Media Update: Amazon Considers Ads for Prime Video, PGA Tour and LIV Golf Merge, Ad Market Decline in April

Industry Notes (Video)

1. Pure play SVOD is dead. That would seem to be a fair conclusion based on reports that Amazon is planning an ad tier for Prime Video, its premier streaming service.

The disruption of the linear video model and the shift to streaming posed some existential questions for the advertising industry – Netflix pioneered the category and was militantly anti-ads for years, and nearly all the premium streamers in its wake copied the model: HBO (Go/Now/Max), Disney+, and Apple TV+ all shunned ads at launch. But the math didn’t work – the programming costs required to persuade consumers to sign up and then not churn (since they’re much less locked in than under the cable bundle) are extremely high, and the lack of a distribution bottleneck (like a cable operator) made the favorable economics of bundling much harder to achieve. Shunning an advertising revenue stream, and running a cash incinerator in the meantime, was not sustainable. The past 18 months have seen a dramatic aboutface, with first Disney, then Netflix, and now Amazon bringing ad-supported options to their flagship streaming platforms (and Apple TV+ is likely to follow suit before long.)

From Amazon’s perspective, it would step into the streaming ad game with a formidable set of advantages:

And finally, advertising is just a great business if one can reach critical scale. While Amazon’s core ecommerce business was flat YoY in Q1, its advertising business grew by 21%, and its margin profile indicates it may be generating as much free cash flow as AWS. Presuming Amazon does indeed move ahead with an ad tier for Prime Video, we expect to see a similar pattern to other high-profile ad introductions: very high CPMs and limited inventory at launch, with supply increasing and CPMs dropping after a few months in market. | WSJ

2. Comcast has launched Now TV, a cable-lite streaming package for price-sensitive users. Priced at $20, Now TV offers a cost-effective option that includes Peacock Premium and FAST channels. However, it’s important to note that Now TV does not include some popular cable channels like CNN, ESPN, and TBS and thus lacks the same value of a traditional cable bundle.

In an effort to adapt to changing consumer preferences, Comcast might also be exploring a shift away from set-top boxes that come with Xfinity stream. These boxes have long been a staple of Comcast’s business model, often costing customers an additional $6+ per month. By exploring alternatives such as smart TVs to deliver content and supplementing information, Comcast may be looking to cater to customers who are increasingly seeking flexible and customizable options. This is all representative of Comcast’s attempt to capture the attention of cord-cutters and address concerns over the high pricing of cable bundles. However it’s not evident that there is a large market for cable-lite offerings. Virtual multichannel video programming distributors like YouTube TV, Sling, Hulu Live TV, and Fubo all launched around $20-$40, but as they improved their offerings, they also hiked their prices. The business imperative now lies in discerning whether this strategy will yield consumer acceptance, thereby cementing it as a viable model in this complex market. | The Verge

3. Netflix’s efforts to crack down on password sharing, as seen in the successful test conducted in Canada, are now being implemented in the United States. With an estimated 100 million non-paying users worldwide, Netflix is aiming to convert a large portion of non-paying subscribers to its ad-supported tier. Password sharers, who are typically more price-sensitive, will play a significant role in shaping the demand and pricing in the ad market. From Netflix’s perspective, ad-supported tier users already have a higher APRU than users of Basic and Standard (ad-free) tiers above it. Therefore, the company is highly motivated to grow this user base and improve on its ad tech.

The focus on supply and ad market growth highlights the evolving dynamics of the streaming industry. Other streaming services may observe Netflix’s approach to address password sharing and adopt similar models. The success of this strategy for Netflix will depend on finding the right balance between monetization and user satisfaction. As the industry continues to evolve, it will be interesting to see how ad supply and pricing are influenced by these developments and whether other platforms will follow suit in their efforts to tackle password sharing and tap into the potential of ad-supported tiers. | The Verge

4. Streaming might claim the broadcast rights of another sport, with Apple, Fox, and Netflix emerging as potential contenders in the race for NBA’s future broadcasting rights. Their interest underscores a larger industry trend as companies strive to harness the enormous popularity of sports like the NBA to entice and retain viewers.

In the broader context, these developments reflect similar discussions taking place in numerous sports networks, such as ESPN, considering a DTC approach. However, the viability of such a delivery model isn’t yet definitively established, as the substantial cost associated with sports rights can present significant financial challenges. Sports rights often command billion-dollar price tags, and whether these investments can offer adequate returns, despite the large potential audiences, remains a matter of speculation. The future trajectory of sports media will likely be heavily influenced by these unfolding events. | Bloomberg

Viewership across all genres fell towards the end of May, with sports declining the most before rebounding in the first week of June.

Industry Notes

1. In a rather seismic shift, the PGA and LIV Golf will be merging together, putting aside a feud that gripped the golf world for the past two years. As you may recall, LIV Golf began broadcasting on the CW this year and brought in a relatively small audience. After the first six events, the league stopped reporting ratings, leading many to speculate that it was not generating sufficient audience interest, despite its placement on a national network. The merger of these leagues came as a surprise not only to the players and fans, but also to the PGA Tour’s media partners, raising questions over whether the new entity will attempt to renegotiate its media rights deals. In the near-term, it seems that the PGA Tour and LIV Golf will remain separate brands with their broadcasting rights intact, but as this merger was announced without many details, we will have to wait and see how this shakes out.

From a viewership perspective, it is evident that the PGA outperforms LIV. More than that, it appears that PGA viewership overall has increased modestly from last year. In April the PGA reported that total audience delivery was up 3% on NBC, 4% on CBS, and 9% on the Golf Channel. It is true that viewership of the PGA Championship fell to a 15-year low for the final round, but the Masters also scored a 5-year high in final round viewership. With the LIV not damaging viewership, it seems that the reason for the merger has more to do with the costs of prolonged legal battles. While we wait for more details on the merger and its impact on broadcasts, it seems likely that the integration of these two leagues could have a positive effect on golf viewership, eliminating head-to-head scheduling and increasing the number of golf events throughout the year. | ESPN, SMW

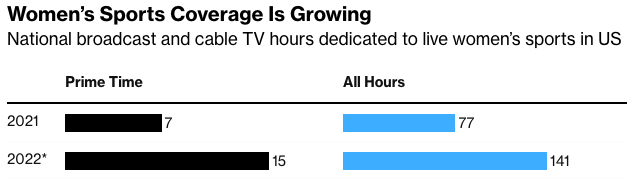

2. We’ve frequently covered the growth of women’s sports viewership in the United States, with increases across the board indicating a solid appetite for the genre.

In large part, media companies have benefited from the growth of these sports, as advertising revenue has increased commensurately with viewership growth. With NCAAW rights expiring next year and WNBA expiring the year after that, ESPN will have to fork over a lot more to retain rights. In 2011 ESPN paid just $24 million for 20 NCAAW sports – rights for the NCAAW college basketball final are now expected to fetch $100 million alone. This is a serious problem for ESPN, as the decline of traditional television has put financial pressure on all Disney networks. As the media company looks to retain the rights for the sports that it largely helped grow, we might see some properties go to other networks or streamers. | Bloomberg

1. The U.S. ad market declined for the 10th consecutive month in April – but it’s not as bad as the headline implies. April YoY fall is the smallest since September 2022, and the first few months of this year were particularly affected by tough comps. This small decline might actually signify that erosion in demand might be bottoming out as the macroeconomic picture is a bit rosier than it was at the end of last year/beginning of this year. Throughout this uncertainty, digital media has fared better than other channels and increased its share of ad spend by 4 points YoY. | Media Post

2. According to a recent study by MediaRadar, ad spending on streaming was down 28% YoY in the first quarter. As we near the end of the second quarter, concerns regarding the ongoing writers’ strike are bubbling, even if streaming services are more insulated because of their large libraries of content. Several original shows on Netflix and Max have delayed production schedules, which could affect delivery at the end of 2023 and into 2024. The decline of original content on traditional television will likely result in increased ad pricing on streaming content. | Media Post

1. Although the concern of a recession has been top of mind for the better part of the last year, consumers are showing surprising resilience.

Of course, this also means that inflation falling below the Fed’s target of 3.5% seems increasingly unlikely in the near-term – and in turn, the Fed might not cut interest rates for a while. Core inflation, excluding food and energy, ticked up in April to 4.7%. Despite sustained inflation, consumers are still finding the budget to keep their heads above water. | WSJ

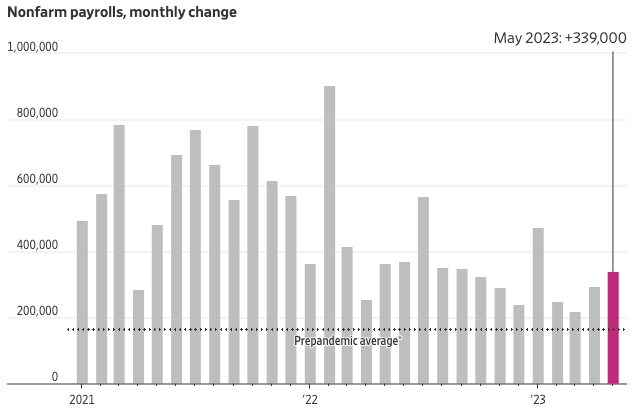

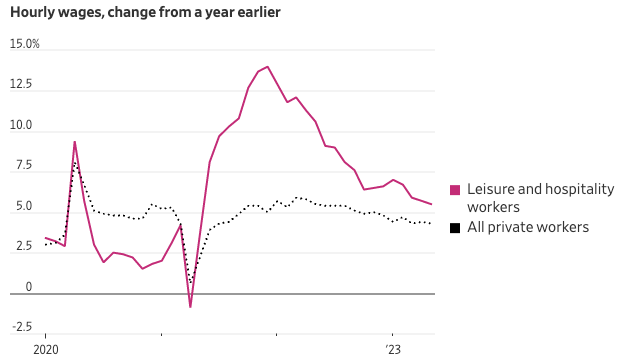

2. Like last year, the strength of the labor market is a major contributor to the health of consumers. In April there were 10.1 million job openings, an increase over March and just under double the 5.7 million people looking for work. The evidence of strong labor demand was bolstered by the May jobs report, which revealed that employers added 339,000 jobs in May:

That being said, there was some data that reinforced the idea that the labor market is slowly cooling: the average workweek fell to 34.3 hours, slowing wage gains on a weekly basis. Hourly wage gains have also moderated in 2023:

Although economists are still expecting a recession some time in the next 12 months, the strength of the labor market indicates that the economy still has a lot of steam in it. | WSJ, WSJ