Media Update: May Upfronts, YouTube Shopping, and Agentic Commerce

1. Drip, drip, drip – the linear audience base continues to erode. With the exception of a small bump for sports in the week of May 12th (which benefitted from the Knicks-in–Six conference semifinals win), every major linear category has been down year-over-year since late April. In Nielsen’s latest Gauge, linear’s share of total TV viewership came in at a paltry 45% (compare that to the 63% figure linear boasted just four years ago).

2. May: the weather is warming, the flowers are blooming, and TV buyers celebrate by cramming into theaters and event spaces to eat canapes and watch celebrities shill new media. This month was upfronts & Newfronts, and nearly every major media publisher and tech company descended on New York to showcase their latest products in search of investment for the 2025-26 broadcast season. While the events themselves are decidedly over-the-top, they also are an unparalleled way to gauge where the industry is headed, this year and beyond.

The most apparent theme across nearly every upfront event in 2025 was the singular importance of live programming, particularly sports. NBC led the charge by promoting a slew of live events, repeatedly touting what it’s dubbed “legendary February”, a stretch next year that will include the Super Bowl, Winter Olympics, and NBA All-Star Game. Fox countered by hawking the 2026 World Cup and a healthy amount of NFL coverage; Disney trotted out Jason Kelce and Patrick Ewing to promote Monday Night Football and the NBA Finals; Amazon brought on Blake Griffin to showcase its new NBA rights; and YouTube put NFL commissioner Roger Goodell onstage to promote its first free NFL game (Chargers-Chiefs in São Paulo). Each publisher (especially those with legacy linear arms) has clearly bet the house on live sports and events, so much so that scripted programming has almost entirely evaporated from broadcast TV. Viewers’ time has fragmented across the streaming ecosystem with its deep libraries of content, leaving these live events as the last area of meaningful audience unification.

At the same time, these publishers are looking to differentiate themselves in their ability to bring effective advertising to those fragmented streaming audiences. Interactivity was another major element across upfront presentations this year. For NBC, this meant a focus on tools like engagement ads with “gamified” elements, YouTube launched shoppable CTV ads with an interactive product feed, while Amazon touted shoppable ads with real-time information from Prime. Surveys have shown shoppable formats are an area of growing interest for advertisers, so it was hardly a surprise to see this in the foreground. With advertisers particularly concerned with ad performance and lower-funnel impact, these new tools show the fight from TV publishers to keep ad dollars from shifting away, either to other marketing channels or other business uses entirely.

For all the pomp and circumstance, there was an air of uncertainty across many of the upfronts. The pressure each publisher felt, from its competitors and from the macroeconomy, was apparent. For advertisers, this does mean opportunity. Streaming CPMs continue to trend down amid the competition, meaning that advertisers with capital to deploy are able to make their investments work harder for them, even in premium inventory. Overall, we strongly encourage brands of all sizes to explore the linear, CTV, and broader video spaces while leveraging Bliss Point measurement to track impact throughout the funnel. | NBC, Disney, NBC

1. May was a packed month for Google events, from NewFronts and Brandcast to Google I/O, culminating in Google Marketing Live (GML). While AI and the evolution of Search dominated headlines – Michelle gives a great overview below – no Google event would be complete without a spotlight on YouTube.

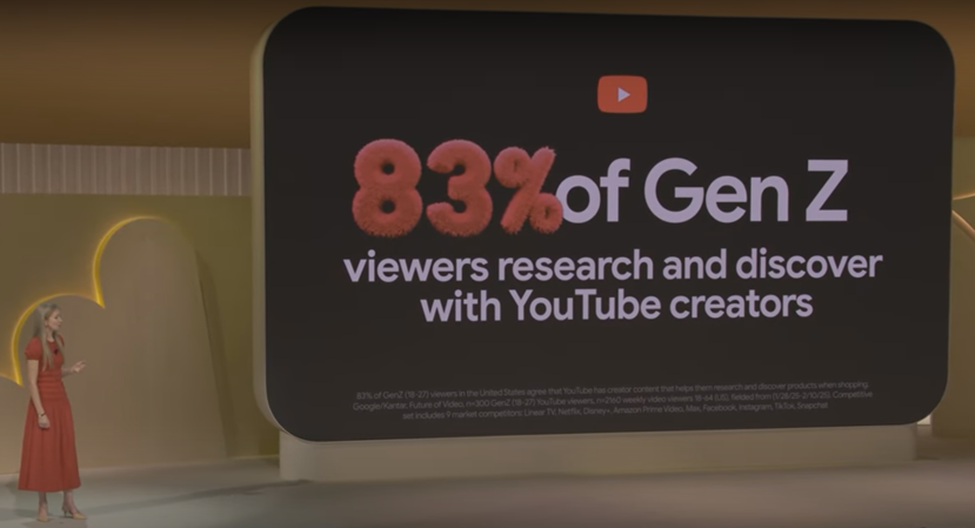

Google continued to emphasize YouTube’s value as a discovery engine, especially among Gen Z, with 83% using YouTube creators to discover and research new products. To help advertisers capitalize on this continued trend, Google announced two new tools:

We’re excited about both announcements, particularly the new attributed branded search reporting. YouTube plays a crucial role in the consumer journey, and Google reinforced this by restating that YouTube shortens the average online video shopper’s journey by six days. This always-on visibility into search impact will help advertisers better measure YouTube’s full impact and refine cross-channel strategies.

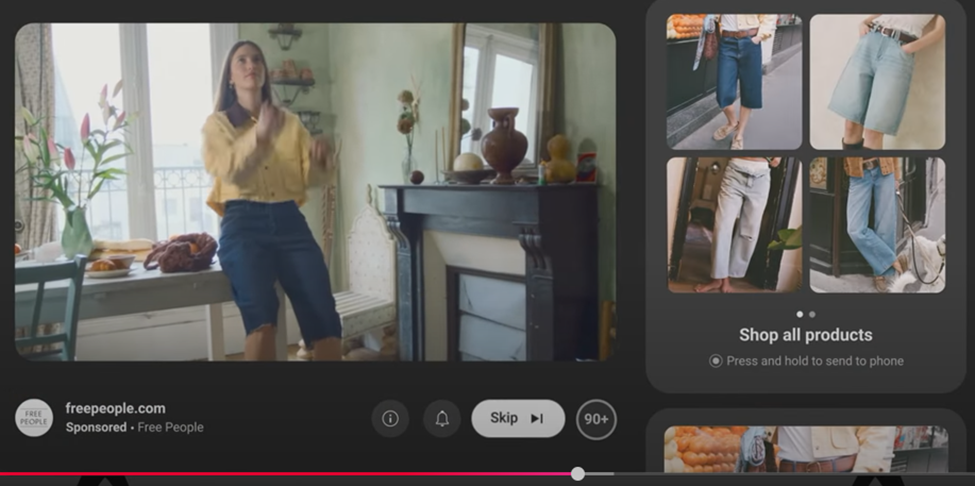

YouTube’s growing role as a shopping platform was also a major focus. Google shared that 68% of Demand Gen conversions came from users who never saw the brand’s ad on Google Search, showing how influential YouTube has become in driving purchase decisions. Additionally, brands using product feeds are seeing a 2x year-over-year increase in conversions per dollar spent.

To make the path from discovery to purchase even more seamless, Google is rolling out several new shopping features:

YouTube has long been an expansive discovery platform, and now it’s evolving into a full shopping experience, bridging the gap between interest and action. While features like the CTV-to-mobile conversion flow will take time to scale, they mark exciting progress—creating new opportunities for brands to drive engagement and for consumers to shop seamlessly from the content they watch. | Google, Search Engine Land

Last week Google stacked its two annual, announcement-packed events on back-to-back days: I/O and Google Marketing Live (“GML”). Unsurprisingly, the evolution of search as we know it was a key theme throughout both events. One thing that all speakers made very clear was that search is having a moment.

After the main keynotes and behind closed doors for select GML attendees, there was a fascinating discussion between top leaders from the organic / engineering side (Julie Farago) and the advertising side of Google search (Brendon Kraham). These two sides of the house rarely speak together in public (akin to “church and state”), so it was a big moment. Julie, who has been a leading engineer for 20+ years, shared that this current “AI in search” transformation has her more excited than she’s ever been (even more than other key moments like the transition to smart phones, the rise of voice search, and the launch of Chrome).

Throughout the I/O and GML events, there was a major focus on how user search behavior is shifting (becoming increasingly multimodal and unpredictable), and how AI is changing the types of queries and search results consumers can expect (more complex and nuanced). When asked, “What is one word you’d use to describe the future of search?”, Julie responded with “intelligent.” She discussed how search is moving beyond just understanding what people are looking for to understanding why, and how this shift means moving from matching keywords to predicting what people might need next.

After piloting it in Labs since early March, Google has now rolled out AI Mode to everyone searching in the US, and is experimenting with ads in AI Mode. At Tinuiti, we’re curious to see what usage of AI Mode in Google search will look like since AI Mode’s functionality is a bit buried within the search experience. Users need to specifically navigate to that separate tab in Google, so it’s not entirely intuitive for the everyday searcher. Digitally savvy folks will likely use AI Mode’s advanced capabilities more and more, but will everyone else even know it’s there?

We imagine ads in AI Mode will be rolled out very gradually and selectively, similar to what we’ve seen with ads in AI Overviews. However, a significant challenge for marketers is that there is currently no visibility or control over whether or how their ads are appearing in these Google AI search experiences. That lack of transparency has some brands concerned, especially when coupled with the ongoing challenges of accuracy from Google’s AI-generated responses. Many advertisers have been vocal about the need for Google to provide more transparency and control. Though we haven’t seen any momentum on that front yet, we’re bullish on Google eventually giving marketers more reporting and controls with ads in AI search, similar to how we’ve seen Google recently roll out channel level reporting for PMax campaigns after years of advertisers demanding that visibility. | The Keyword blog, Ads & Commerce blog, Ads & Commerce blog

The emergence of agentic commerce, featuring AI agents that perform tasks and make decisions for consumers, is swiftly transforming digital retail. This past week, Google demonstrated agentic shopping features on YouTube, signalling a direct challenge to TikTok Shops and opening new avenues for performance marketers.

Agentic AI’s disruptive potential in retail is already manifesting through personalized recommendations and streamlined customer service. A prime example is Amazon’s “Buy for Me” feature, which leverages an agent to enable seamless purchases from other brands directly within the Amazon Shopping app. While brands have often navigated a delicate balance regarding full product presence on platforms like Amazon, the increasing consumer demand for frictionless experiences is prompting a shift towards direct engagement within agent-driven commerce channels.

Beyond individual platforms, the broader ecosystem is adapting. Perplexity, an AI answer engine, has integrated with PayPal to power agentic commerce across its Perplexity Pro platform. This partnership allows users to complete purchases for products, travel, or tickets instantly with PayPal or Venmo directly within Perplexity’s chat interface. This integration signals a future where the act of purchase is woven directly into discovery and interaction points, rather than requiring users to navigate separate e-commerce sites. Google is also actively developing agentic capabilities for marketers, suggesting a wider industry shift towards AI-mediated interactions.For performance marketers, agentic commerce necessitates a re-evaluation of strategies. While traditional advertising remains crucial (for the moment), the focus must expand to optimizing for AI agent discovery and seamless integration into automated purchasing flows. Agentic commerce is moving rapidly, but the path towards an advertising supported model isn’t abundantly clear. It’s likely we will see a lot of activity in the next 12 months as platforms seek to monetize this frictionless shopping experience. | Google, Amazon, PayPal

1. BREAKING – On Wednesday, the US Court of International Trade – a relatively obscure federal court that adjudicates civil actions arising out of U.S. customs and international trade laws – ruled that the tariffs imposed under IEEPA are illegal and therefore void. The three-judge panel wrote, “The court does not read IEEPA to confer such unbounded authority and sets aside the challenged tariffs imposed thereunder.” The court issued a permanent injunction blocking the implementation of the tariffs.

The tariffs in question are the ‘Liberation Day’ tariffs and the fentanyl-related tariffs imposed on Canada, Mexico, and China. National security-related tariffs on things like steel and aluminum are unaffected by the ruling. Lawyers for the administration informed the court they will appeal; US and international equity market futures rose sharply on the news. | WSJ

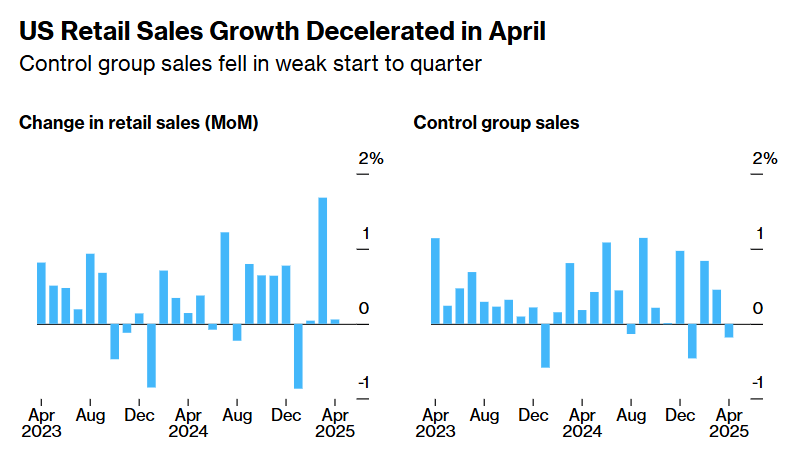

2. Following an epic surge of retail spending in March, as consumers pulled forward purchases in order to avoid large import taxes, U.S. retail sales decelerated dramatically in April, rising 0.06% MoM as compared to a 0.8% rise in April ‘24.

An economist at Pantheon Macroeconomics commented that, while retailers were helped by anticipatory purchases in March and available inventory buffers, “We see good reasons to think that spending will look a lot weaker in the numbers for May and June.”

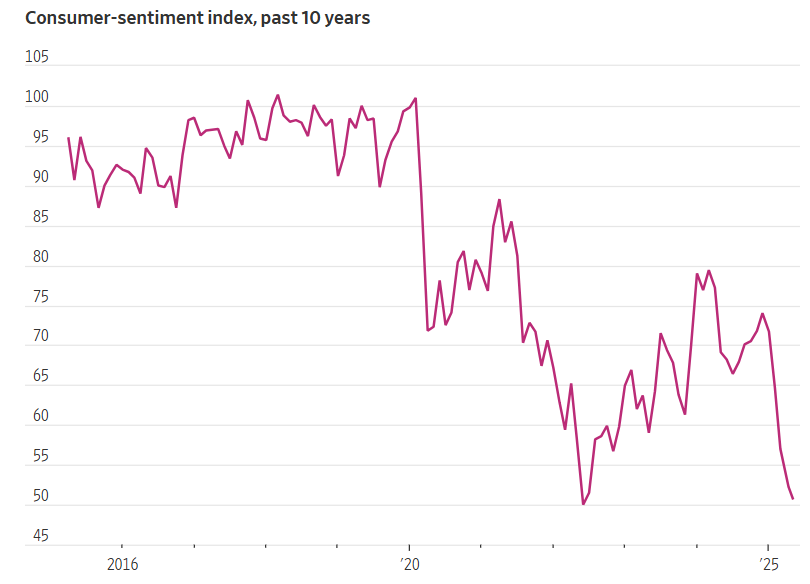

That point of view is consistent with the latest figures on consumer sentiment, which reached a three-year low in May and the second-lowest level on record. Tariffs were spontaneously mentioned by nearly three-quarters of consumers, up from almost 60% in April.

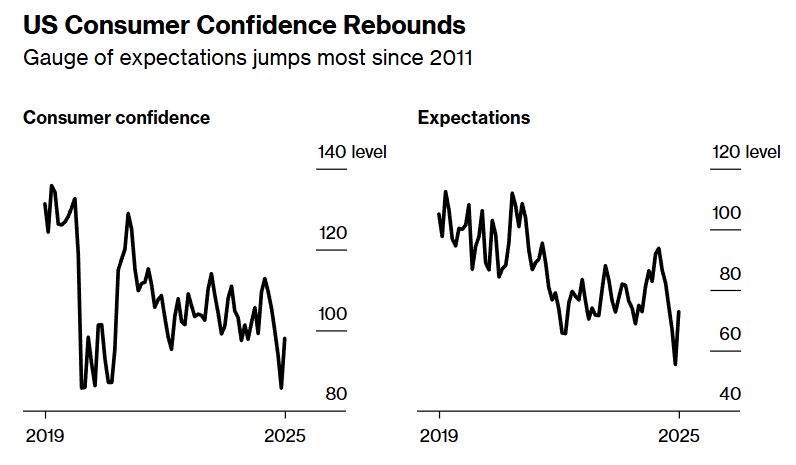

However, like the financial markets, consumers seem to be updating their views as policy continues to rapidly gyrate. The May figures for consumer confidence, which is closely related to consumer sentiment, showed a sharp rebound from April lows. Crucially, the sentiment survey ran from April 22nd – May 13th, while the confidence survey ran through May 19th. The US-China agreement to temporarily reduce tariffs was announced on May 12th.

The improvement in confidence was consistent across age and income groups as well as political affiliations, with the strongest gains among Republicans. | Bloomberg, WSJ, Bloomberg, Bloomberg

3. Meanwhile, the international trade machinations grind onward. One of America’s most prominent corporate citizens, Walmart, announced last week that it plans to raise prices this summer in response to taxes on goods it imports from abroad. Walmart’s CFO said, “The magnitude and speed at which these prices are coming to us is somewhat unprecedented in history.” The company would seem to have few options in the matter – Walmart’s 2024 profit margin was about 2.63%; if it were to allow its cost of goods sold to rise by ~30% (the level currently imposed on imports from China) while leaving prices unchanged, it would wipe out approximately its entire margin.

The company was, however, swiftly met with a public scolding from the White House, which is becoming a common occurrence for companies responding to changes in their cost structure. The White House press secretary said, “He [the President] maintains the position that foreign countries absorb these tariffs.” Shortly thereafter, the President himself posted, “Between Walmart and China they should, as is said, ‘EAT THE TARIFFS,’ and not charge valued customers ANYTHING. I’ll be watching, and so will your customers!!!” It’s increasingly clear that highly visible companies such as Amazon and Walmart will be forced to navigate between economic and political reality.

Meanwhile, the resumption in bilateral trade precipitated by temporary tariff reductions has kicked off a shipping boom:

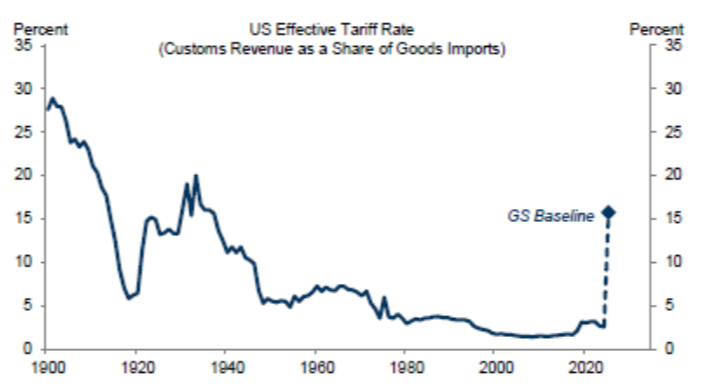

And let us hope this renewed momentum is self-sustaining, as a new Goldman Sachs research note painfully details the long-term harms of a high-tariff regime: lower growth and incomes; resource shifts from higher- to lower-productivity US firms; lower output and investment; less innovation; and increased rent seeking (manipulation of public policy as a strategy for increasing profits).

The GS researchers expect tariffs to remain elevated for the foreseeable future:

And highlight how tariffs will hit the most successful (i.e. most productive) American firms the hardest:

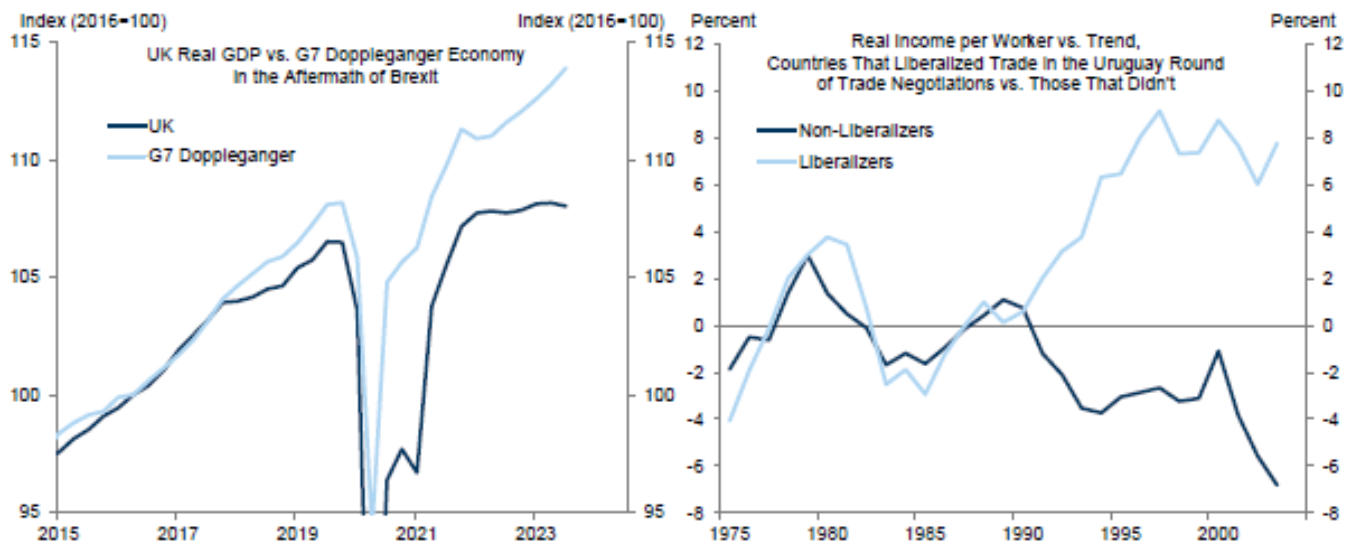

They illustrate, through both trade liberalization in the 1990s and UK Brexit, that trade barriers can have long-lasting effects:

For as long as trade policy is conducted by executive fiat, it remains extremely unpredictable. At the moment, prediction markets assign only a 3% chance to the removal of the 10% blanket tariff before July, and a 1 in 3 chance to tariffs on Chinese imports being below 25% by August 15th. | WSJ, Scott Lincicome