Media Update: Viewership Down For Popular Streaming Titles, 2022 Cord Cutting Tally, and Official January Labor Market Numbers

The overall supply of ad-supported streaming video remains unchanged relative to recent levels.

Industry Notes (Video)

1. Creating hit content is an expensive endeavor, one that streamers have happily engaged in for the past few years. However, especially in the last two quarters, media companies have been warning that content spend cannot continue to increase if their streaming platforms are to achieve profitability. Indeed, the slowdown should be significant: Ampere Analysis estimates that original content spending by streaming companies will grow 8% in 2023 – a healthy clip, but nowhere near the 25% growth that 2022 saw.

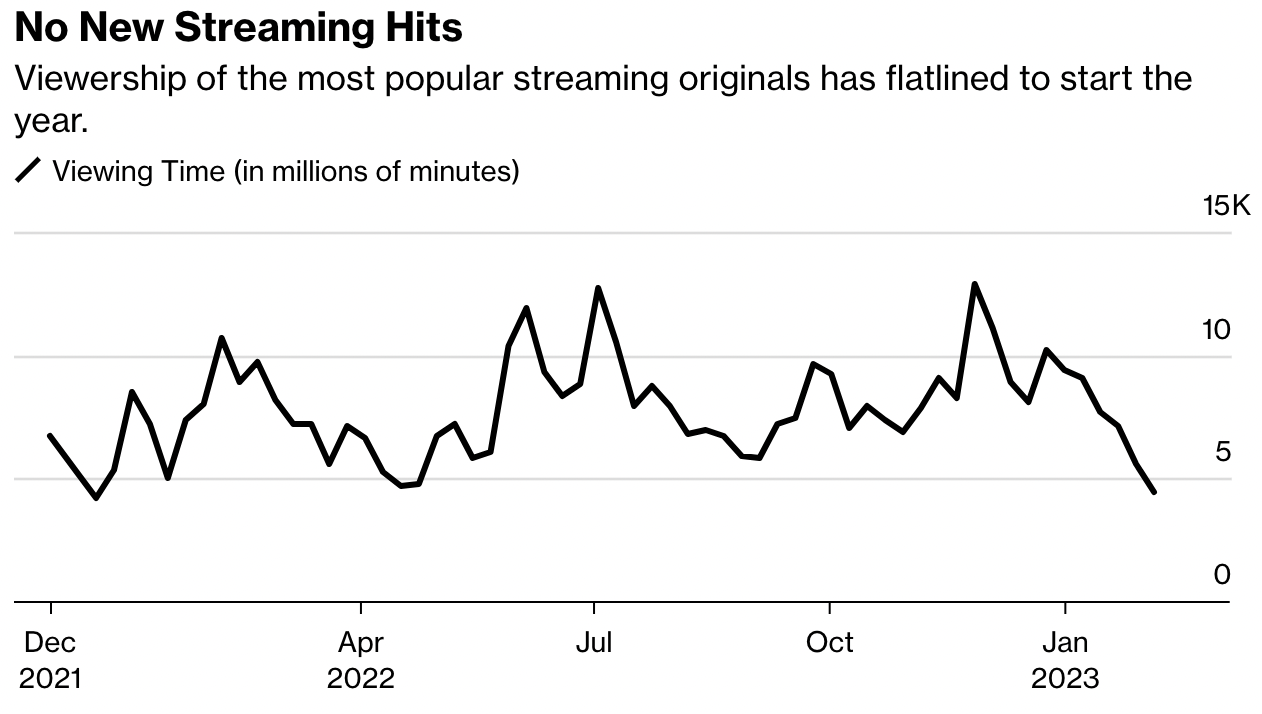

People are streaming at record rates – viewership in January was up 31.8% over last year, and streaming grew its share of TV usage by over nine points last year. However, in the first few months of the year it is clear that viewership of streaming originals in off to a slow start:

The decline amounts to a ~8% drop in viewership for streaming originals over last year. Notably, Disney+ and Hulu have not released a hit show in the United States, and Netflix has but one (Ginny and Georgia). The Last of Us, one of the most popular shows right now, does not count as streaming because it debuted on HBO. While performance in the beginning of the year might not be indicative of the future (there are several popular shows slated), the decline highlights the difficult bind many platforms are in – hit content is the lifeblood of growth and engagement, but it’s extremely expensive and the economics don’t yet work for the industry as a whole. | Bloomberg

2. ESPN is reportedly exploring the creation of a central hub that would link out to the streaming service (whether ESPN or not) where a live sports event is available. Already on the ESPN website and app, users can see the network that an event is broadcast on, right alongside ESPN’s live coverage. The sports network is holding conversations with leagues and media partners, seemingly unconcerned that this feature could benefit its competitors. Then again, becoming an aggregator in the streaming space is a highly coveted market position. There has been notable movement on this front recently: HBO Max returned to Amazon Channels (because it lost over 5 million subs by leaving) and YouTube launched an aggregator called Primetime Channels. From the side of publishers like HBO Max, the opportunity cost of allowing transactions through only a single channel (their website) is too great to ignore, especially as the market has become more saturated and net-new subscribers harder to attract. Aggregators typically take a 30% cut of subscription revenue, and ESPN is undoubtedly looking to adopt a similar fee structure for its feature.

Sports in particular are ripe for centralization; broadcast rights have been increasingly sliced and diced to appease the appetite of streaming services and fans are clamoring for some form of centralization. For one example, consider the headache that Yankees fans experience. Games are spread across YES Network, ESPN, TBS, Prime Video, Apple TV+, and Peacock. In some cases, the broadcast depends on the day of the week, and if you do not have a smart TV, it means switching devices and accounts! With the future of RSNs in question, this situation will likely get worse before it gets better. In reality, because of the fractured nature of this space, ESPN might not be able to create a “YouTube Channels for sports” in the immediate future – but simply linking to other services, and collecting their due, can be immediately implemented and is an important first step in becoming the single-point-of-entry for sports fans. ESPN’s desire to become an aggregator is a microcosm of broader strategic change in the streaming wars and we can expect to see more of the collaboration that benefits consumers as streaming companies focus on growing revenue. | CNBC

3. Newly installed YouTube honcho Neal Mohan said last week that YouTube will incorporate new generative AI features into its video-sharing platform, with an initial focus on tools for creators. Per Mohan, “The power of AI is just beginning to emerge in ways that will reinvent video and make the seemingly impossible possible.”

While it is Mr Mohan’s job to focus on creators, it is our job to focus on advertisers. And it is a sure bet that advertising will be one of the earlier use cases for generative video. As major digital platforms have become increasingly sophisticated over the past decade in terms of targeting and budget optimization, brands have been left with creative production as their owned link in the value chain. Because this can be a costly and time-consuming link, it’s a juicy target for AI, and powerful new tools are on the way:

Text-to-video generative models are in their infancy, to be sure. Today, most produce somewhat grainy, clunky videos of a few seconds. But the prototype that gave us the swimming teddy bear above “can generate arbitrar[il]y long videos conditioned on a sequence of prompts.” While creators will surely come up with hugely inventive ways to use these tools, we’re excited to see, and to help bring to market, the application of this technology in an advertising context. | Bloomberg, Phenaki

Industry Notes (Audio)

1. According to Edison’s quarterly Share of Ear report, Spotify Ad-Supported narrowly surpassed Pandora Ad-Supported in share of daily audio listening for the first time. Spotify has been steadily increasing its share over the past few years, and grew its ad-supported MAUs by 25% in 2022.

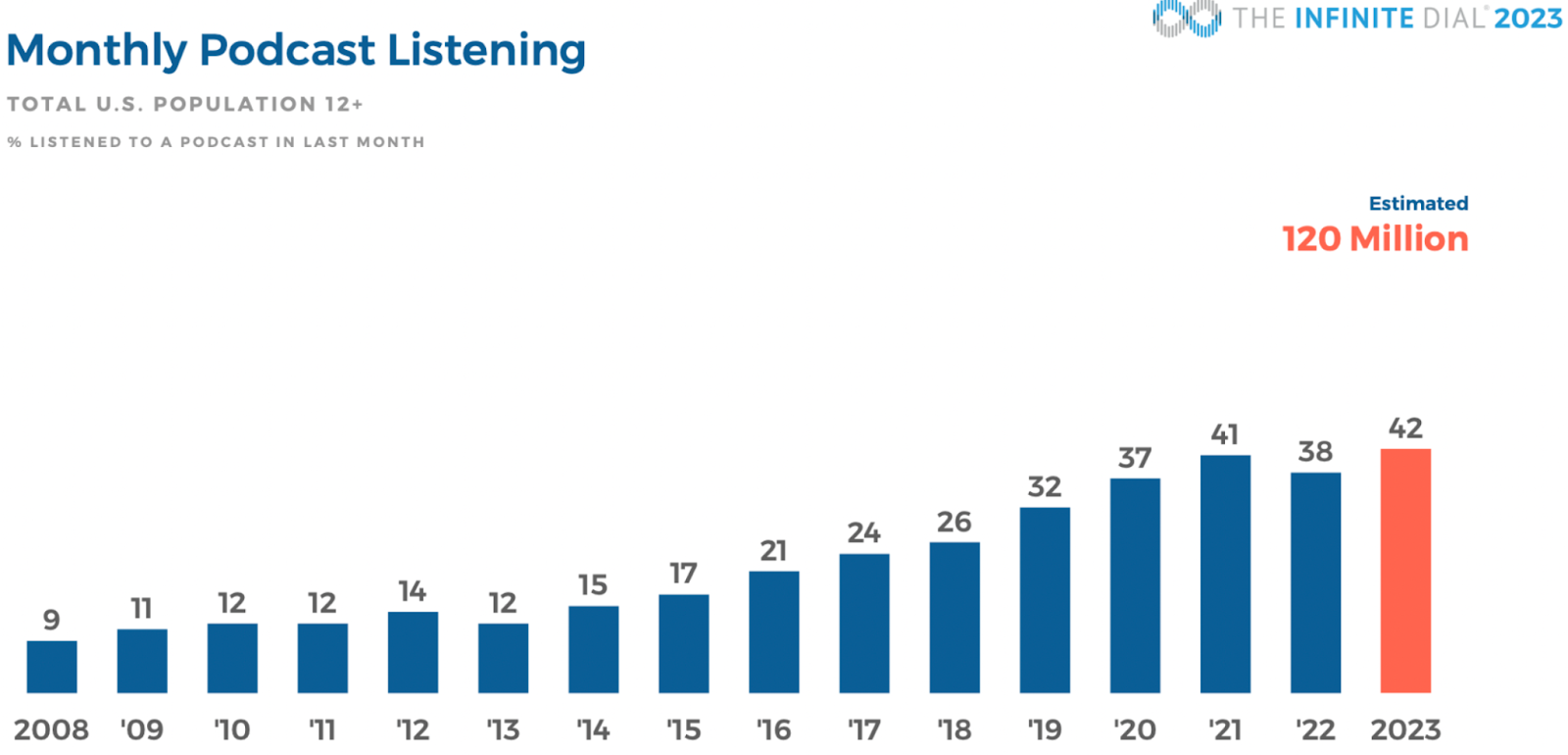

Overall, daily listening time rose 5% over last year, driven by the rising popularity of talk-based content. If you will recall, podcasting has been experiencing a bit of a crisis behind the scenes – major audio companies have pulled back investment in new shows and deal making has slowed. However, after a brief dip in 2022, monthly podcast listening is again growing, with 42% of Americans listening to podcasts in the last month. On the advertising front, there does not appear to be a slowdown in ad spending on podcasts, unlike the rest of the advertising. | Edison Research

News viewership remains way down on a YoY basis, owing to the shock of the invasion of Ukraine at this time last year. Sports viewership is up slightly, while Spanish language and general entertainment remain way down YoY.

Industry Notes

1. The final count is in: pay TV providers lost 5.9 million subscribers in 2022, an increase over the 4.69 million lost in 2021. This brings the total down 70.2 million, as 8% of the base was erased. As noted numerous times last year (nearly every quarterly earnings report from pay TV providers came with a shocking loss), the concerning loss of subscribers is only accelerating and the growth of vMVPDs is not offsetting it.

| Pay-TV Providers | Subscribers at end of 2022 | Net Adds in 2022 |

|---|---|---|

| Comcast | 16,142,000 | (2,034,000) |

| Charter | 15,147,000 | (686,000) |

| DIRECTV^ | 13,100,000 | (1,500,000) |

| DISH TV (DBS) | 7,416,000 | (805,000) |

| Cox | 3,050,000 | (340,000) |

| Internet-Delivered (vMVPD) | ||

| Hulu + Live TV | 4,500,000 | 200,000 |

| Sling TV | 2,334,000 | (152,000) |

| fuboTV | 1,445,000 | 323,000 |

Numbers for vMVPDs were less than spectacular. After gaining 885,000 subscribers in 2021, these services added just 370,000 last year. YouTube TV is notably excluded from this analysis because it does not report subscriber counts; back in June the service declared that it had surpassed 5 million subscribers, but did not indicate if that figure encompassed solely residential subscribers. As you will note, that could put the vMVPD at the top of the list, and with its recent acquisition of NFL Sunday Ticket, it is a major player in the space. Looking to 2023, it is likely that losses in the cable industry will mount, and vMVPDs will continue their modest ascent. | Media Post

2. The TV upfronts are around the corner and it seems that flexibility is set to be of the utmost priority to buyers and media companies. Last year’s upfronts were record breaking – companies like NBCUniversal and Disney scored massive gains, significantly boosted by spending on CTV; Peacock doubled its upfront commitments to $1 billion, and 40% of Disney’s commitments came in streaming and digital. But as the advertising market declined, there was record “breakage”, i.e. fall-off from planned media commitments to actual booked media commitments. Heading into this year’s upfront negotiations, it seems that the same issues that plagued the industry at the end of last year – worsening macroeconomic conditions and broad uncertainty – will heavily factor into negotiations. Because the macroeconomic picture has not obviously improved in the past few months, we could see uncertainty manifest as demand for greater flexibility in linear contracts, and greater commitments to CTV, which is traditionally much more flexible.

To be clear, projections of spend at the upfronts are highly speculative right now. The ad market is down (-5.8% in January, YoY), but the CEOs of Paramount, Warner Bros. Discovery, and NBCUniversal all indicated cautious optimism for the second half of the year after softness in the first half. Additionally, some of the largest advertisers – those most likely to participate in the Upfronts – are still planning to increase their advertising spend in 2023. Coca-Cola, Kraft Heinz, Unilever, and Procter & Gamble can all be counted in that group. We will have to wait to see how exactly spending will shake out, but it is certainly something to watch as the upfronts – and breakage – have a major impact on pricing and availability in the scatter market. | Adweek

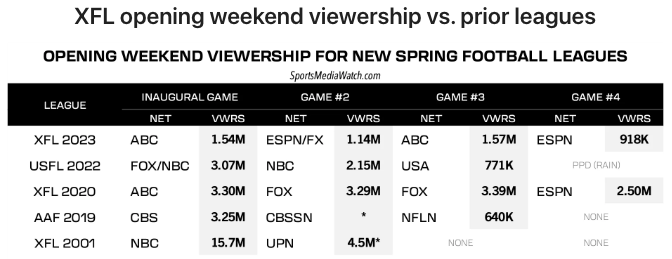

3. The XFL is back, but it’s certainly not better. Viewership for opening weekend (2/18-2/19) declined approximately 50% compared with its last iteration in 2020, and was lower than similar NFL-alternative leagues. Viewership in the second weekend fared no better, falling more than 50% from Week 1. Week 2 was the first week without a single game airing on broadcasting television, resulting in an average of 655,000 viewers across ESPN, ESPN2 and FX.

The challenge of attracting and retaining viewers is nothing new for NFL-alternative leagues. Theoretically, there should be a large appetite for football – the NFL is the undisputed king of television and the audience is massive. But despite decent viewership in Week 1, every league experiences a major dropoff the following week; USFL 2022 dropped 57%, XFL 2020 dropped 34%, and AAF 2019 dropped 69%. Leagues continue to iterate in an attempt to capture some of the NFL’s audience, but so far the resounding response from fans is “we’re not interested.” That being said, this year will be a fascinating test, as the XFL and USFL will coexist for the first time. It is hard to imagine that there is sufficient interest to support two leagues, but the success of even one would still be a significant change in the industry.

Update: Viewership fell 13% in Week 3 from Week 2, with an average of 571,000 across FX and ESPN2. Three of the four games were broadcasted on FX, which has not regularly carried live sports since the 2000’s. Because of weak viewership, ESPN will be moving two games originally scheduled for FX to ESPN and ESPN2, and one from ESPN to ABC. | SMW, SMW

In the Tinuiti Q4 Digital Ads Benchmark Report we noted that ad spending growth was decelerating across channels – Facebook in particular experienced a decline of 7% YoY growth in the fourth quarter. As a result of signal loss owing to Apple’s ATT, agencies and brands appear to be losing confidence in Facebook, even as they are still spending on the platform.

This data comes from a survey that Digiday conducts among agencies and brands. While there is not a correlation between confidence and spending in Digiday’s survey, the decline in confidence is certainly not favorable for Facebook. Then again, Facebook guided that Q1 revenue would be near $28.5 billion, which would mark a return to revenue growth following three consecutive quarters of decline. As Facebook’s performance is an important bellwether for the industry, this is certainly an area to watch. | Digiday

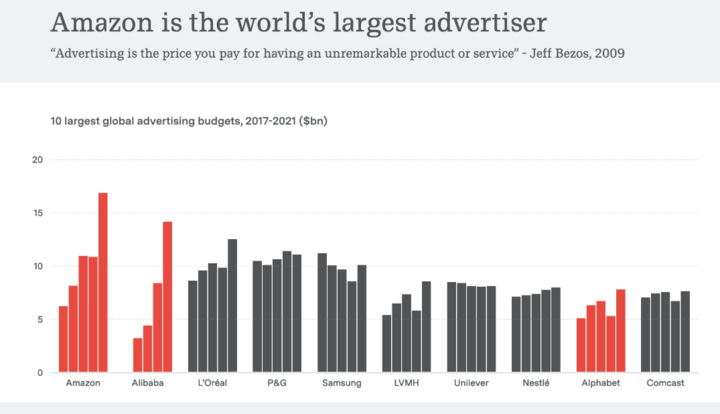

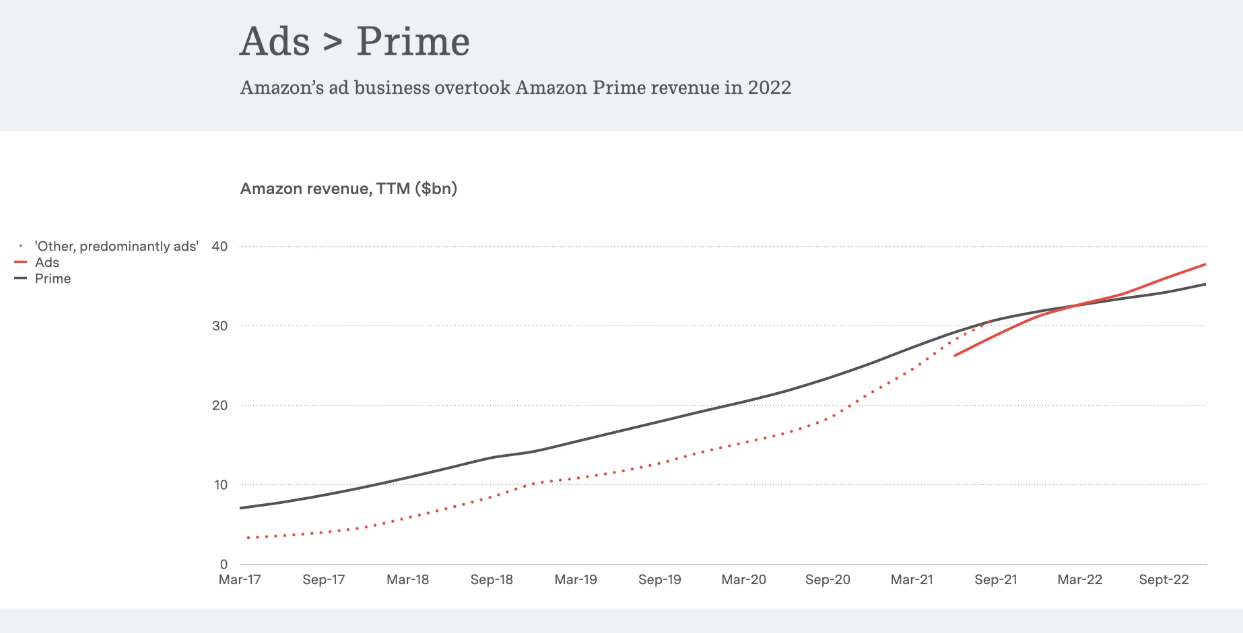

There is a saying that every platform that attracts a sufficiently large audience eventually tends toward advertising. We’ll propose to call this Bezos’ Law for just how spectacularly Amazon illustrates the adage. Consider:

Fast forward fourteen years, and Amazon has become the world’s largest advertiser:

And not only is Amazon spending lavishly on advertising, it’s also raking it in from its own advertising business – Ads now contributes more revenue than Prime!

Other prominent examples of Bezos’ Law include Google, Netflix, Uber, Instacart, and on and on. It seems that a prominent business model for the 21st century will be “an advertising business with [consumer feature] attached.” | Benedict Evans

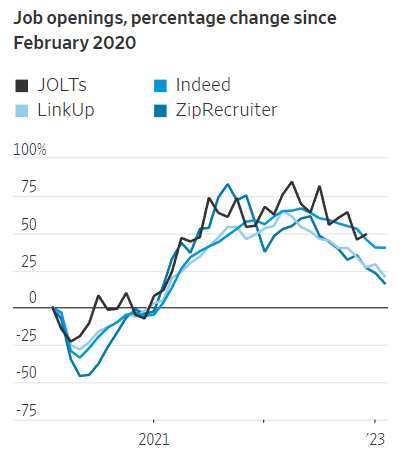

1. Last week we told you about scattered indications of a cooling labor market, pointing to data from job listing platforms like ZipRecruiter and Indeed:

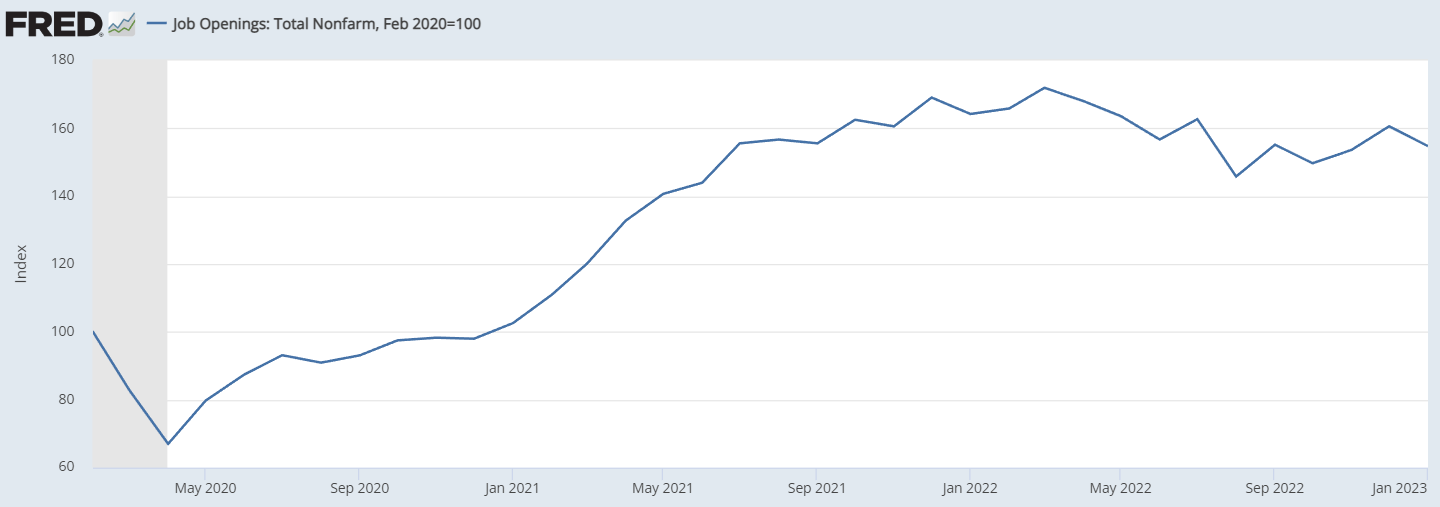

New official data have now been released that show job openings fell and layoffs rose in January, reinforcing the notion of the labor market cooling off. Here are the update job openings figures:

As you can see above, the dropoff in job openings is not dramatic, and the level remains about 50% above where it was in February 2020.

Layoffs increased to a seasonally adjusted 1.7m in January, and 20% increase YoY and up from 1.5m in December. Once again, this is a directional cooling of the labor market, but the level remains below its pre-pandemic baseline.

Overall, the labor market continues to show remarkable resilience, with unemployment at record lows, but signs of the Fed’s “medicine” taking effect are beginning to accumulate. February job figures will be released this Friday, followed by consumer inflation numbers on Tuesday. | WSJ

2. More and more retailers are expecting sales to fall this year, as persistent inflation weighs on shoppers. Both Macy’s and Best Buy are projecting worse performance for 2023, joining other major retailers like Target and Home Depot in expressing concerns over the sustainability of consumer spending. In a seemingly contradictory development, retail spending rose 3% in January – for reasons that are not easily discernible – with spending shifting away from non-essential goods. Notably, Target, Walmart, Kroger, and Costco all reported that consumers are increasingly deal-hunting and that groceries/essentials is the primary category of growth. As Kroger’s CEO put it, “[consumers] are behaving as if they are already in a recession.” So where does that leave retailers that do not deal in essential goods? Mostly unsure. Some, such as Big Lots, are not even providing annual guidance because the uncertainty in the macroeconomic environment is too great. Based on the general consensus of the industry, it seems that sales will be at most flat this year. | WSJ

As retailers expect sales to fall, consumers’ optimism about their current financial situation has reached a 13-year low. Squeezed by rising prices and dwindling savings, consumers are more pessimistic about their financial future than before in recent memory. The Fannie Mae survey that gathered this data also indicated that nearly 24% of respondents were concerned about losing their job in the next year. However, Friday’s jobs report is expected to postpone that fear a bit, as ADP is reporting that private companies beat expectations by adding 242,000 jobs in February. If job numbers stay robust we can anticipate the Fed implementing further rate hikes to try to slow the rate of inflation. | Bloomberg