Media Update: Discovery+ Stays Standalone, Google YoY Ad Revenue Decline, and 517k New Jobs In January

Ad-supported video supply hasn’t moved much recently, continuing to hover at about 2x its level of 18 months ago.

Industry Notes (Video)

1. Back in the summer we told you about Warner Bros Discovery’s plans to merge HBO Max and Discovery+ into a single, combined platform, and in November we told you about an accelerated timeline to roll out the new service in spring 2023. A streaming “super bundle” was indeed a central strategic plank of the companies’ $43 billion merger last year. Now, in a significant shift, WBD has partially reversed course and will maintain Discovery+ as a standalone streaming platform.

In a time of intense financial pressure on major streamers, this decision goes against some trends we’ve seen recently; you may recall our discussion last week of Paramount combining Showtime and Paramount+ in an effort to rein in costs. WBD’s logic seems to be that the 20m people who subscribe to Discovery+ today may be alienated by being asked to pay more for new content they were never interested in (welcome to bundling!), and thus Discovery+ will be “left alone” to prevent those subscribers churning out. The new, soon-to-be-renamed HBO Max will include most Discovery+ content, so WBD is not abandoning the bundling logic altogether.

From the very beginning, we’ve highlighted that WBD has a tricky brand identity problem with two assets at opposite ends of the programming spectrum. Recall this graphic, wherein WBD attempted to square the circle:

It seems this conflict has not been resolved entirely, and WBD’s solution (for now) is to avoid pushing consumers into its bundle too aggressively. | WSJ

2. 2022 was a big year for many streaming companies, with the adoption of advertising, major bundling, and price increases shaking up the industry. While most streamers were a bit more cautious of their bottom line last year, Amazon stood apart, choosing instead to ramp up its content investment and diversify its streaming portfolio. Prime Video spent more than $16.6 billion on content in 2022, with ~$7 billion going to original content, putting it virtually on par with Netflix. The biggest contributors to Amazon’s spending were LOTR: The Rings of Power (~$500 million for the first season) and Thursday Night Football (~$1.2 billion/year). The former, although sometimes described as a pet project for Jeff Bezos, became Amazon’s most watched TV premier and surpassed 100 million viewers for the entire season. TNF might be considered a success as well, as it drove the largest single day of Prime sign ups in its season opener, despite soft viewership in the season overall.

The company is spending big to acquire and retain subscribers, which is standard practice in the industry. Except, Amazon is not just in the streaming business – with a $14.99/mo Prime membership, subscribers get a stupendous number of benefits. The question Amazon must answer, as it advances into the streaming space, is if it can justify holding the Prime package together at the current price point. Cracks are already beginning to show: last week the company announced that subscribers would have to spend more money per order to get free grocery delivery. Most streaming companies are hemorrhaging money, losing billions each year just to provide video content, whilst charging the same amount as Prime. Given the plethora of additional features that come with a prime membership, it is difficult to imagine that Prime Video is yet a profit generator for Amazon.

As we’ve heard from streaming companies this year and last, the level of content spending in the industry is wholly unsustainable. With further consolidation in the industry, there should be some downward pressure on content costs as a result of normalizing competitive dynamics – this should help rightsize the streaming business model. | TechCrunch

3. Rumors are brewing that Disney is looking to license its library content to other media companies, as its “content sales/licensing and other” business segment reported a 86% increase in operating loss for the quarter ended December 31. This strategy should sound familiar – just last week Warner Bros. Discovery signed deals with Roku and Tubi to bring its library content to consumers via free ad-supported TV (FAST). In fact, many of the issues that plague WBD/HBO Max/Discovery+ are similar to those at Disney. The Mouse House experienced its worst stock market results in decades last year, posting billion-dollar quarterly losses in its online video unit, as did WBD. Disney is undergoing major strategy and leadership changes with Bob Iger’s return, as WBD is still restructuring with its merger. Both streamers are desperate to increase profitability, and are willing to sacrifice some of the exclusivity of their platform and content in order to achieve it.

This raises the question: is this the beginning of a resurgence in content licensing? It certainly stands to reason that platforms that have reached scale reap little incremental gain by hoarding library content rather than licensing it to other streamers. Back in the early days of streaming, when Netflix wasn’t considered an existential threat to the media companies, licensing content was an accepted endeavor. It was only when the decline of cable became more pronounced, and when companies launched streaming platforms in a frenzy, that hoarding content was employed as a strategy to attract subscribers. And so the pendulum swings.

While the battle over library content might be cooling off, it seems apropos to discuss Sony, one of the only media companies to forgo the creation of its own streaming platform. This has turned out to be a very fruitful decision – the company earned over $3 billion in revenue in 2021 from producing television content and is projected to exceed that amount for FY 2022. Even further evidencing the success of this model, Blackstone-backed Candle Media is building its business on acquiring/producing content and licensing it to streaming platforms that are desperate for hits that will attract audiences.

As Disney mulls its most recent quarterly results, wherein it gained only 200,000 domestic subscribers and laid off 7,000 employees, it may see content licensing as a quick financial win, and as a valuable strategic pivot from a fully integrated content & distribution model. | Bloomberg, WSJ

4. Speaking of Tubi, the FAST service notched another quarter of strong growth at the end of the last year, with total viewing time (TVT) in December reaching a monthly high. Seemingly unaffected by the advertising slowdown, Tubi’s December quarter ad revenue grew 25% YoY and ad revenue over the entire fiscal year grew by approximately 45%. Tubi’s remarkable success in 2022 is owed not only to its very friendly price point, but also to its vast content library, which includes a wide variety of programming and was further improved by the addition of WBD content this month. Unlike other media companies, Fox does not have its own subscription-based DTC streaming service, instead licensing its primetime content to Hulu, with which it just extended a multi-year partnership over next-day broadcast rights. Although Tubi’s inventory is less premium because of this, the service has still clearly found its audience. | The Wrap

All linear genres are down on a YoY basis once again, with broadcast viewership ticking down considerably last week.

Industry Notes

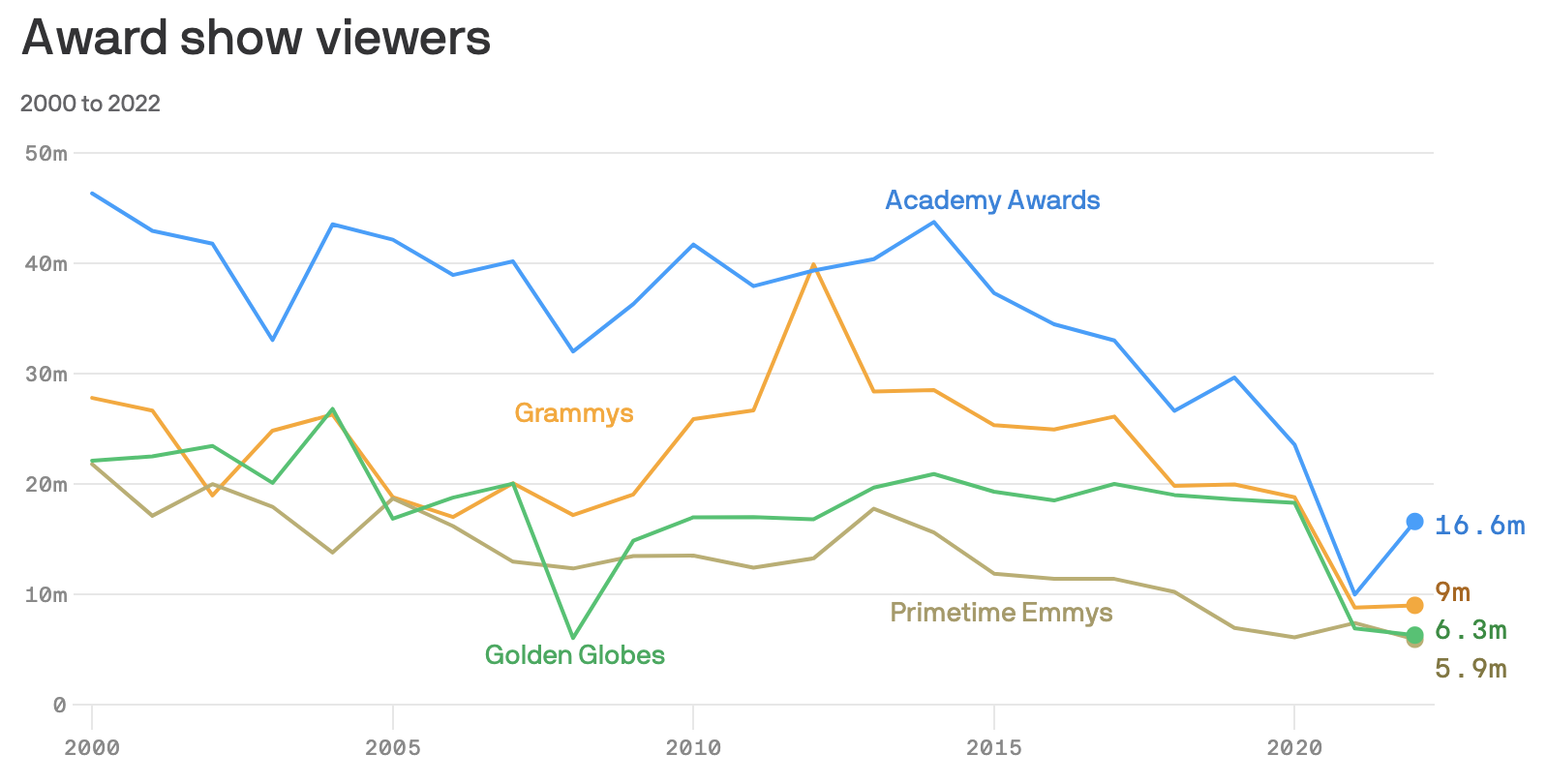

1. The Grammy Awards posted a surprising 30% YoY gain in viewership over the weekend, averaging 12.4 million viewers across CBS and Paramount+. This represents the largest bump since 2012, when viewership peaked at 40 million. As we head into award season, it’s important to note that viewership for these tentpole events, although far below historical levels, is still significant on linear television. Outside of sports, the Grammys were the most watched primetime program this year. Additionally, this was Paramount+’s largest live streaming audience in history. While viewership in these award shows is not likely to rebound significantly, streaming could play an important role in revitalizing this programming. | Variety

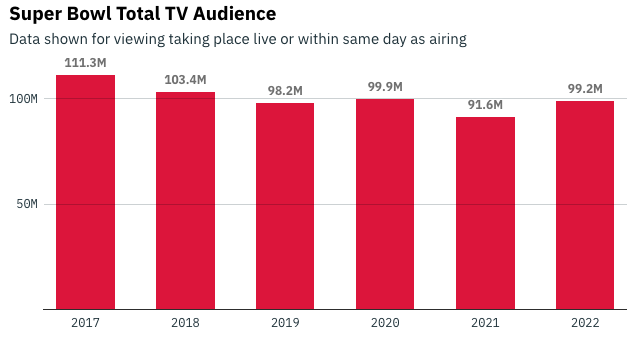

2. Just a week before the big game, Fox has announced that it sold out its Super Bowl inventory, grossing just shy of $600 million in revenue, a big leap from the estimated $500 million that NBCU pulled in last year. Like last year, several 30-second spots went for as much as $7 million, with the majority coming in at the mid to high $6 million range. Although buys came in a bit later, Fox is not seeing a significant slowdown in advertising revenue. This Super Bowl is expected to draw a strong audience (potentially over 100 million viewers) for a couple reasons: firstly, Fox will not be multicasting with a SVOD service, so essentially all viewership will come in via linear. Contrast this with recent years, in which NBC multicasted on Peacock and CBS multicasted on Paramount+. Secondly, last week we saw conference championships viewership reach its highest level since 2014. Whether you watch for the football or the commercials, this is gearing up to be an exciting Super Bowl Sunday. | Adweek, Variety

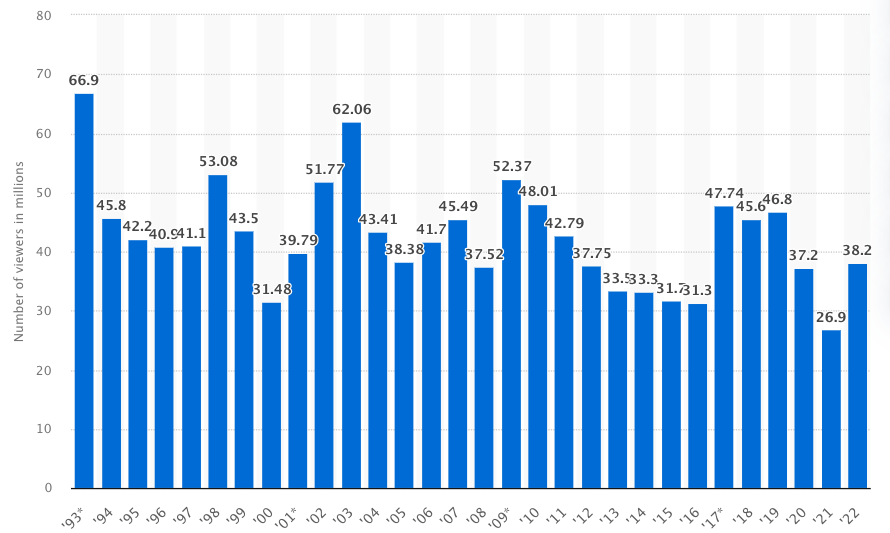

3. President Biden’s State of the Union (SOTU) address brought approximately 27.3 million viewers, a decline of 29% versus last year. While that fall in viewership may look bad, it is fairly consistent with the downward trend observed over the past few decades, in line with the steady decline of linear television. Viewership might have also been affected by the concurrent broadcast of the Lakers-Thunder game, in which 3 million viewers tuned in to watch Lebron James surpass legend Kareem Abdul-Jabbar as the the most prolific scorer in pro basketball history. | Deadline

1. Following Snap’s downright poor Q4 results last week, and Meta’s not-great-but-better-than-expected numbers, it was the turn of the other digital ad behemoths to show their cards. Google announced Q4 numbers that reinforced the notion (if any reinforcement were needed) of a digital ad recession – total advertising revenue declined by 3.6% YoY, with the search business declining 1.6% and YouTube declining 7.8%. These figures are notable for many reasons, not least that it is only the second time in Google’s life as a public company that ad revenue growth has been negative; the only other time was Q2 2020, owing to the onset of the coronavirus pandemic.

Also notable is what these numbers say about what’s going on under the surface of the advertising economy. When the froth of 2020 – ‘21 began to subside in February last year, Google was much better positioned than most of its rivals: as marketers became more cautious and reined in their investment, Google benefited from a flight to quality, i.e. marketers’ tendency to stick with tried and true bottom-funnel investments while cutting upper-funnel media, experimental channels, etc.; and Google search in particular was highly insulated from the impact of ATT (contrast search with YouTube below, which is impacted by ATT), the privacy policy from Apple that kneecapped many of Google’s competitors and arguably triggered the digital ad recession single handedly.

With ATT off the table as an ‘excuse,’ and the tremendous advantages of being the world’s default search engine baked in, the revenue decline is unambiguous evidence of secular retrenchment.

A final note on YouTube – we’ve discussed numerous times the amazing strides YouTube has made in an ultra-competitive streaming marketplace:

Given this growth in share – and bearing in mind that the total pie grew by about 10 points of viewing share Q4 to Q4 – YouTube’s revenue decline is all the more noteworthy. Google does not publicize average CPM’s for its properties, but it would certainly seem a fair inference, and consistent with our internal data, that YouTube CPM’s have come down materially. | WSJ

2. Next up was Amazon, which posted YoY growth of -2% in its core ecommerce business and 19% in its advertising business, commenting, “We do expect to see some slower growth rates for the next few quarters.”

Amazon has been one of the major advertising stories of the past few years, as we discussed at some length in the Amazon Ads IPO. Its ads business brought in $11.5 billion in Q4, still well shy of Google’s $59 billion and Meta’s $31 billion, but well meriting its inclusion in the so-called triopoly; and its 19% growth rate is significantly higher than Google’s (-3.6%) and Meta’s (-4.5%). Similar to our discussion of Google’s search business above, Amazon’s is notable for being largely immune to the impact of ATT due to its emphasis on search ads, and the fact that it often has an on-platform closed loop (i.e. its platform is the surface for both ad exposure and transaction, obviating the need for an identifier like an IDFA). Similar to Google’s search business, Amazon has thus been a beneficiary of Apple’s policy update, as marketers have shifted dollars away from platforms (Snap, Meta, YouTube) that have been heavily impacted.

Perhaps ironically, Amazon is aggressively pushing into the kind of upper-funnel ads that have been less resilient in the digital marketing recession of the past year. The argument in favor of this expansion is that Amazon is much better placed to understand upper-funnel ad impact than, for example, a television network, given the vast quantity of signals it collects from consumers and its ecommerce platform’s focal point in the retail landscape. | WSJ

3. Finally, Apple reported revenue growth of -5%, its first quarterly revenue decline in nearly four years. iPhone sales, which represent more than half of total revenue, declined by 8%, which the company attributed to manufacturing disruptions in China related to the country’s Zero Covid policy. CEO Tim Cook remarked that “the wind was in our face for the fourth quarter.” Join the club Tim!

Apple does not break out results for its advertising business, grouping them with its Services business line that includes things like the App Store, Apple TV+, AppleCare, etc.; that segment of the business grew by 6%, making it the only division apart from iPad (don’t ask us) to report positive growth. | WSJ

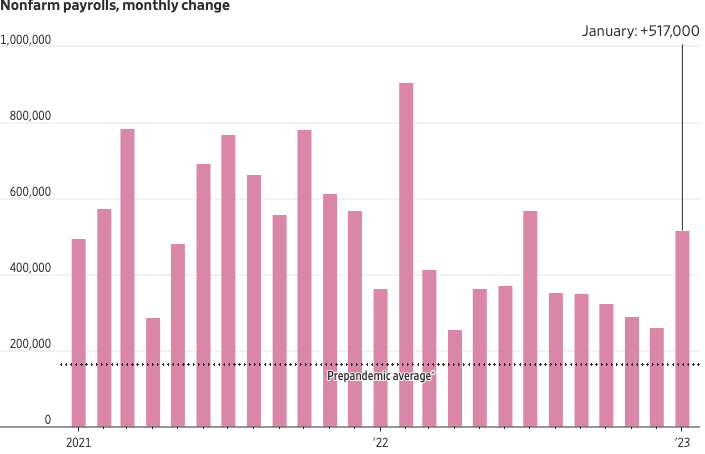

In a surprising report, the U.S. labor market added 517,000 jobs in January, a sharp spike compared to the last 5 months of around 300,000 jobs, and despite tech layoffs, unemployment fell to a 53-year low. This shocking news has reignited debates over the Fed increasing interest rates, which are designed to tamp down inflation largely by cooling down the labor market. With this strong jobs report, it seems likely that the Fed will increase rates again.

On the flip side, the jobs report also revealed that wage growth continued to slow, albeit at a less rapid pace. Average hourly earnings grew 4.4% in January YoY, down from 4.8% in December and below the rate of CPI inflation. With nearly two jobs available for every unemployed person looking for work, we might expect to see wage growth remain relatively steady in the upcoming months. | WSJ