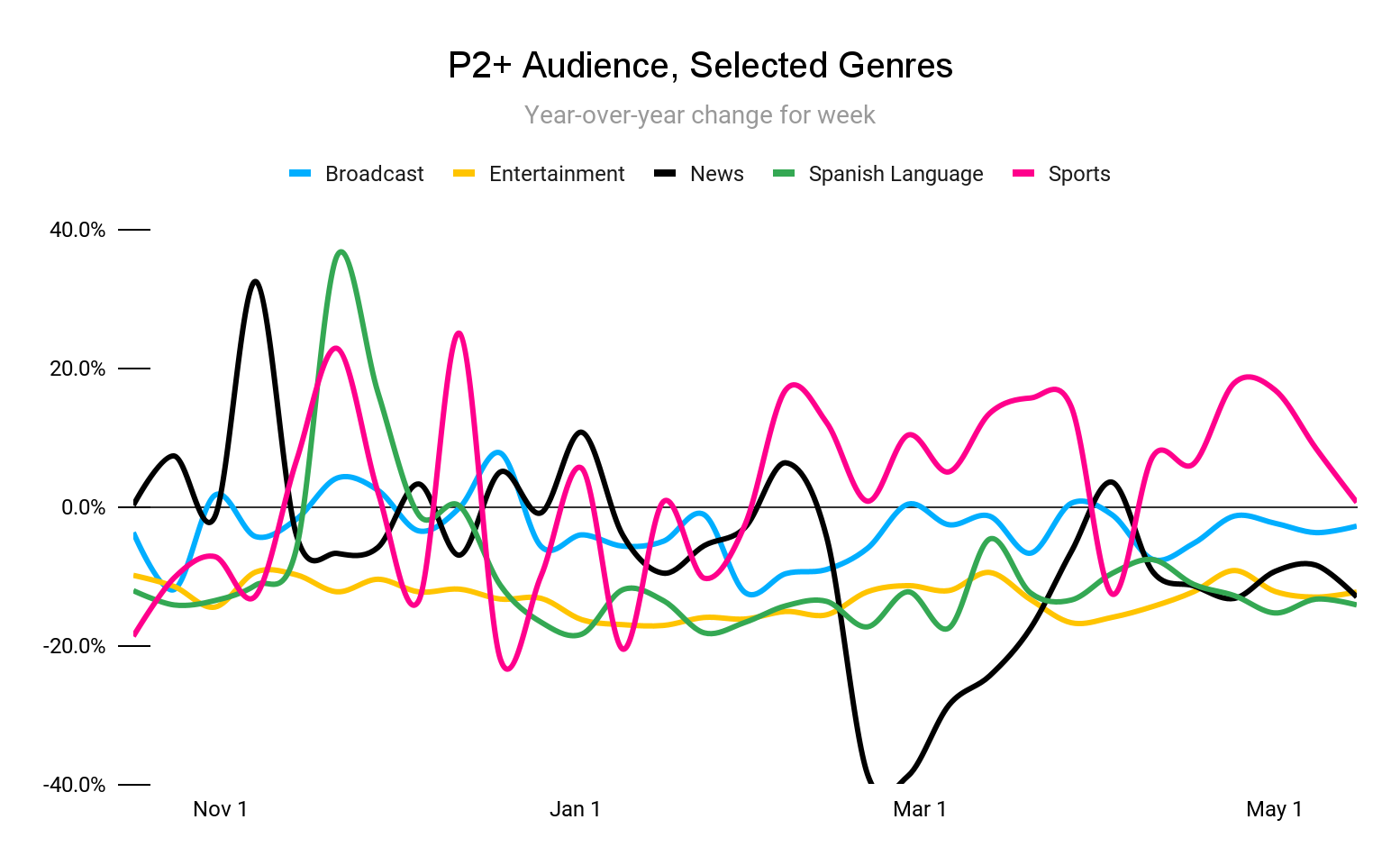

Exciting matchups in the first few rounds of the NBA playoffs produced an increase in YoY viewership at the end of April/beginning of May, but that has since leveled off.

Industry Notes

1. We typically feature Nielsen’s The Gauge in the streaming section, as the rise in streaming viewership and competitive dynamics between those players cause notable changes in viewership share. However, this week, good old-fashioned cable made the story: cable increased its share of viewership again in April, rising 0.4 points, the first back-to-back increase since The Gauge was created in May 2021. The gain is attributable to a strong news cycle, including President Trump’s court appearance, which caused major daily usage spikes for CNN, FOX News and MSNBC. News was the only cable genre that did not decline in usage MoM. Overall cable content viewership is still down on a YoY basis, having fallen 5.3 share points. | Nielsen

We’ve bled a lot of ink in this newsletter on the decline of cable television and the crucial role that sports play in keeping it alive. If we think of the cable bundle as being supported by three types of content (live sports, live news, and live entertainment), it is easy to understand why the fall of any of these pillars would be catastrophic to the model. In the story of sports, we’ve seen how streaming companies have been chipping away at linear TV’s exclusive hold on sports content: DirecTV lost NFL Sunday Ticket to YouTube TV, TNF is on Amazon Prime Video, the RSN system is in major trouble, Apple TV+ owns the broadcast rights to MLS for a decade, etc. The sports marketplace has become more fragmented than ever before as leagues and media companies have been experimenting with different strategies to capture the revenue lost from cord-cutting.

It is not totally surprising that ESPN has already begun talking with its cable partners and securing flexibility in order to bring the channel directly to consumers. Rumors indicate that this will occur sometime in the next few years, but Disney has not publicly revealed anything – after its last earnings call, Disney CEO Bob Iger stated that it hadn’t changed its position regarding the transition, which was that it would happen eventually. It is not self-evident that this would mean the death of the cable bundle – it is more than likely that ESPN would still remain a part of the bundle, and cord-cutters could access the channel via ESPN+. But to be sure, this would represent a monumental shift in the television industry and would tip the scales towards streaming.

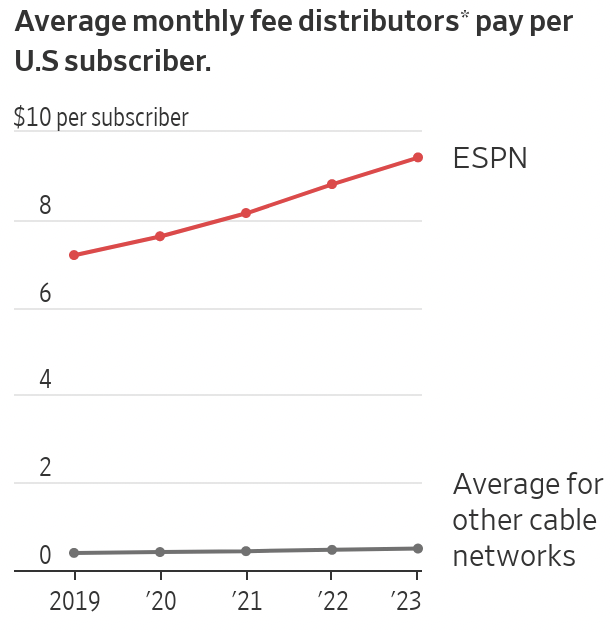

Why? Because ESPN is not just another cable channel. It is so valuable that cable providers pay nearly $10 per subscriber per month in carriage fees to include it in the bundle. This is 20X the average that other cable networks earn. With ESPN, Disney is able to negotiate for its whole family of networks, which has been very profitable for the company. But without the draw of ESPN exclusivity, there is serious concern that Disney networks would bring in significantly less revenue.

The challenge for Disney and media companies alike, is that the economics don’t clearly make sense for streaming. Streamers have found that their investments in sports broadcast rights were disproportionately large, overestimating consumers’ willingness to pay. Hence the bundling and consolidation that has rapidly occurred in the streaming space. While we are still very much in the “wait and see” phase, of all the dominos that could initiate the end of cable as we know it, ESPN is the most important to watch. | WSJ

1. By now you’ve likely heard about the writers’ strike in Hollywood, involving over 11,500 members of the Writers Guild of America (WGA). The strike has had an immediate impact on the advertising space, particularly on linear TV shows that rely heavily on fresh content. Due to the shockwaves this strike can send through production schedules, it seems that original programming will be limited, particularly in daytime and late night dayparts. Late-night shows went dark when the strike began, and networks are already planning for a fall TV season with mostly unscripted content: ABC’s fall primetime schedule currently does not contain any original content that is not in reruns.

Networks have also begun pushing original programming back in the year to maintain some level of original content. This has the potential to put stress on areas like network news and sports, as advertisers search for places to secure high audience delivery.

The last WGA strike (2007-08) lasted 100 days. According to Insider Intellegience’s principal analyst, that strike had a relatively light impact on ad spending. While the strike looms over the Upfronts, networks are asserting that they are better positioned to handle a delay in original content than before due to their streaming offerings, which boast deep catalogs of content. With ad buyers requesting more flexibility in their upfront ad deals, we could see an acceleration in the migration of TV ad dollars to streaming platforms. | WSJ

2. In February we told you Google had begun rolling out beta-testing of its Android Privacy Sandbox, which can be thought of as the mobile app analog of the Chrome Privacy Sandbox for the web. The next step in cookie depreciation is for Chrome Privacy Sandbox, and Google has laid out a timeline (again). In Q1 2024, Google will disable third-party cookies for 1% of Chrome users, and completely depreciate third-party cookies by the end of that year. In order to allow the ad tech industry to adjust, Google will roll out the Privacy Sandbox API in July of this year and in Q4 users will be able to opt in. As the clock on one of the foundational pieces of the digital ad economy is ticking, the second half of this year will be critical for developers to test and adjust for looming data loss in 2024. | TechCrunch

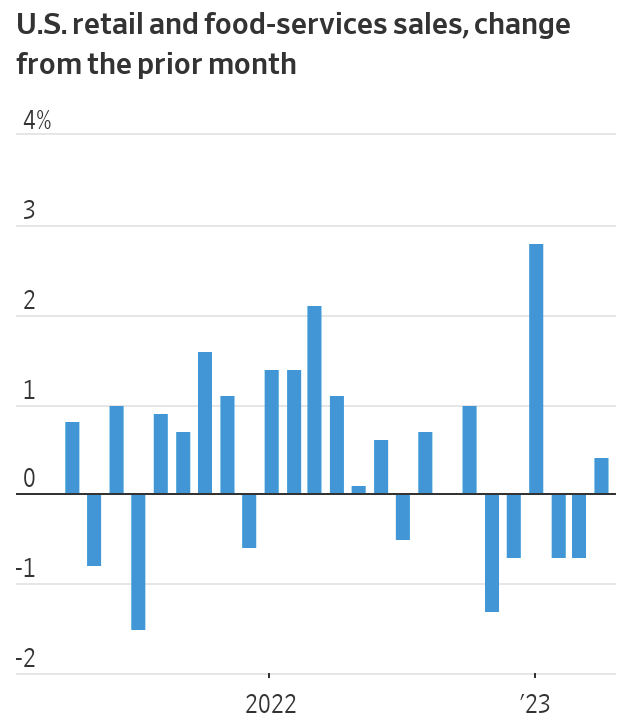

U.S. retail sales rose 0.4% MoM in April, indicating consumers’ resilience to mounting pressures from high interest rates. Like last month, online sales lead all other other categories as consumers cut back on big-ticket purchases.

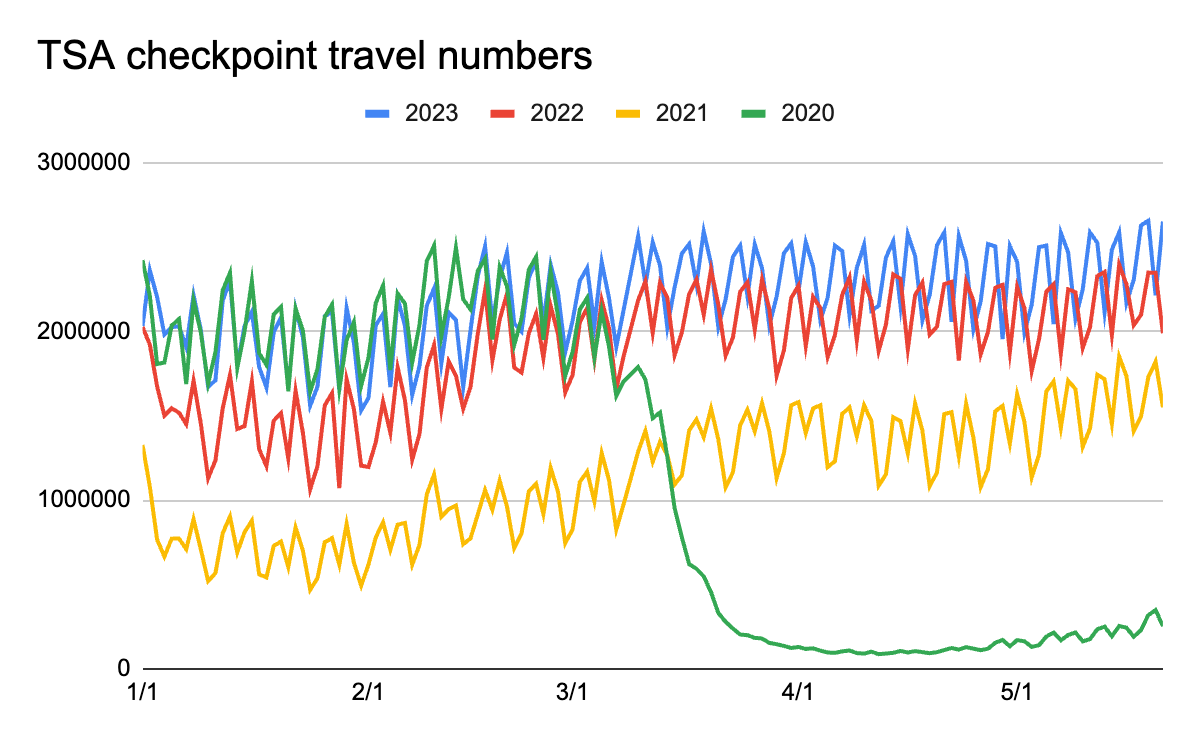

The culprit of this trend is clear pent-up demand for activities that were not possible during the pandemic. In the second half of 2022, traveling had reached the same level of activity as before the pandemic and demand has remained strong in 2023, as indicated by the blue line in the chart below:

The growth of the service sector was further reinforced by S&P Global’s surveys of purchasing managers, which showed that economic activity in May rose to the highest pace in 13 months. While this data bodes well for the health of consumers in the near term, it does complicate Fed’s decision to pause or raise interest rates going forward. | WSJ