Media Update: Women’s NCAA Basketball Viewership, TikTok Notes, and Introduction of New Digital Privacy Law

Sports viewership continued to show strength heading into April, in large part driven by the NCAA women’s basketball tournament. The title game between South Carolina and Iowa drew 18.9M viewers, the most watched basketball game (regardless of gender or professional status) since 2019. Not only did this outpace the men’s title game figure of 14.8M, it rivals the Barbenheimer Oscars’ 19.5M viewers (itself an improvement, which eagle-eyed readers will recall from our March newsletter).

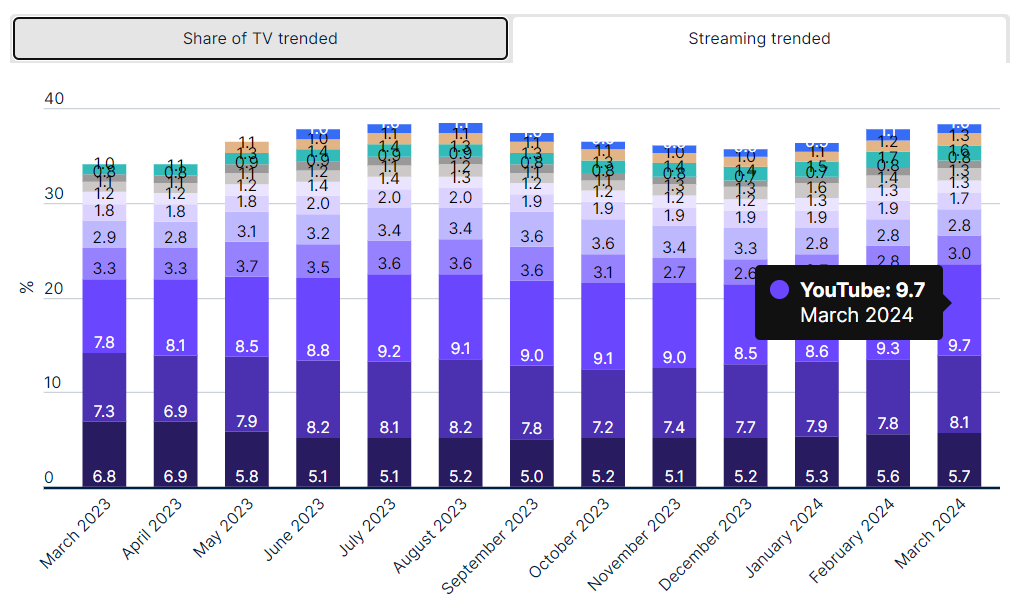

1. Television viewing declined by about 3% in March, consistent with historical seasonal viewership trends for this time of year. Even with March Madness ratings up YoY, factors like better weather, spring break, etc, pulled people away from their TV sets. The largest MoM decline was in broadcast television, which came down almost a full share point.

Streaming was more resilient MoM, declining just 1% overall and picking up 0.8 points of share. Netflix, YouTube, and Hulu all appear to have contributed to this strong showing, each posting material share gains last month. YouTube continues to (somewhat quietly) dominate the streaming market, notching 9.7% of total viewing, the highest figure it’s reached to date.

As we’ve frequently noted in the past, consolidation is inevitable for the streaming industry, and a YouTube/Netflix duopoly is one of the plausible scenarios. | Nielsen

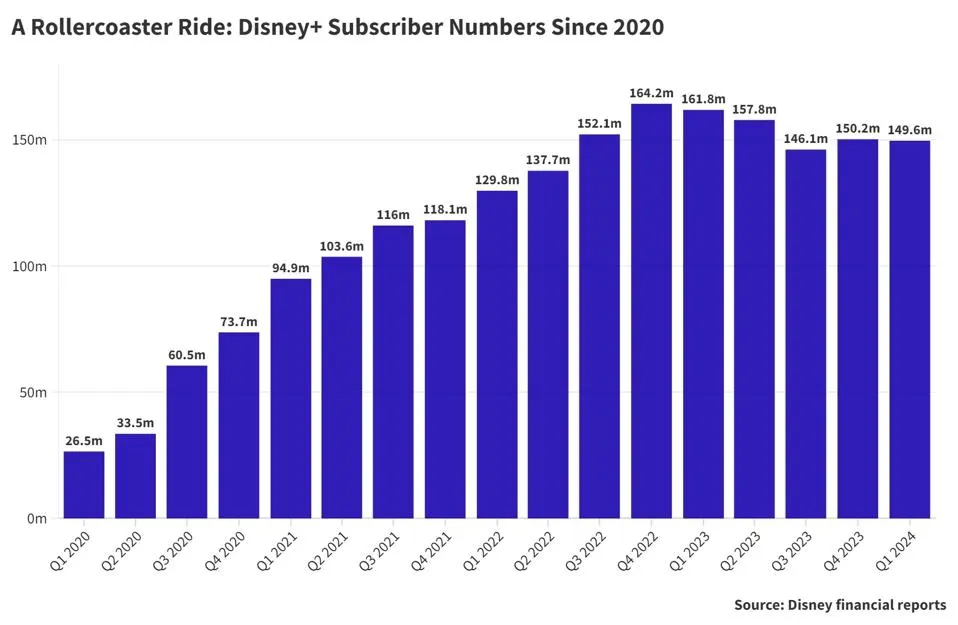

2. We may have covered the rise of streaming sports ad nauseam, but it demands ongoing attention given the scale of disruption underway. Case in point – Disney has announced that ESPN’s DTC streaming service will be bundled with Disney+ in 2025, following the playbook it used last month for Hulu. At the company’s shareholder meeting, House of Mouse CEO Bob Iger said, “This will give consumers the ability to stream their favorite live games and studio programming, and take advantage of an immersive, customizable sports experience that includes betting, fantasy sports, e-commerce, and more… No one has the breadth of what Disney has when it comes to streaming.”

While it is building content breadth and bundles, Disney is highly focused on getting to profitability as quickly as possible. To that end, it announced a crackdown on Disney+ password sharing to take effect this summer. This follows the lead of Netflix, which saw an increase of almost 30M subscribers in 2023 after a similar crackdown. Disney surely hopes the move will reinvigorate its stalling subscriber counts, which topped out in Q4 2022 and have been declining since.

So what does this mean for advertisers? It’s fair to assume that linear cord cutting won’t slow down, especially with the major incumbents betting so big on OTT, meaning audiences of every age and demographic are likely reachable digitally. As such, advertisers of any type looking to access high-impact, engaged audiences will need a robust streaming strategy. Don’t mistake this for the “death” of linear, however; while audiences shift to streaming, linear spot prices are likely to come down, presenting an enticing opportunity for national advertisers looking for cheap reach. | LATimes, CNN, Forbes

3. A hallmark of the streaming era has been a proliferation of content – never before has there been so much available to watch at a moment’s notice. But too much optionality can be its own problem, with viewers regularly spending 10+ minutes searching for something to watch, and ~20% calling it quits when something isn’t found quickly. To combat this, Cineverse is partnering with Nielsen’s Gracenote to launch Cinesearch, a recommendation engine built using Google’s Vertex AI that aims to bring viewers the precise content they want. In a sign of the times, recommendations will come from an AI chatbot, Ava.

We’ve discussed on many occasions the growing presence of AI in the advertising landscape, often relating to ad tech developments and generative creative (such as PMax’s use of Gemini to make creatives). Here, we see that the role of AI will be much broader, impacting viewers and content directly. In the short term, such a tool may increase ad supply slightly by boosting viewership, with viewers less likely to churn during the search process. In the long term, it raises interesting questions about prioritization in the AI era. How will AI search engines prioritize recommendations, which publishers will benefit, and how can advertisers ensure their creative is placed in recommended content? While AI is still nascent, expect more developments on this front in the year ahead. | TheWrap

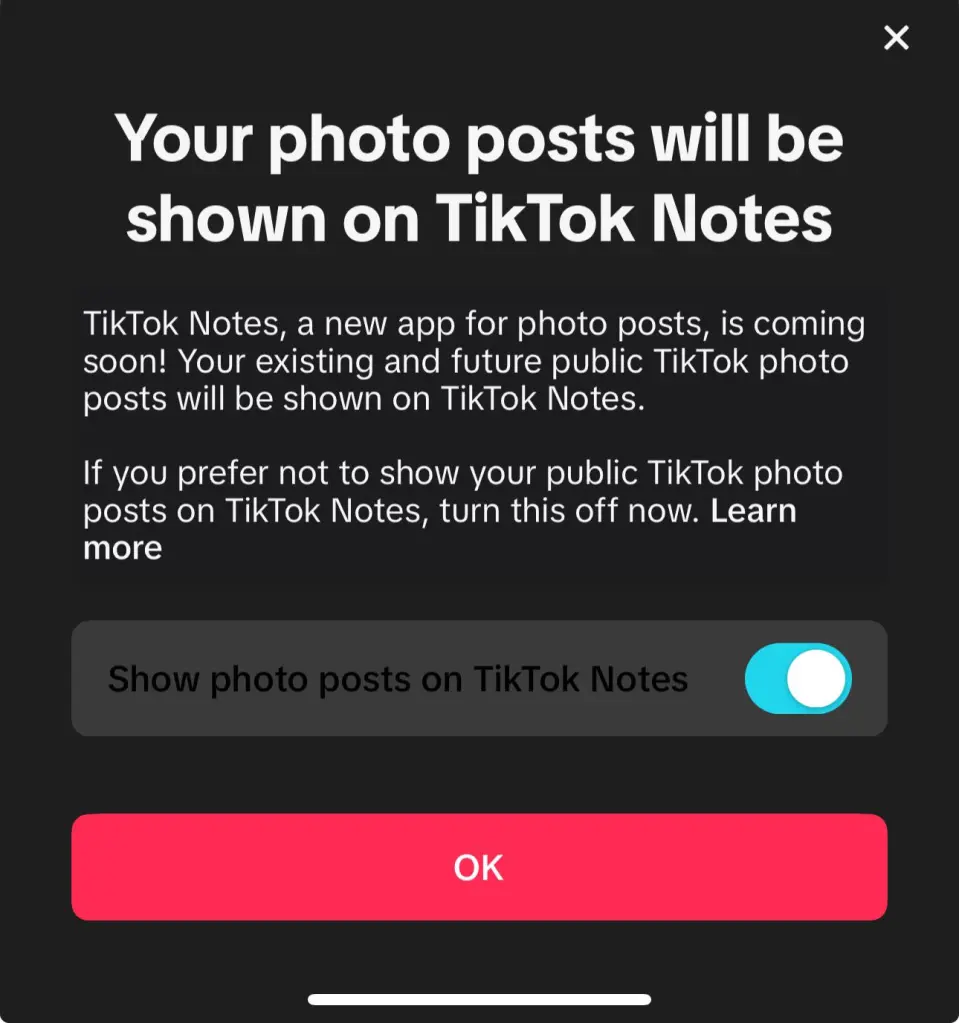

1. In the ongoing battle between social platforms to maintain relevance and grow their user bases, TikTok announced a new app, TikTok Notes. The new app is designed for photo sharing, à la Instagram. This is not the first time we have seen social platforms mimic one another – in fact, it has become commonplace over the past decade. Instagram copied Snapchat’s Stories feature, YouTube Shorts and Instagram/Facebook Reels were born in close succession to TikTok’s meteoric rise during the pandemic, many platforms including Spotify came out with their own AI-powered versions of TikTok’s ‘For You’ Feed, and Instagram released Threads last year to win over former Twitter (now X) users.

Many TikTok users began receiving notifications like the above in their TikTok feeds over the last couple of weeks. While the app is not publicly available yet, TikTok is using these automatic opt-ins to start building content on the new platform before any users officially join. While this will give the new app a jumpstart, there is an uncomfortable fit here with TikTok’s positioning. From its conception, TikTok has always been a video-first entertainment platform. The rollout of TikTok Notes thus seems less like a pivot in strategy and more so a “what else can we do.” We can expect legacy TikTok to remain focused on video-first content, and still be an entertainment hub, while TikTok Notes will live alongside and be a safe space for consumers to share photo and text content.

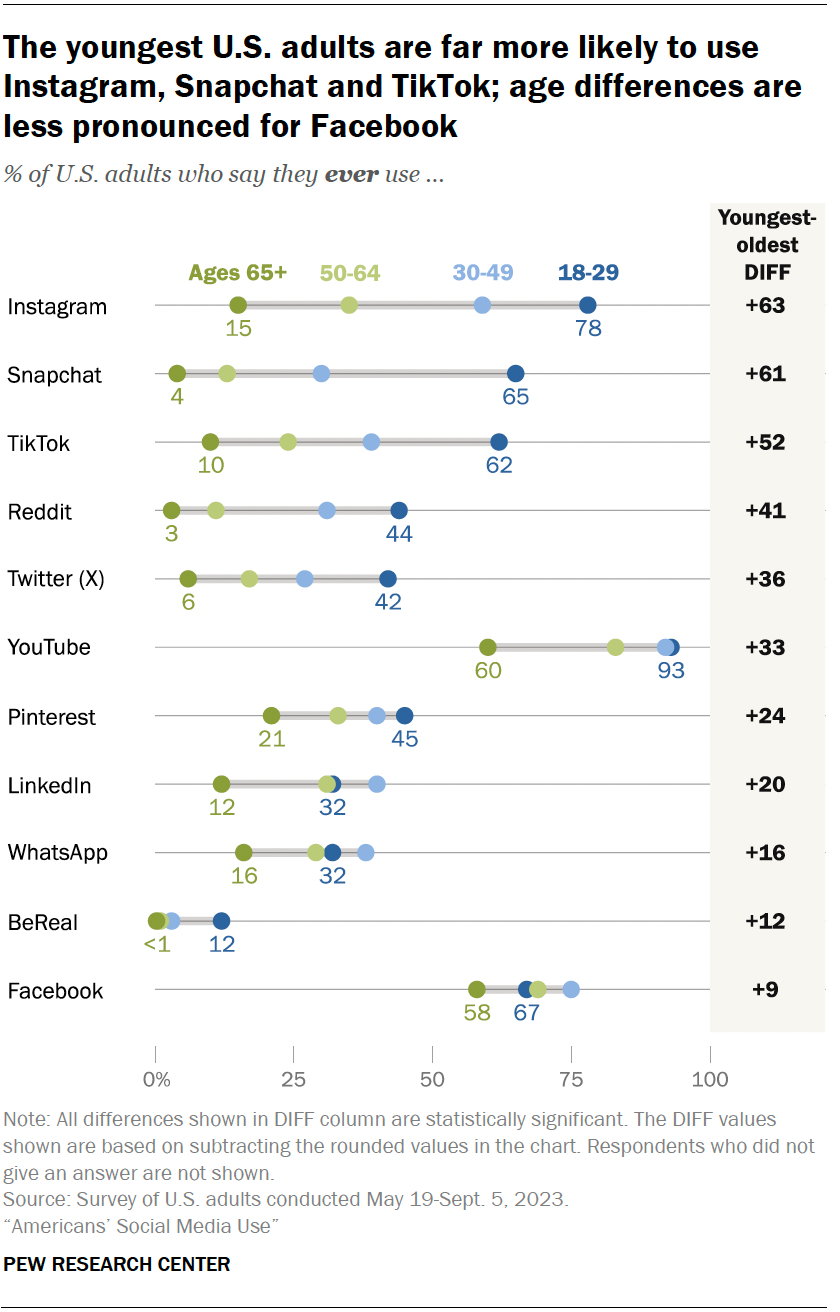

The opportunity for TikTok could be substantial. 78% of Americans aged 18-29 use Instagram, which aligns with TikTok’s core Gen Z demo. While it is too early to know what advertising options will be available on Notes, or if marketers will be able to programmatically bid on inventory across the broader ecosystem, this is a significant development in the industry. If you recall from mid-March, TikTok was making headlines as the US government tried to pass a bill to force a sale. While the bill is still awaiting a Senate vote with no timeline, TikTok has continued business as usual and doubled down on its US presence through the launch of this new app. Time will tell if users switch from Instagram to TikTok Notes, or if there is app fatigue by way of too many social platforms. | Forbes, USA Today, Pew Research

2. Snapchat has long been a leader among social platforms in self-service creative. It was the first to make augmented reality easily accessible to both users and to brands for advertising. As such, it’s no surprise that the company has been an early mover in integrating AI within its platform, including generative AI capabilities and an AI chatbot for users.

Focusing on AI creative, a significant update has been released for image outputs – now all Snap creative will feature watermarks, including a custom ghost icon on images generated in the app.

Snapchat highlights that the addition of the watermark increases transparency and will help users recognize when an image is AI-generated. Included with the watermark rollout is some additional callouts within the generative AI toolkit, cautioning users to “not assume generative AI outputs are true or depict real events. Generative AI…may be incorrect, inappropriate, or wrong.”

What this all means for advertisers is that Snapchat is making an effort to protect itself from liability. It is also taking steps to actively prevent any misuse of its tool set, e.g. generating content and repurposing it on other platforms without giving Snapchat credit. Whereas this has been a common practice in the past with brands repurposing 9×16 content across Meta, TikTok, and Snapchat, brands will need to be more careful about usage rights for any generative AI content in the future. | Social Media Today

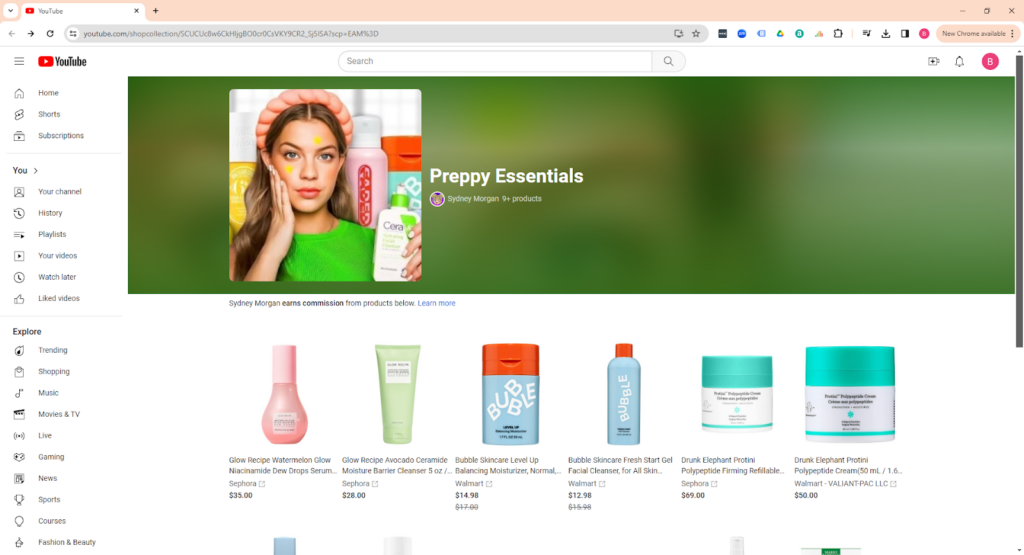

1. Last month, we talked to you about YouTube developing a TV viewing experience that is “uniquely YouTube,” incorporating features such as comments and shopping elements into the experience. This month, we lean more into the shopping element and surface YouTube Shopping’s latest features release.

YouTube Shopping was launched as a way for creators to sell products from their line or from other brands on their YouTube channel. The latest round of features is designed for creators to more easily promote products throughout their channels and provide viewers with a more streamlined shopping experience on the platform.

Two noteworthy new YouTube features are Shopping Collections and the Affiliate Hub.

The features release comes on the heels of YouTube-released data that over 30 billion hours of shopping content were watched on YouTube in 2023. For perspective, that equates to 3.4M years of watch time.

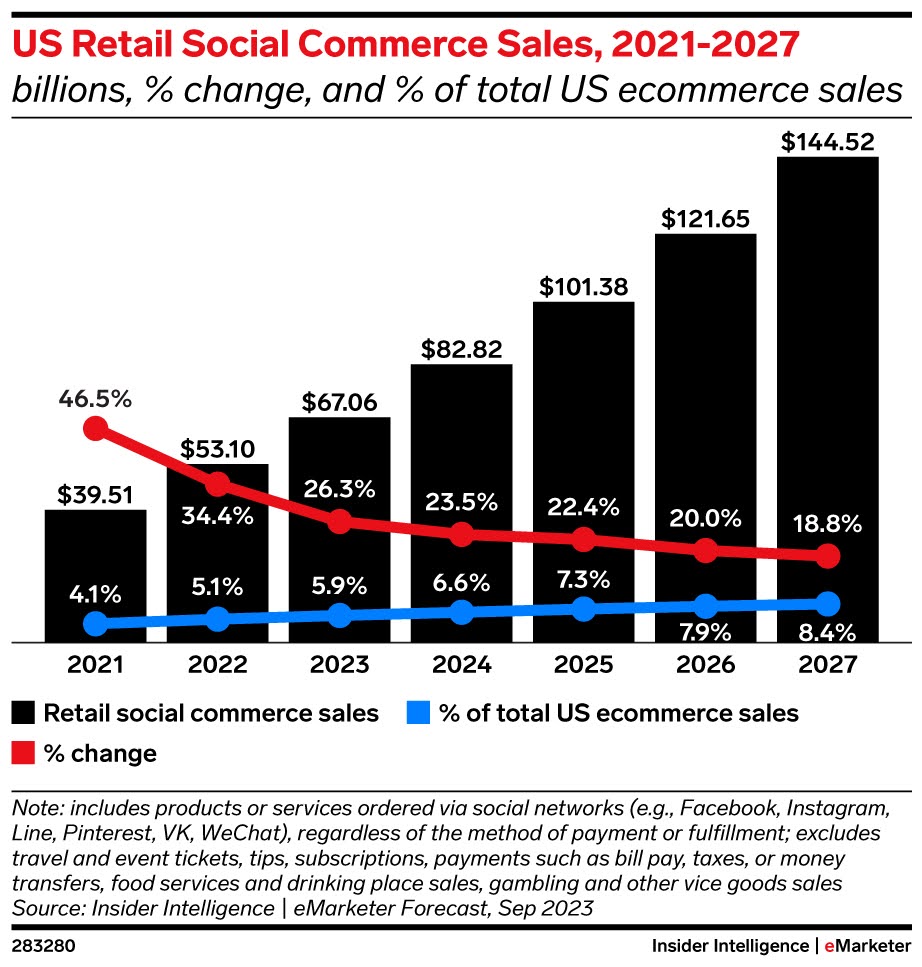

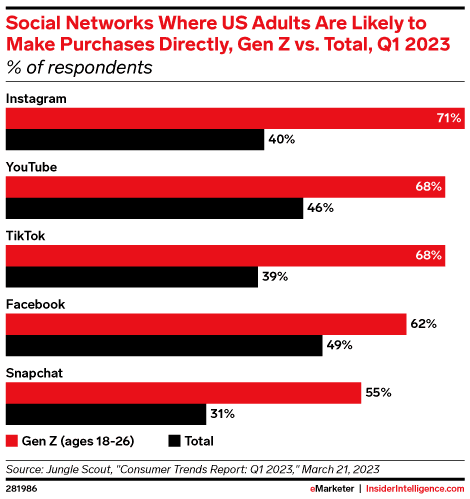

The frequent updates to enhance the on-platform shopping experience reaffirm YouTube’s endeavor to capture a larger share of the growing social commerce market. eMarketer forecasts social commerce sales will grow to $144B by 2027 and notes that YouTube is positioned well to capture the demand as viewers, particularly the Gen Z audience, are more likely to purchase on YouTube than most other social platforms.

While YouTube Shopping is still evolving and not open to all creators or brands, YouTube’s push to capture more of the growing social commerce sales will open up more opportunities for creators and brands to transact directly with viewers. | YouTube Blog, Google Support, YouTube Blog, eMarketer

There have been several important developments on the privacy legislation front recently, headlined by a bipartisan digital privacy bill released by the Commerce Committee chairs of the House and Senate, respectively. The American Privacy Rights Act will, according to its authors, set “clear, national data privacy rights and protections for Americans.” If enacted in its current form, the legislation would override state-level privacy measures; it would allow Americans to opt out of targeted advertising; and it would create a private right of action to sue violators.

Those of you who follow this space know that national privacy legislation has been a hot topic for years, as the hodgepodge of inconsistent state-level laws makes it increasingly complex to operate digital platforms at scale. Two years ago we highlighted Google’s call for a national privacy law, arguing that consumers are overwhelmingly in favor and Congress needs to act. And since that time, things have become even more complex:

Last year, the state of Washington passed the My Health My Data Act, which came into force in March for larger businesses and will come into force in June for small businesses. This legislation broadly restricts the use of any health data in advertising, and creates a private right of action for consumers who believe their statutory rights have been violated. This latter fact has created concern that a flood of litigation could be unleashed.

This month, the Maryland legislature passed two sweeping privacy bills, which will become state law if signed by Gov Wes Moore. The two bills are the Maryland Online Data Privacy Act, which would impose wide-ranging restrictions on how companies may collect and use consumers’ personal data in the state; and the Maryland Kids Code, which would prohibit certain social media, video game and other online platforms from tracking people under 18 and from using various techniques — like auto-playing videos or bombarding children with notifications — to keep young people glued online.

The federal legislation remains highly uncertain – it has not been voted on by either house of Congress, and much of the substance could change in the legislative process. As it progresses, lawmakers ought to be mindful of the effects we’ve seen play out from privacy measures in the past several years, including:

The lesson, which we should all know already, is that policy is complex and unintended consequences are par for the course. If we do get a national digital privacy law in the U.S., let’s hope it incorporates the lessons from recent history. | The Hill, eMarketer, NYT

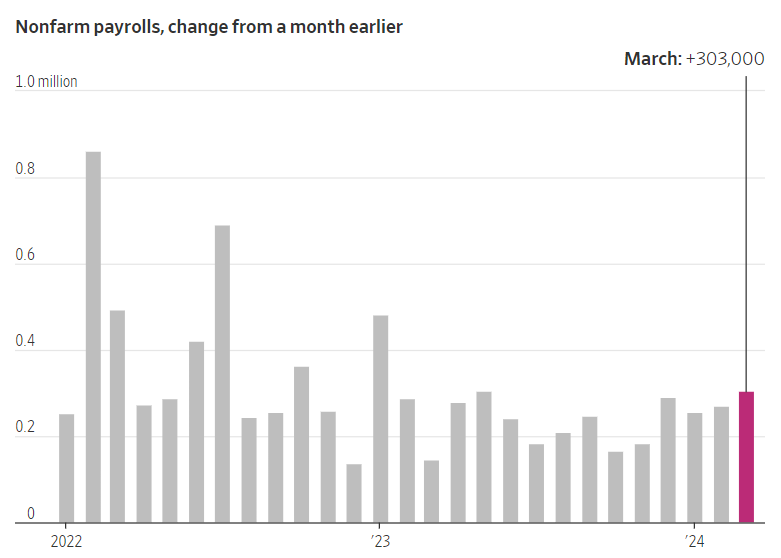

1. The Labor Department released its latest jobs report, which revealed that U.S. employers added 303k net jobs in March, significantly surpassing the consensus forecast of 200k (take the 303k figure as tentative, as several recent jobs figures have been subsequently revised downward). The official unemployment rate fell from 3.9% to 3.8%, continuing to hover near historic lows.

A closely watched figure in recent jobs reports is wage growth, given its connection to price inflation and thus to interest rates. High (nominal) wage growth has generally been seen as a negative, as it implies inflation is too high and will force the Fed to keep interest rates elevated. March’s data show average hourly earnings rose 4.1% YoY, the slowest rate since June 2021.

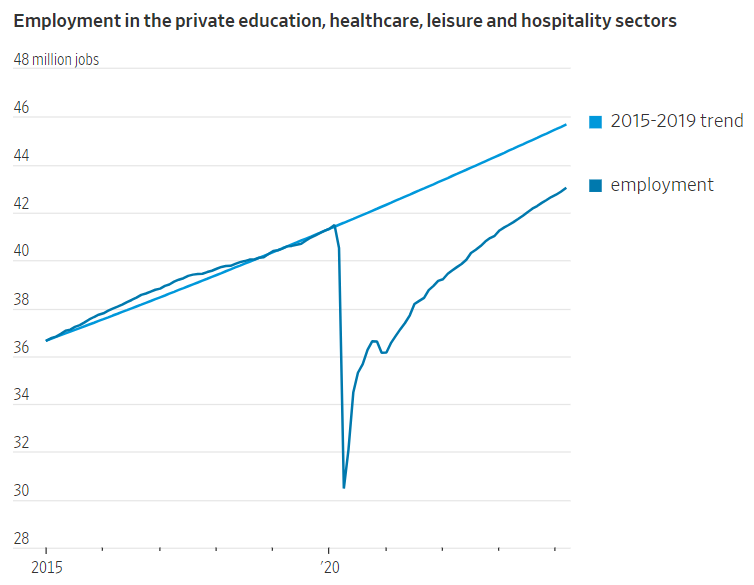

The biggest industry contributors to March’s employment gains were healthcare, private education, and leisure & hospitality, which have produced more than half of the job gains in the past year. These are all “high touch” sectors, i.e. those where lots of in-person, face-to-face interaction is part of the job. They were hit especially hard during the pandemic, and may still have significant catching up to do:

Markets welcomed the jobs figures (all indexes were up), and the Fed has stated explicitly that employment growth per se will not be a brake on interest rate reductions. | WSJ

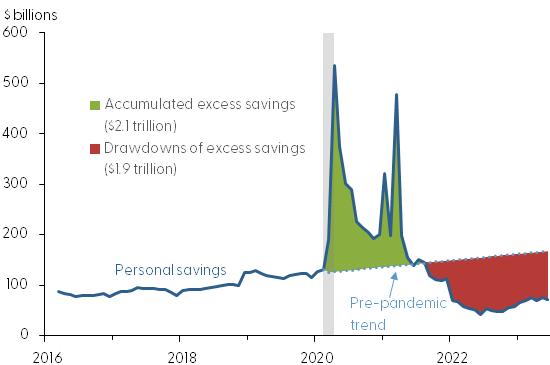

2. This time last year we told you about the massive drawdown in pandemic savings – while we were all cooped up in 2020 and ‘21, Americans saved over $2 trillion above and beyond their normal nest eggs. In late ‘21, as the country began to open up, that trend reversed and Americans drew down those savings; by last spring about 90% of the excess savings had dissipated.

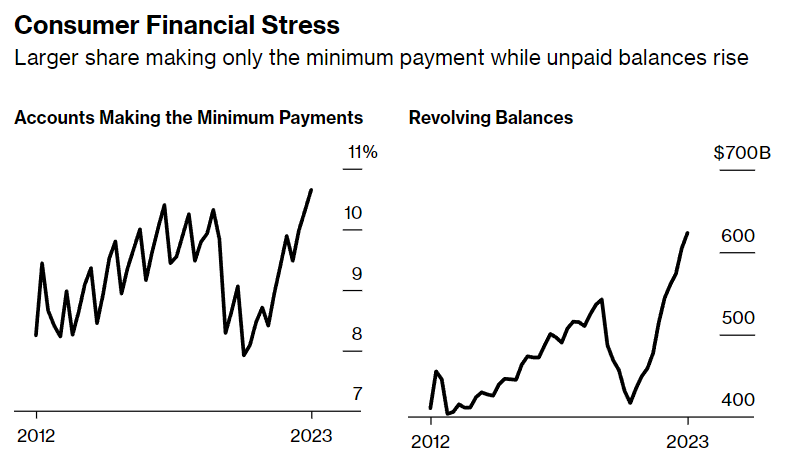

The trend of saving less and spending more has continued, as a new study from the Philadelphia Fed reveals U.S. credit card delinquency rates were the highest on record in the fourth quarter, with almost 3.5% of card balances at least 30 days past due as of December. The fraction of accounts making minimum payments has also increased precipitously, now surpassing pre-pandemic levels.

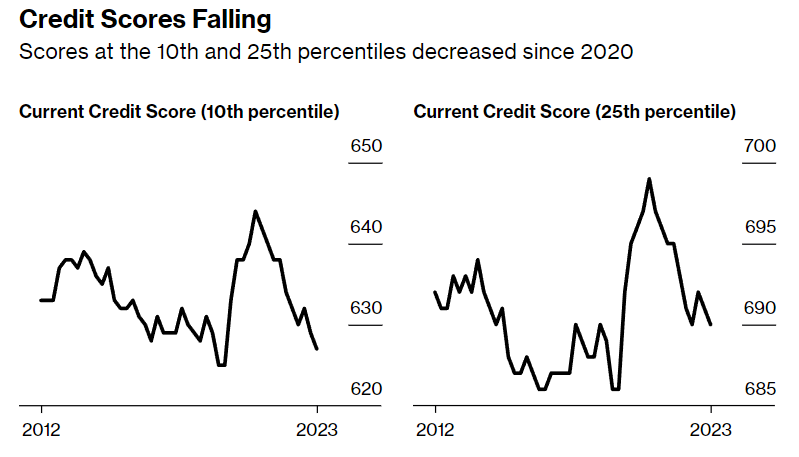

The mirror image of these trends is consumer credit scores, particularly at the lower ends of the credit distribution. Collectively, these data points suggest growing pressure on household finances amid persistently rising prices.

Unsurprisingly, credit issuers have begun to tighten credit standards as delinquencies have risen – the median account opened with a $3,000 limit in the fourth quarter, down from $3,368 in the second quarter. Should interest rates come down later this year, giving consumers even less incentive to save, we could see credit utilization rise even further. | Bloomberg, Philadelphia Fed

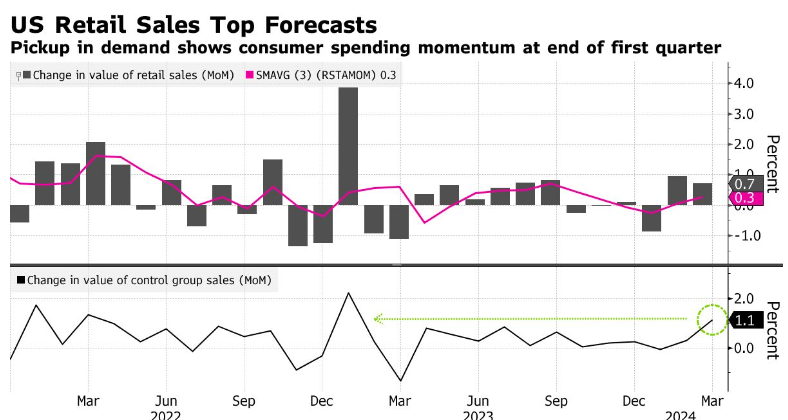

3. Underneath those rising credit card balances is brisk consumer spending – retail sales rose by 0.7% MoM in March, and February was revised upward, making for two months of strong spending growth following a four-month period of flat-to-down spending.

Notably, e-commerce led the way with 2.7% growth MoM, with gas stations the only other category cracking 2%. Clothing stores were at the other end of the spectrum, contracting 1.6%. The continuing strength of the labor market (see above) is no doubt underwriting this resilience in consumer spending, but growing indebtedness and rising credit delinquency rates are clearly concerning and suggest consumers will have to moderate consumption before too long. | Bloomberg