Digital Ads Benchmark Report Q1 2024

Quarterly Trends Across Google, Meta, Amazon, And More

Quarterly Trends Across Google, Meta, Amazon, And More

The Tinuiti Digital Ads Benchmark Report is based on anonymized performance data from advertising programs under Tinuiti management, with annual digital ad spend under management totaling over $4 billion. Samples are restricted to those programs that have remained active and maintained a consistent strategy over the time periods studied. Unless otherwise noted, all figures are based on same-client growth. The trends and figures included are not meant to represent the official performance of any advertising platform or the experiences of every advertiser.

Note: The data below is from 2024. Head here to see our most recent report.

Tinuiti is the largest independent performance marketing firm across Streaming TV and the Triopoly of Google, Facebook, and Amazon, with $4 billion in digital media under management and over 1,000 employees.

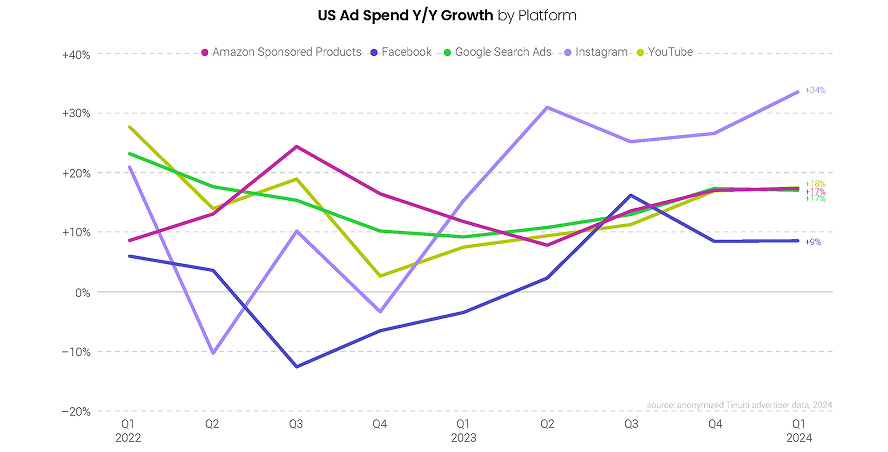

Across the major US digital ad platforms of Amazon Sponsored Products, Facebook, Google search, Instagram, and YouTube, year-over-year spending growth largely held steady from Q4 2023 to Q1 2024. The exception was Instagram, which not only grew advertiser investment the fastest of these platforms for the fifth straight quarter, but saw a seven-point acceleration in advertiser spending growth to 34% Y/Y.

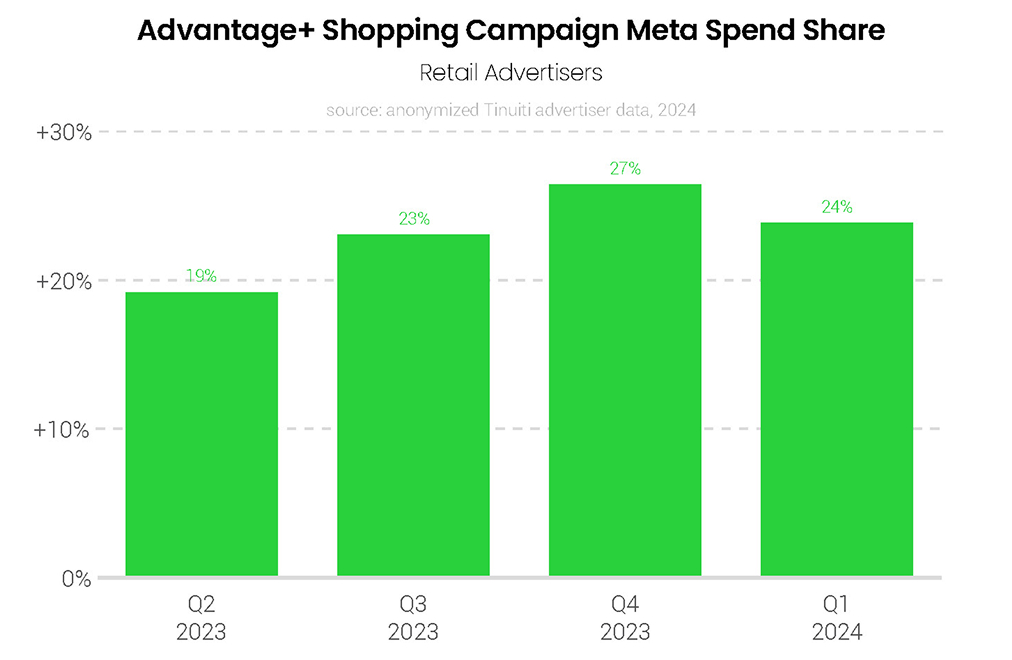

With Facebook seeing a 9% increase in spending in Q1, Meta Ads saw a 16% overall increase in spending including Instagram, up from 13% a quarter earlier. Advantage+ shopping campaigns have proved to be a key driver of Meta’s recent turnaround in growth. In Q1, 24% of retailers’ Meta spending was attributed to these AI-powered campaigns, up from 19% in the first half of 2023.

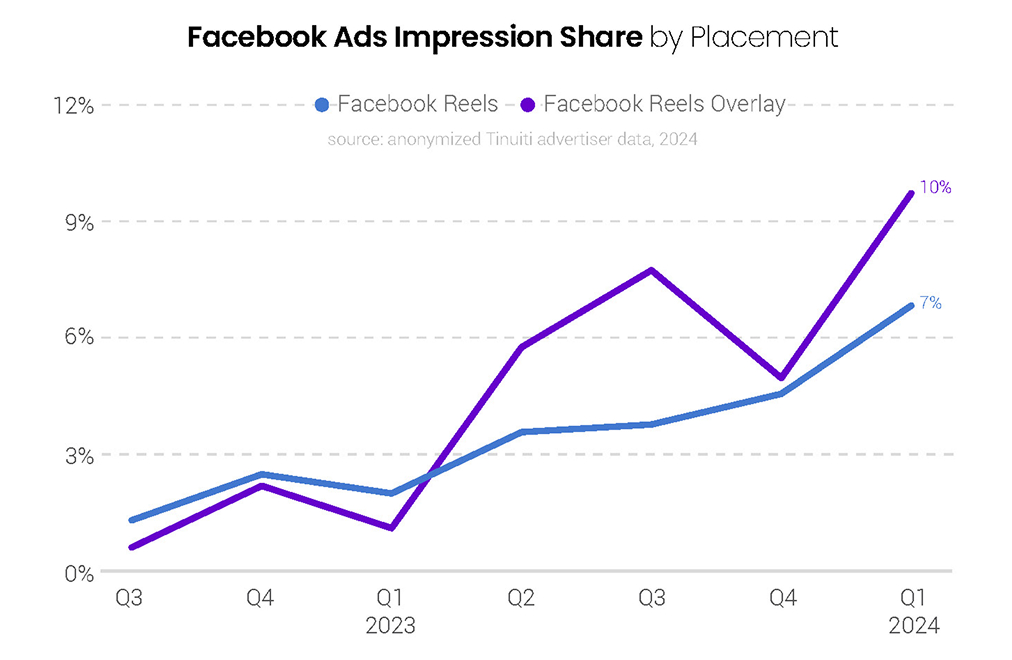

Instagram and Facebook also continue to improve the contribution of Reels to advertiser investment in each platform. Between Reels video ads and Reels overlay ads, Reels ad units accounted for 17% of Facebook impressions in Q1 2024, up from just 3% a year earlier. For Instagram, Reels ads produced 13% of impressions in Q1.

While there are many moving pieces in the Google search ad world, including the rise of Performance Max campaigns and the entry of Temu as a major competitor for impressions, spending growth ultimately held steady at 17% Y/Y from Q4 to Q1. News on the competitive landscape proved mixed for retailers in Q1 as Amazon appeared to take a more aggressive stance in Google shopping ad auctions throughout the quarter while Temu’s presence faltered in just the last few weeks.

Although YouTube inventory is now available through Google’s Demand Gen and Performance Max campaigns, advertiser spending on standard YouTube video ad campaigns remained strong in Q1, growing 18% Y/Y, up a point from a quarter earlier. TV screens accounted for 30% of YouTube investment, with spending up 36% Y/Y.

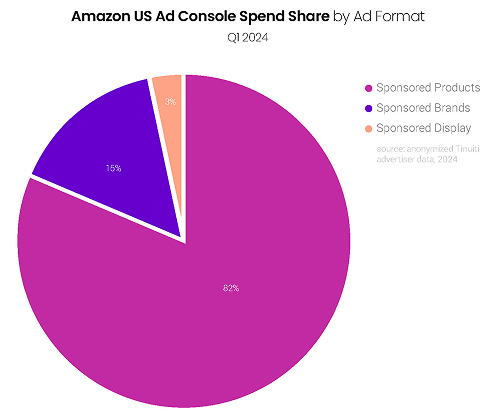

Spending growth for Amazon Sponsored Products trended closely with Google search and YouTube over the last two quarters, with growth little changed at 17% Y/Y in Q1. Advertisers saw mixed results for Amazon’s two other Ad Console formats in Sponsored Brands and Sponsored Display, but Sponsored Products accounted for 82% of Ad Console spend in Q1. For its part, the Amazon DSP generated an 18% increase in spend in Q1, the first quarter in which brands ran Prime Video ads through the platform.

Although its scale is not nearly as large, Walmart Sponsored Products has been the one digital ad platform in this report to outpace Instagram in spending growth in each of the last five quarters. In Q1, Walmart Sponsored Products spending was up 35% Y/Y. As another rising platform, TikTok has seen spikier growth rates than Walmart, with spending up 64% in Q4 2023, but just 21% in Q1 2024.

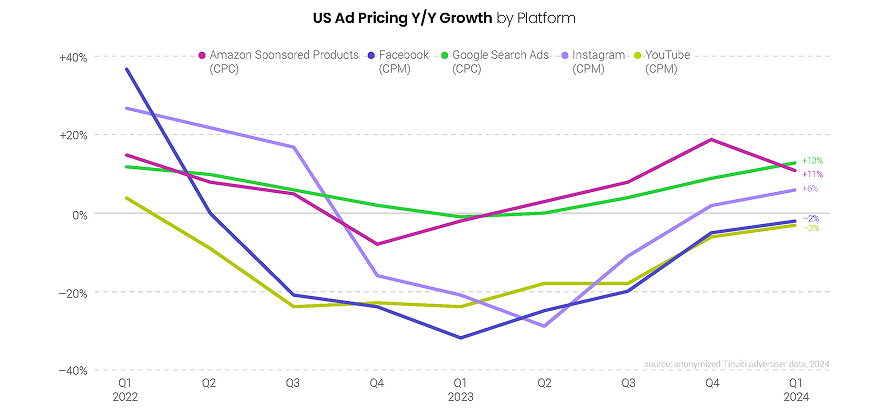

Across the five major platforms covered in this report only Amazon Sponsored Products saw slower pricing growth in Q1 than in Q4, but all have seen a significant increase in pricing growth since Q1 2023. On average, Y/Y pricing growth ran 21 points higher in Q1 2024 than it did in Q1 2023, a quarter where all five platforms saw Y/Y declines, with three seeing declines greater than 20%.

Typically managed with a focus on cost per click (CPC), Google search and Amazon Sponsored Products ads are also generally lower funnel and did not see pricing decline as sharply in late 2022 and early 2023 as it did for CPM-focused platforms. As the economic concerns that helped drive pricing lower during that period have faded, Facebook, Instagram, and YouTube have seen pricing trends pick up more swiftly.

While this report highlights the role that Temu has played in Google auctions in the past year, it’s important to note that Temu has invested heavily across the digital ads ecosystem including on Facebook, Instagram, and YouTube. Temu is just one advertiser among many, but they have been a major one, and if they are truly pulling back on digital as Google results suggest, it may ease some pressure on pricing going forward.

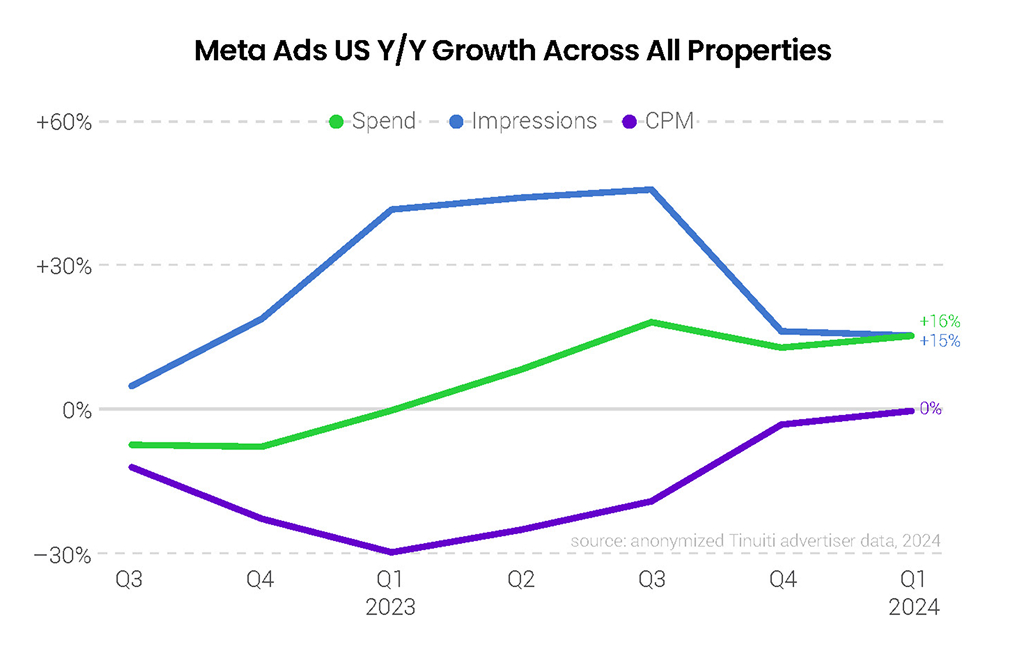

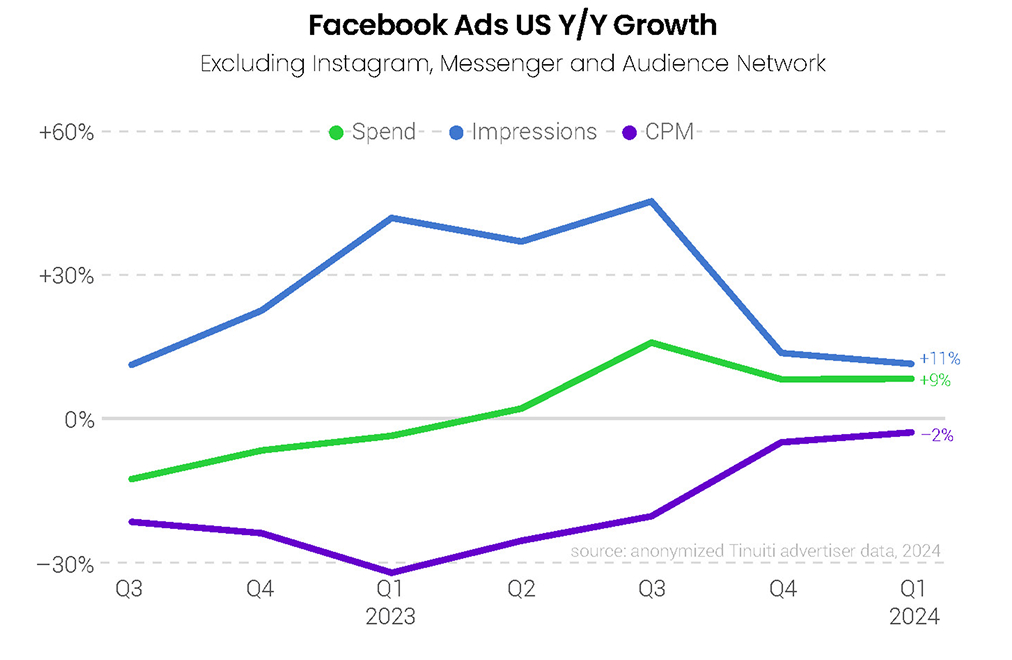

Meta advertising spend continues its rebound from a soft 2022, with Q1 2024 investment up 16% year over year across Tinuiti advertisers, the third straight quarter of double-digit growth. Pricing growth continued its steady rebound, with CPM flat year over year after a 3% drop in Q4, and impressions rose 15%. Reels ad inventory reached new highs across both Facebook and Instagram in the first quarter, helping to drive impression growth with incremental placements.

Facebook CPM fell 2% year over year in Q1, the seventh straight quarter of year-overyear declines, but it was the smallest drop observed over the course of that stretch. While impressions growth fell from 14% in Q4 to 11% in Q1 as advertisers ran up against tougher year-ago comparisons, spend growth accelerated from Q4 2023 to Q1 2024 with a smaller decrease in the cost of ad impressions. Reels inventory helped to boost impressions growth in the first quarter.

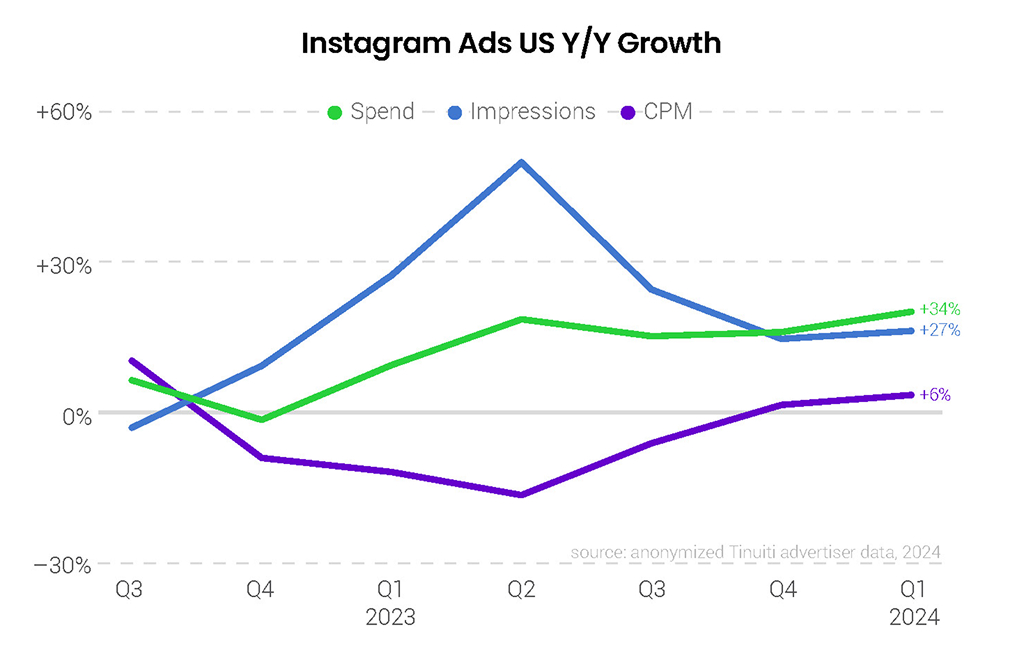

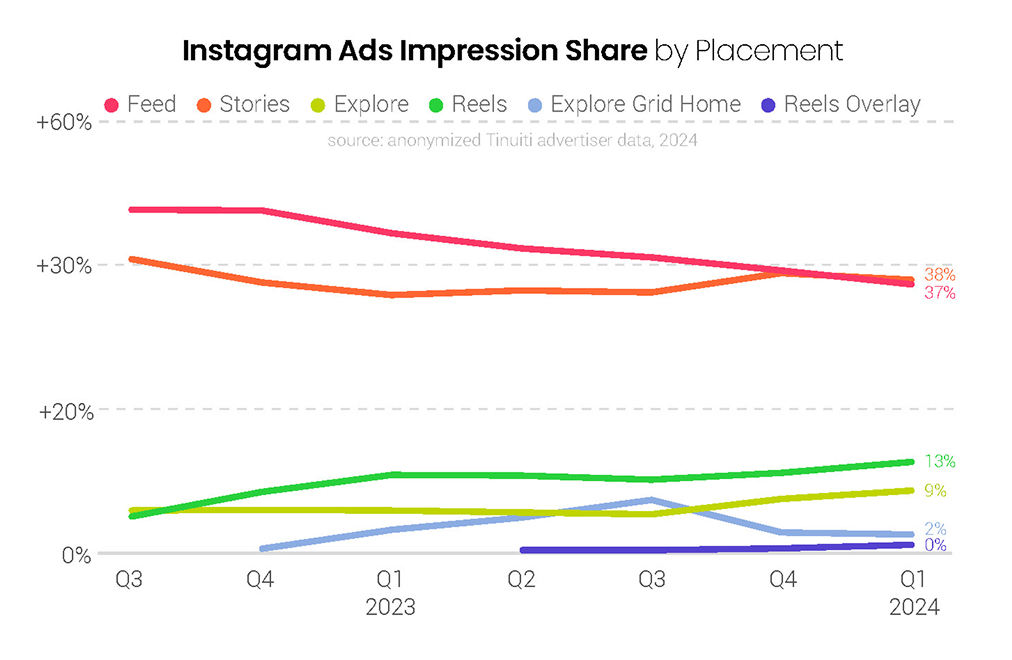

Instagram CPM rose 6% year over year in the first quarter of the year, the second straight quarter of positive growth and up from a 2% increase in Q4. Impressions also grew faster in Q1 than in Q4, pushing spend growth from 27% in Q4 to 34% in Q1, the fastest rate of growth since Q4 2021 for Tinuiti advertisers on the platform. Newer inventory from sources like Reels and Explore is helping push growth along, with combined Feed and Stories impression share hitting an all-time low for Tinuiti advertisers in Q1.

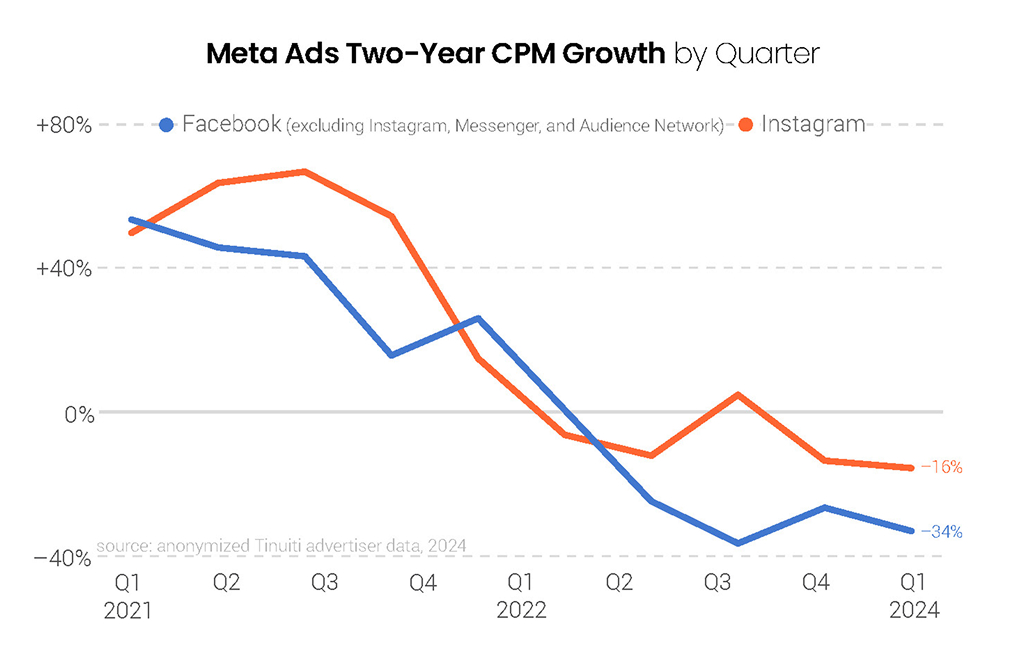

As recently as Q4 2022 Meta advertisers were seeing significant growth on a two-year basis in the cost of ad impressions on both Facebook and Instagram. More recently, however, two-year growth in CPM has been deeply negative for both platforms. This is at least partly the result of the rise in inventory from newer placements like Reels, which have a lower CPM than more established placements like Feed.

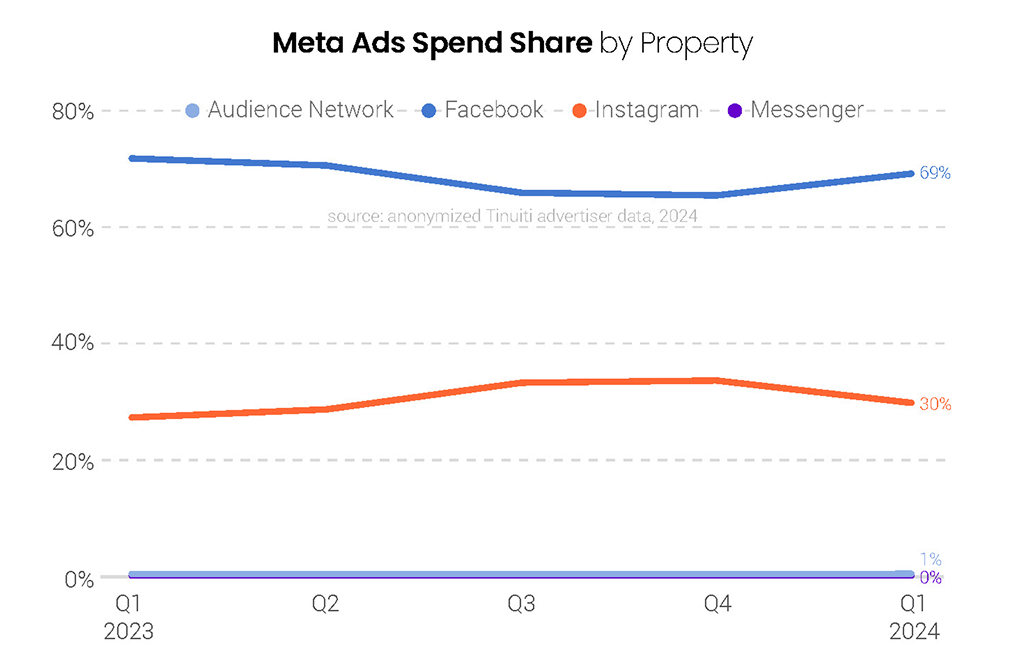

Instagram share of Meta advertising spend rose from 27% last Q1 to 30% in Q1 2024, as Facebook share slipped from 72% to 69%. The Audience Network, which was the platform most impacted by Apple’s App Tracking Transparency update back in 2021, continues to account for only a small share of spend for the vast majority of advertisers. Messenger has yet to become a meaningful source of ad impressions.

Fully 24% of all Meta ad spend for retail advertisers was attributed to Advantage+ shopping campaigns in the first quarter of the year. While this is lower than the 27% observed in Q4, Advantage+ shopping has still grown over the last year, with 19% of retailer spend attributed to the campaign type in Q2 2023. Rolled out in the back half of 2022, Advantage+ has already become an important part of advertising plans across retailers given strong performance for many.

The share of Instagram impressions attributed to Reels video ads hovered around 11% from Q1 2023 to Q4 2023, but rose to 13% in the first quarter of 2024 to reach an all-time high for Tinuiti advertisers. Feed and Stories ads, the two oldest placements on Instagram, combined for 75% of ad impressions, the lowest combined share ever observed for Tinuiti advertisers, as Reels and Explore inventory have grown in importance over the last couple of years.

In the first quarter of 2024, 7% of all Facebook ad impressions were attributed to Reels video ads, with an additional 10% attributed to Reels overlay units. Overlay ads, which appear as banner ads on top of Reels videos, have been an important part of how Meta has monetized Reels views on Facebook for several quarters now. Rolled out to Instagram in 2023, overlay inventory is not yet an important source of ad impressions for that platform.

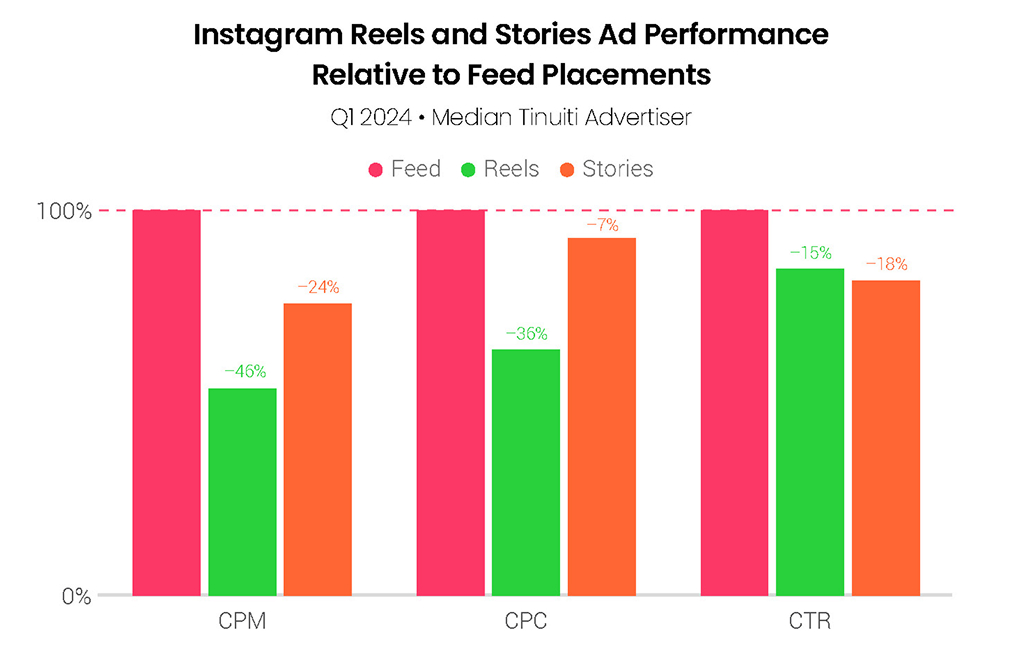

Once again, Instagram Reels CPM was 46% lower than that of Feed in the first quarter of 2024, the same difference observed in Q4 2023. The difference in CPC was smaller, with Reels clicks costing 36% less than Feed clicks, but that marks a much larger disparity than the difference in CPC between Feed and Stories inventory, which are both much more mature placements. Reels CPC should draw closer to Feed as the format matures, though that may take some time.

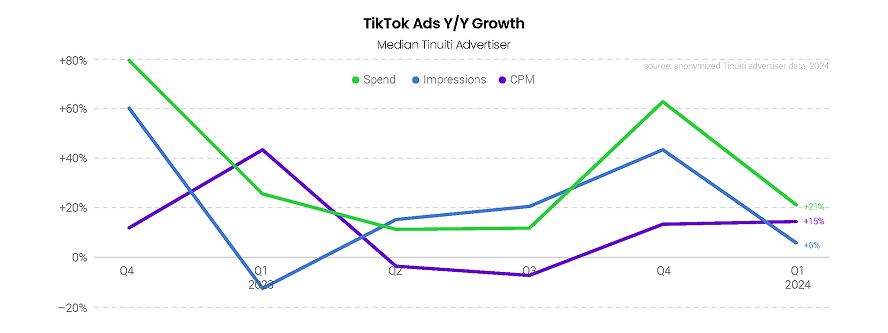

TikTok advertisers increased spend on the platform 21% year over year in Q1 2024, driven by a 6% increase in impressions and 15% growth in CPM. While recent legislation aimed at forcing the sale of TikTok to new ownership is creating many headlines, the platform remains a key part of many US advertisers’ marketing mix given its strong standing with younger generations as well as growing adoption among Americans of all ages.

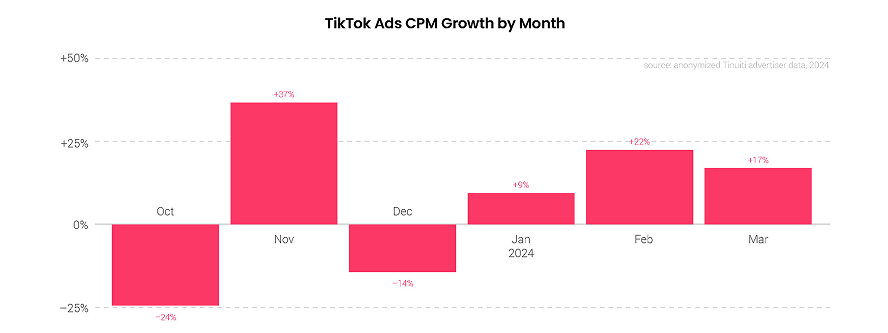

The median TikTok advertiser saw a 14% decline in CPM in the final month of 2023, but that rebounded to a 9% increase in January and advertisers ended the first quarter with a 17% lift in March. The 15% growth in CPM observed in Q1 was the largest increase in CPM since Q1 2023, when the cost of ad impressions rose a whopping 44% year over year. CPM can be impacted by updates to formats and placements over time.

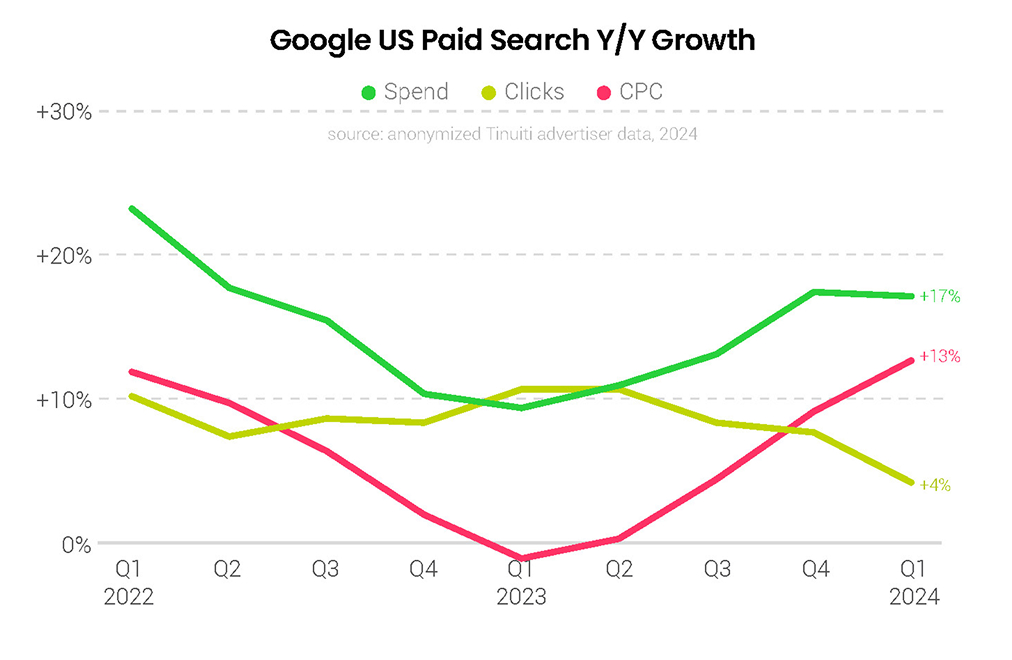

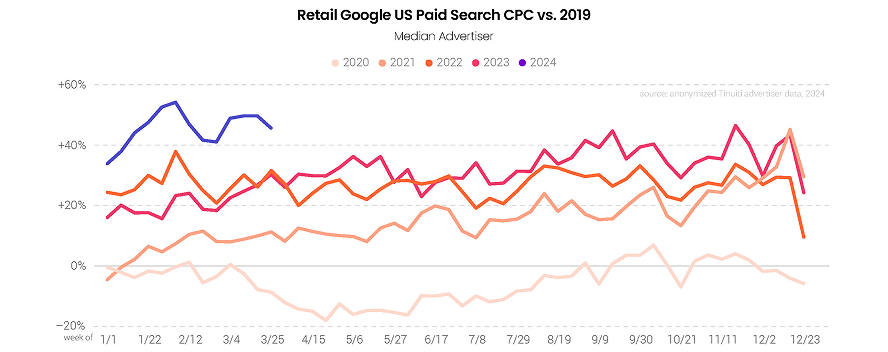

Spending on Google search ads rose 17% Y/Y in Q1 2024, which was unchanged from Q4 2023. The key metrics driving Google spending growth have been shifting significantly in recent quarters, however, with CPC growth accelerating and click growth slowing. In Q1 2024, Google search CPCs were up 13% Y/Y, up from 9% a quarter earlier. Google search CPCs had fallen 1% Y/Y in Q1 2023 as economic uncertainty helped depress ad pricing, but have since been on the rise.

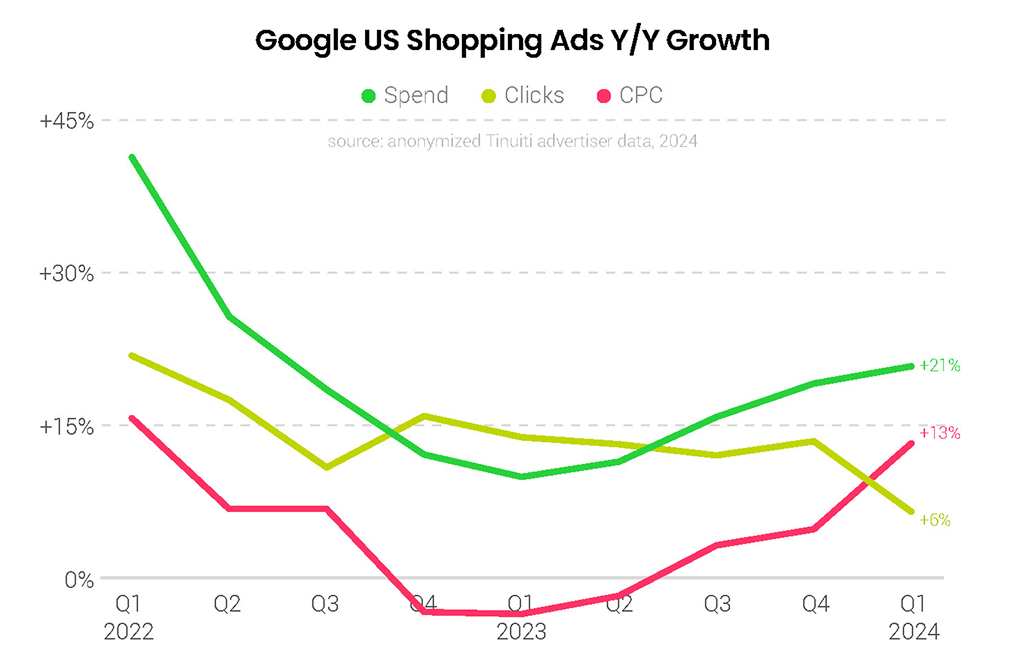

Advertiser investment in Google shopping ads, including both Performance Max and standard Shopping campaigns, rose 21% Y/Y in Q1, up from 19% growth in Q4. That acceleration came despite click growth slowing from 13% in Q4 to 6% in Q1. While CPC growth has strengthened across all Google search ads in the past year, it has picked up the most steam on the shopping side. Shopping CPCs had fallen 3% Y/Y in Q1 2023, but growth has now reached 13% Y/Y in Q1 2024.

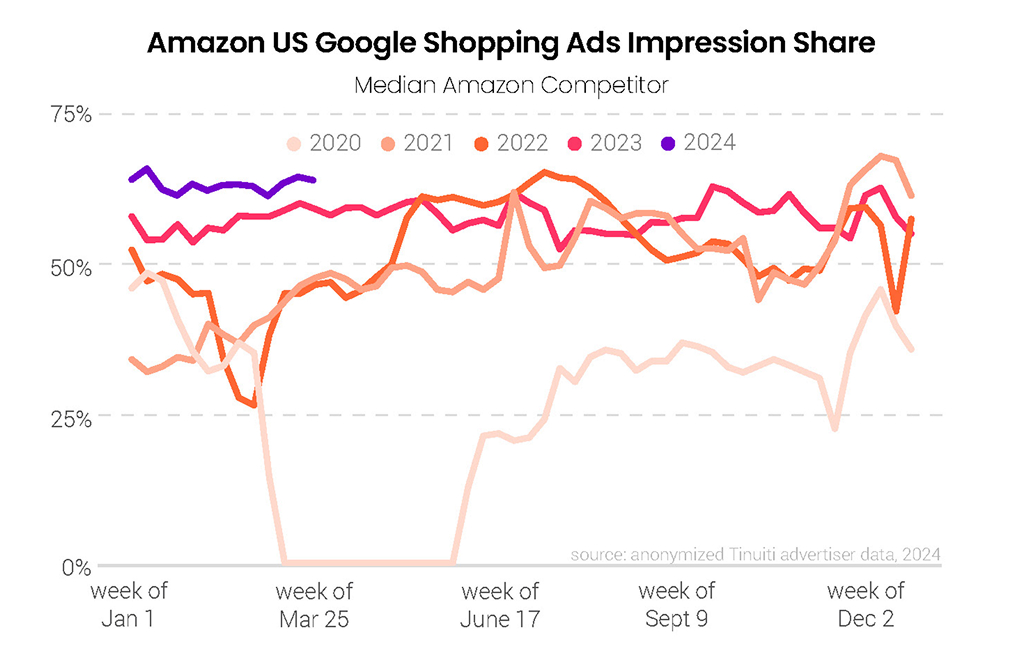

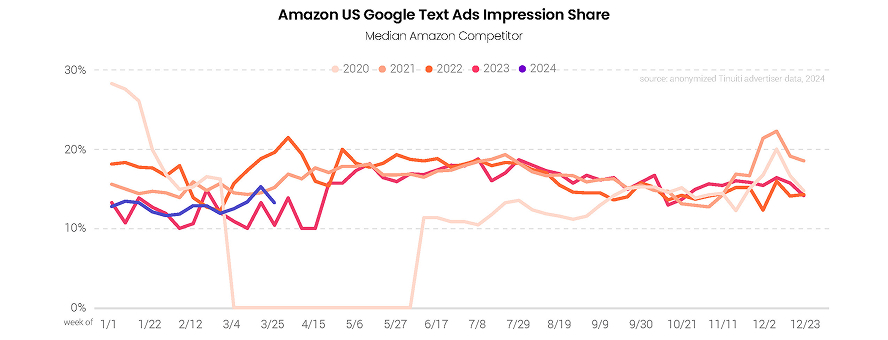

In the face of Temu pouring money into digital and even Super Bowl ads, Amazon appears to have taken a more aggressive stance in Google shopping ad auctions to kick off 2024. Amazon’s first quarter Google shopping impression share was as high as it has been since at least 2020 over the course of Q1 2024. This follows a 2023 that saw Amazon already commanding a relatively strong share of Google shopping impressions for most of the year.

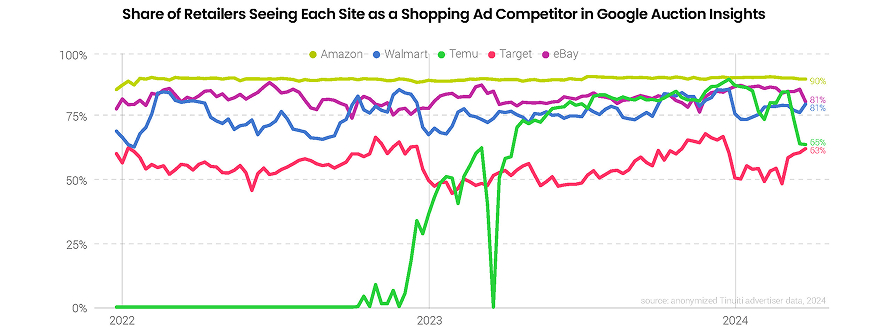

The number of retailers seeing Temu as a top competitor for Google shopping impressions ramped up sharply over early 2023 and ultimately peaked at a level that matched Amazon at the tail end of the 2023 holiday shopping season. Temu’s position in Google auctions seems to have faltered in Q1 2024, though, particularly over the last three weeks of the quarter. At the highest point, 90% of retailers running Google shopping ads saw Temu as one of their top competitors in Google’s Auction Insights report. At the end of Q1 2024, that had dropped to 65%.

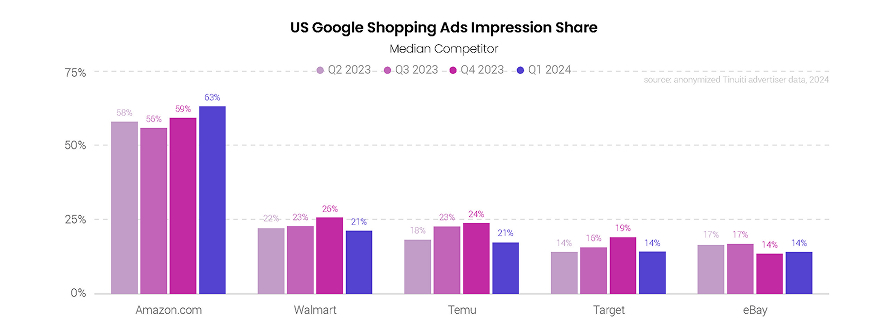

Although Temu may have briefly rivaled Amazon in the number of retailers seeing each as a top competitor for Google shopping impressions, Temu has consistently trailed Amazon by a wide margin in the share of Google shopping impressions each actually receives. That gap only widened in Q1 2024 with Temu seeing a median impression share of 17% against its retail competition to Amazon’s 63% share. Walmart and Target also saw their impression share fall between Q4 2023 and Q1 2024, while eBay saw a small gain.

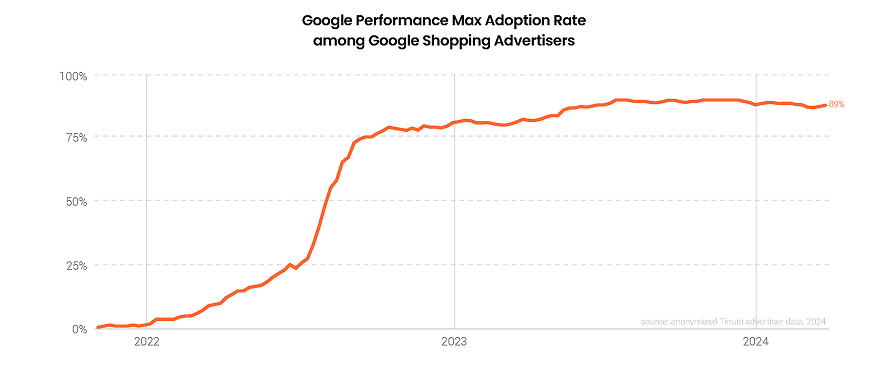

During the height of the Q4 2023 holiday shopping season 91% of retailers placing shopping ads with Google were running Performance Max campaigns. Over Q1 2024, that rate dropped, but only very slightly. On average, 89% of Google shopping advertisers were running PMax campaigns during Q1 2024, which was up from an average of 82% in Q1 2023.

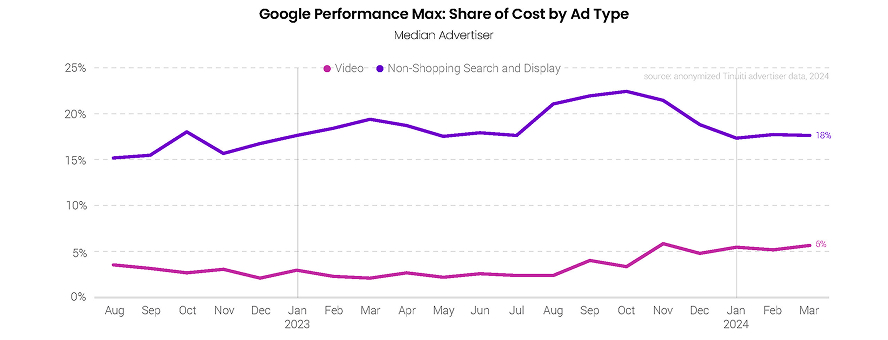

Video and other non-shopping ad inventory accounted for 23% of Performance Max spending in Q1 2024, which was down from 26% in Q4 2023. Video cost share held steady between Q4 and Q1, but non-shopping search and display cost share fell by three points. The non-shopping search and display bucket of PMax costs can include text ads, but Google prioritizes exact match keywords over Performance Max campaigns for scenarios where brands want greater control over their ad serving.

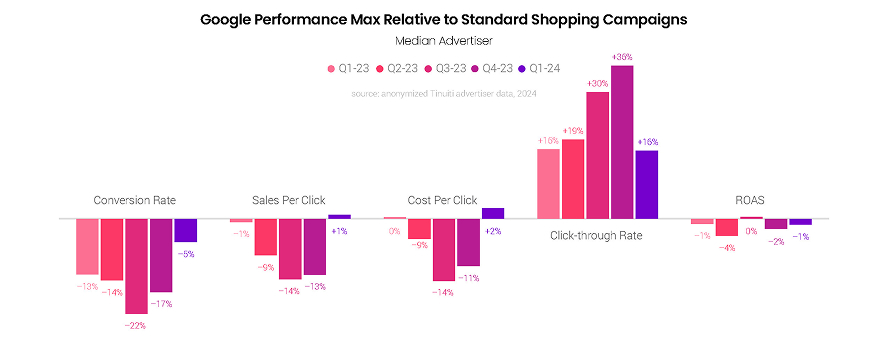

With shopping inventory making up a larger share of Performance Max costs in Q1 than in Q4, the relative performance of PMax campaigns compared to standard Shopping campaigns (SSCs) improved across most key metrics from quarter to quarter. PMax conversion rate was just 5% lower than that of SSCs in Q1, compared to a 17% deficit in Q4. PMax campaigns were able to generate a slightly higher sales per click than SSCs in Q1, although with CPCs running 2% higher for PMax campaigns, their return on ad spend was still 1% lower.

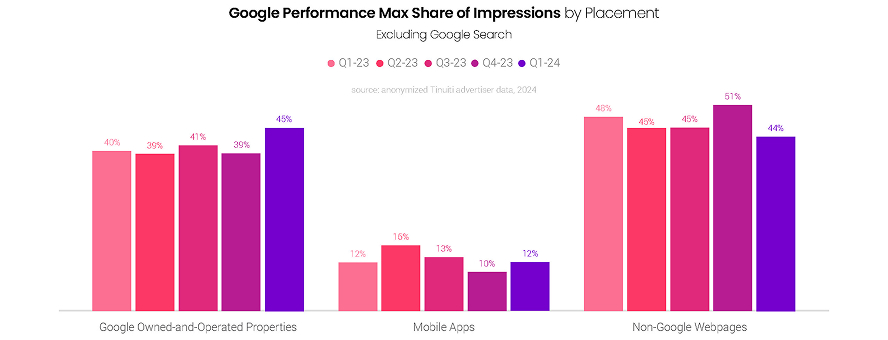

For PMax placements outside of Google search, other Google owned-and-operated properties accounted for 45% of all impressions, the highest level since at least the start of 2023. Google O&O property gains in Q1 came at the expense of nonGoogle webpages, which saw a spike in share during the Q4 holiday season. The share of PMax impressions produced by mobile apps ticked up to 12% in Q1 from 10% in Q4.

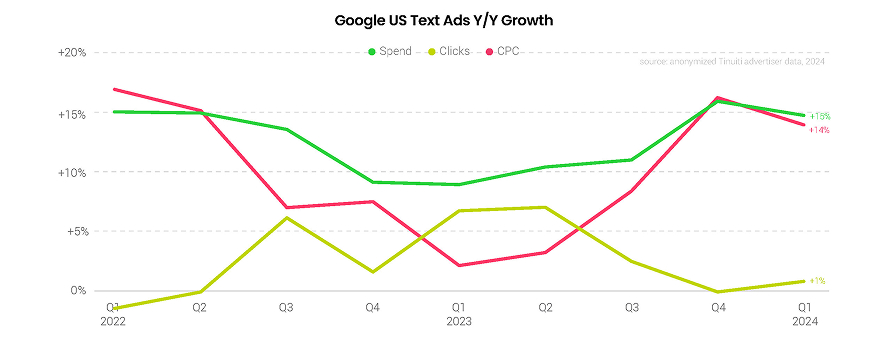

Spending on Google text search ad campaigns was up 15% Y/Y in Q1 2024, down from 16% growth in Q4 2023. Text ad clicks were up 1% in Q1, a slight increase from a quarter earlier, while text ad CPC growth slowed from 16% Y/Y in Q4 to 14% Y/Y in Q1. Although text ad CPC growth slowed, it still slightly outpaced that for Google shopping ads. In fact, text ad CPCs have grown faster than shopping CPCs in all but one of the last 20 quarters.

Advertisers, including Amazon, have historically generated a lower share of impressions for text ads than Google shopping ads and over Q1 2024, Amazon’s average text ad impression share against the typical retailer was 13%, compared to 63% for Google shopping ads. While Amazon’s share of text ad impressions is up slightly compared to 2023, it is still running toward the lower end of where it has been over the last five years.

The typical retail brand running Google search ads has seen its average CPC rise by 40-50% compared to five years ago. In just the last year, from Q1 2023 to Q1 2024, Google retail search ad CPCs rose about 20% for the median advertiser. Temu making a heavy investment in digital ads and Amazon appearing to counter by running Google ads more aggressively has put pressure on retail CPCs. CPC growth was also depressed in early 2023 due to uncertainty around the macroeconomic picture.

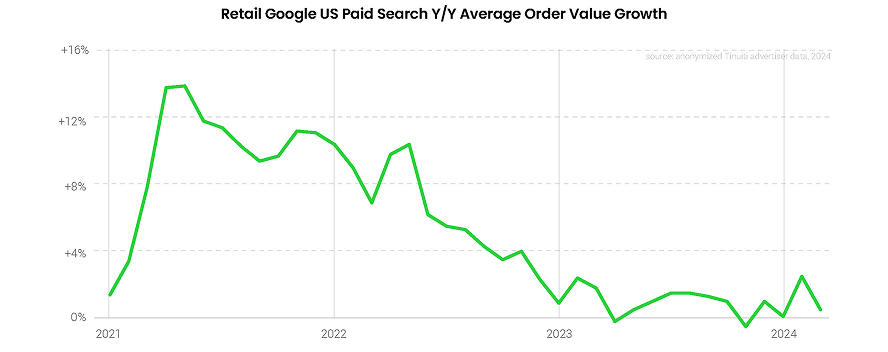

The current rise in Google search CPCs is coming at a time when inflation has generally cooled in the US and, more directly related, advertisers are seeing only small increases in the average value of orders generated by search ads. 12/23 Google search AOVs were up by an average of 1% over the course of Q1 2024, just a slight increase from roughly flat growth in Q4 2023.

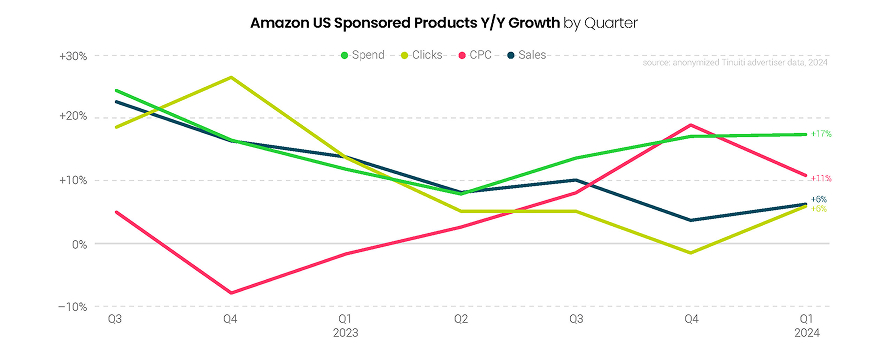

Amazon advertisers increased investment in Sponsored Products 17% year over year in Q1 2024, the same rate of growth observed in Q4 2023. While CPC growth decelerated from 19% to 11%, click growth rebounded from a 2% decline in the final quarter of 2023 to 6% growth in the first quarter of the year, the strongest increase in clicks since Q1 2023. While the reach of Sponsored Products was extended to sites off of Amazon in 2023, this inventory has yet to produce a meaningful share of ad traffic for advertisers.

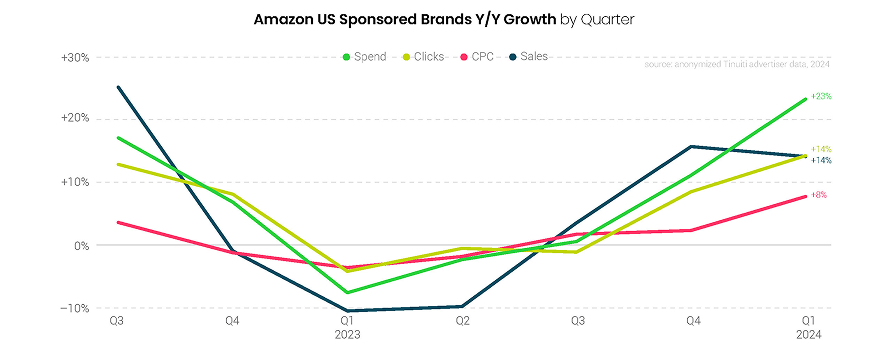

Amazon Sponsored Brand advertisers decreased ad spend 8% year over year in Q1 2023, but growth rebounded in the first quarter of 2024 to 23%, the fastest growth for Tinuiti advertisers in more than two years for the format. Click growth accelerated from 9% in Q4 2023 to 14% in Q1 2024, while CPC growth ramped up from 2% to 8%. Sales attributed to the format rose 14% in the first quarter, the second straight quarter of double-digit increases.

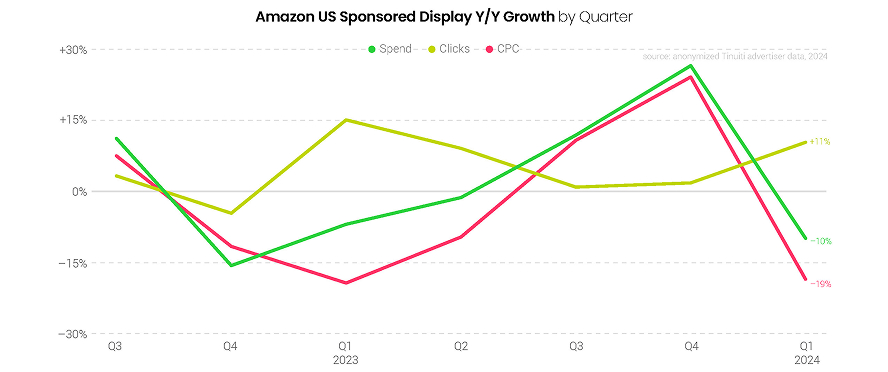

Cost per click for Sponsored Display campaigns decreased 19% year over year in the first quarter, pulling spend down 10% compared to the same quarter last year even as clicks rose at the fastest rate since last Q1. While many Sponsored Display campaigns are still targeted using cost per click, advertisers do have the option to bid on the format based on the cost of viewable impressions.

Amazon advertisers spent 82% of all Ad Console investment on Sponsored Products campaigns in the first quarter of 2024, with 15% attributed to Sponsored Brands and 3% going to Sponsored Display. While Sponsored Products campaigns have not yet materially been boosted by Amazon’s move to extend their reach to partner sites like Pinterest, this inventory may only help to bolster the format’s standing as the biggest investment for advertisers.

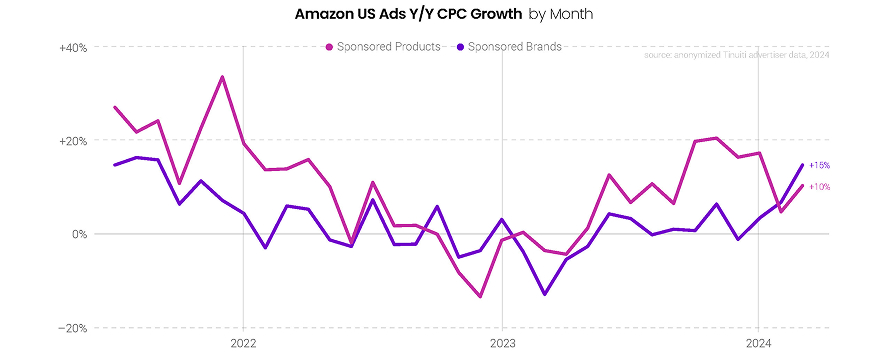

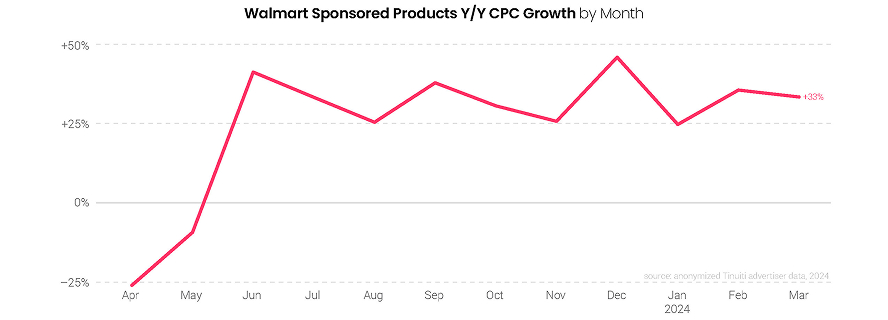

For the first time since November 2021, CPC for both Amazon Sponsored Products and Sponsored Brands rose at least 10% year over year in the same month in March 2024. While Sponsored Products CPC growth slowed from 17% in January to 10% in March, Sponsored Brands CPC growth ramped up from 3% in the first month of the year to 15% in the final month of the first quarter.

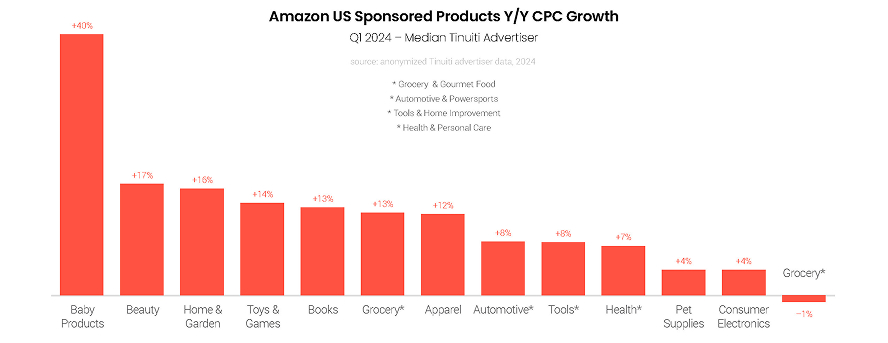

The median advertiser in twelve of the thirteen product categories studied for this report saw positive CPC growth in the first quarter of 2024, with double-digit increases for more than half of these product categories. Baby products saw the biggest CPC increase at 40% year over year, while sports products were the only category to see a decrease, albeit a slight one, at a 1% decline for the category.

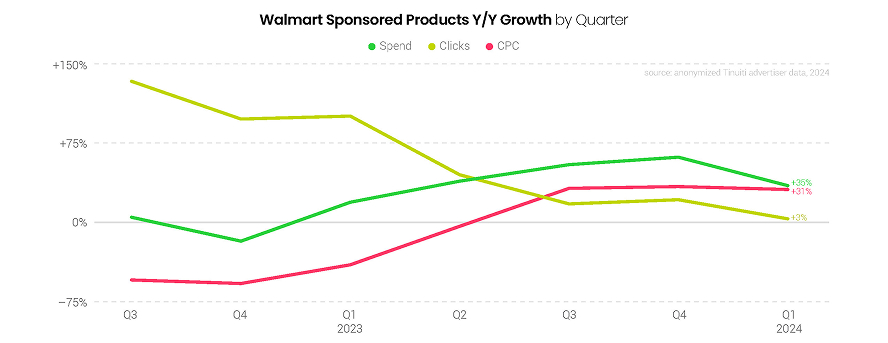

Advertisers ramped up investment in Walmart Sponsored Products by 35% year over year in Q1 2024, with clicks up 3% and CPC up 31% for the quarter. CPC has now grown by at least 30% year over year in each of the last three quarters, as advertisers are lapping periods of significant CPC decline that were caused by Walmart’s transition to a second-price auction in 2022. Year-ago CPC growth comparisons will firm up meaningfully in the second quarter.

The cost of Walmart Sponsored Products clicks has grown meaningfully for much of the last year as advertisers lapped weak comparisons from 2022. Walmart’s change in Q2 2022 from a first-price auction to a second-price auction sent CPC crashing down, as advertisers no longer had to pay the full price of the bid placed and now pay only just enough to beat the advertiser directly below them in ad auctions.

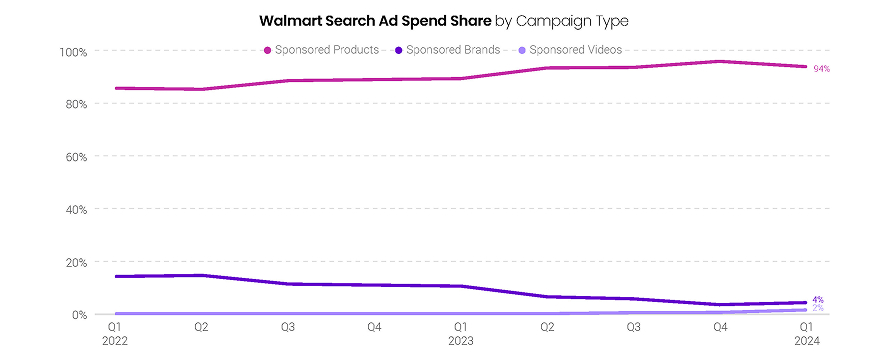

Walmart’s most recently released search ad format, Sponsored Videos, rose from 1% of Walmart search ad spend in the final quarter of 2023 to 2% in Q1 2024. Sponsored Brands, formerly known as Search Brand Amplifier, accounted for 4% of Walmart search spend. Sponsored Products ads continued to account for more than the vast majority of Walmart search ad investment, much like the Sponsored Products format does for Amazon advertisers on that platform.

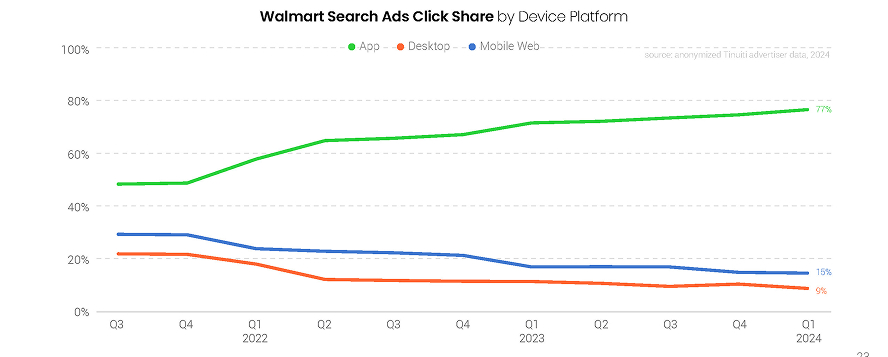

Over the last three years, the share of Walmart search ad clicks coming from the Walmart app rose from less than half to more than 75%, as the importance of the app to both consumers and advertisers grows. The mobile web accounted for another 15% of search ad clicks in Q1. Between the app and mobile web, mobile shopping is clearly the dominant method for consumers looking to search on Walmart, with less than 10% attributed to desktop computers in the first quarter of the year.

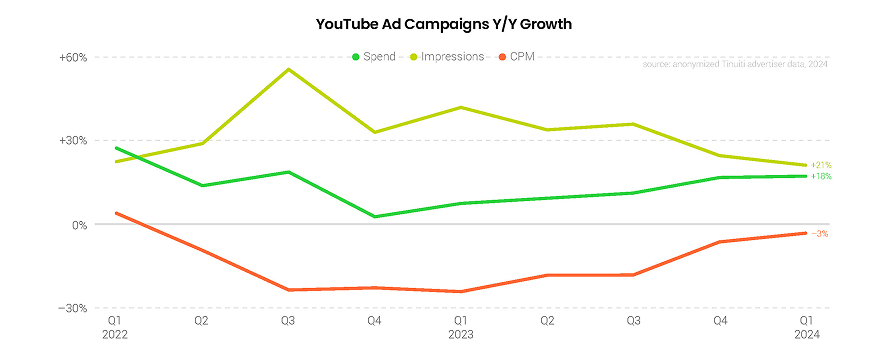

Spending on YouTube video ad campaigns rose 18% Y/Y in Q1 2024, up from 17% growth a quarter earlier. YouTube impression growth slowed from 25% Y/Y in Q4 to 21% Y/Y in Q1, but ad pricing trends continued to strengthen. Although CPMs were still down 3% Y/Y in Q1, that was the smallest CPM decline YouTube advertisers have seen in two years. Importantly, YouTube inventory, including on Shorts, is also available through Demand Gen and Performance Max campaigns.

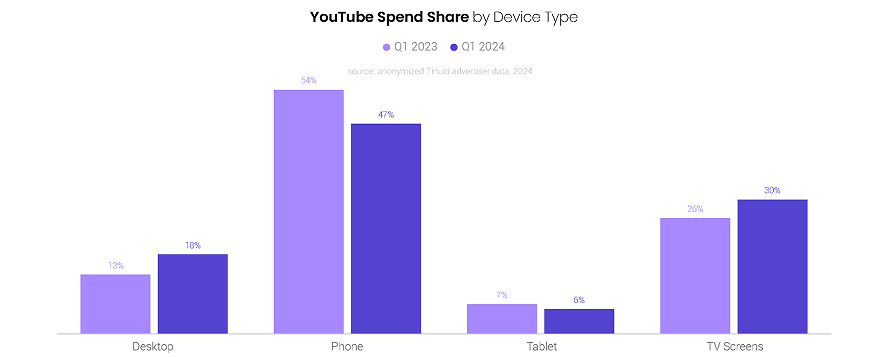

YouTube ad spending attributed to TV screens was up 36% Y/Y in Q1 2024 and the share of total YouTube spending produced by TVs rose to 30%, up from 26% a year earlier. Phones still account for the largest share of YouTube spending at 47%, but that rate was down from 54% in Q1 2023. Desktop and laptop computers contributed 18% of YouTube spending in Q1 2024, while tablets contributed 6%.

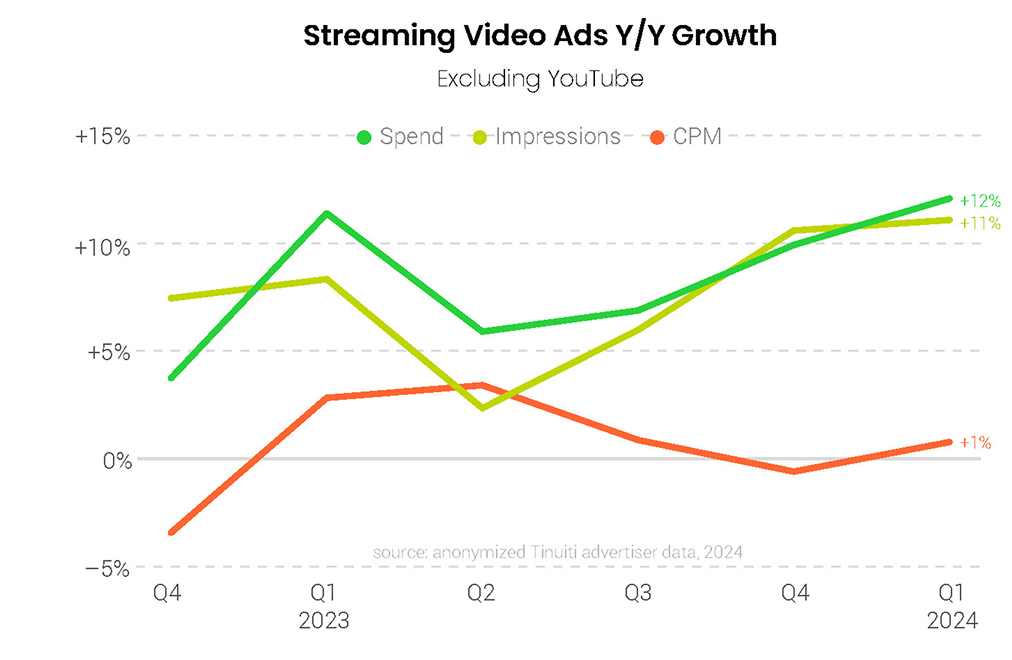

For streaming video ads outside of YouTube, including on major platforms like Hulu, Netflix, Max, and Disney+, spending grew 12% Y/Y in Q1 2024, up from 10% growth a quarter earlier. Streaming video ad impression growth held steady at 11% Y/Y while average CPM grew 1% Y/Y, up from a 1% decline in Q4. As more premium inventory has come online in recent quarters, streaming CPMs have averaged a 2% quarterly increase since 2023 even as YouTube has seen an average quarterly CPM decline of 14%.

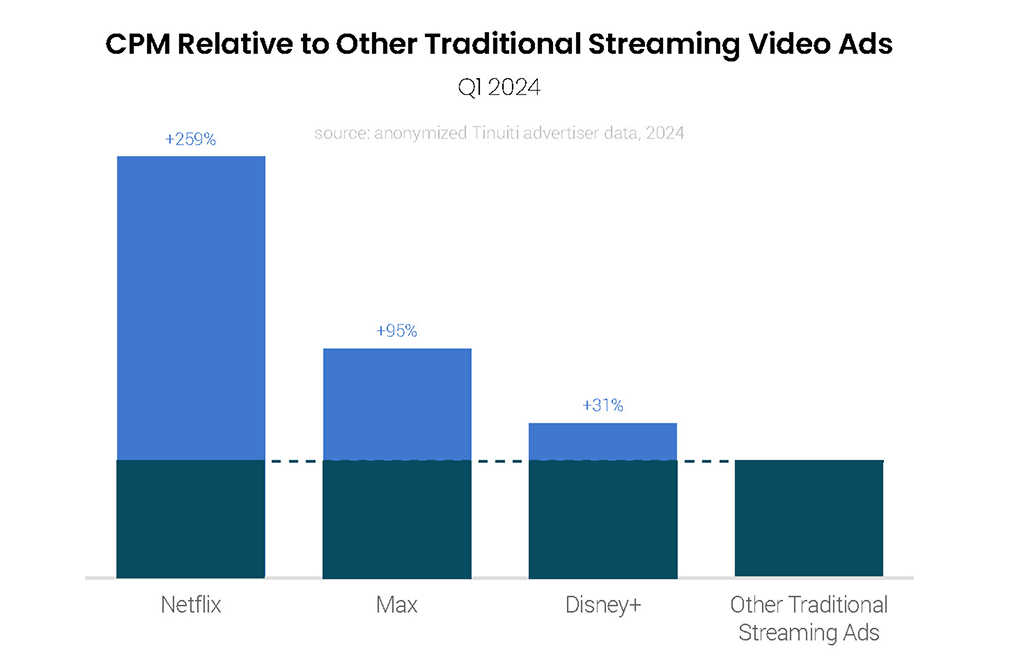

Relative to other traditional streaming video ads, Netflix, Max, and Disney+, all saw strong CPMs in Q1 2024. Netflix outpaced its marquee competitors with its advertisers paying 3.6 times as much for Netflix ads as they did for other non-RTB purchased streaming video ads. For Max, the typical advertiser paid twice as much for Max ads as they did for other traditional streaming ads, while Disney+ advertisers paid 31% more for Disney+ ads than other streaming ads.

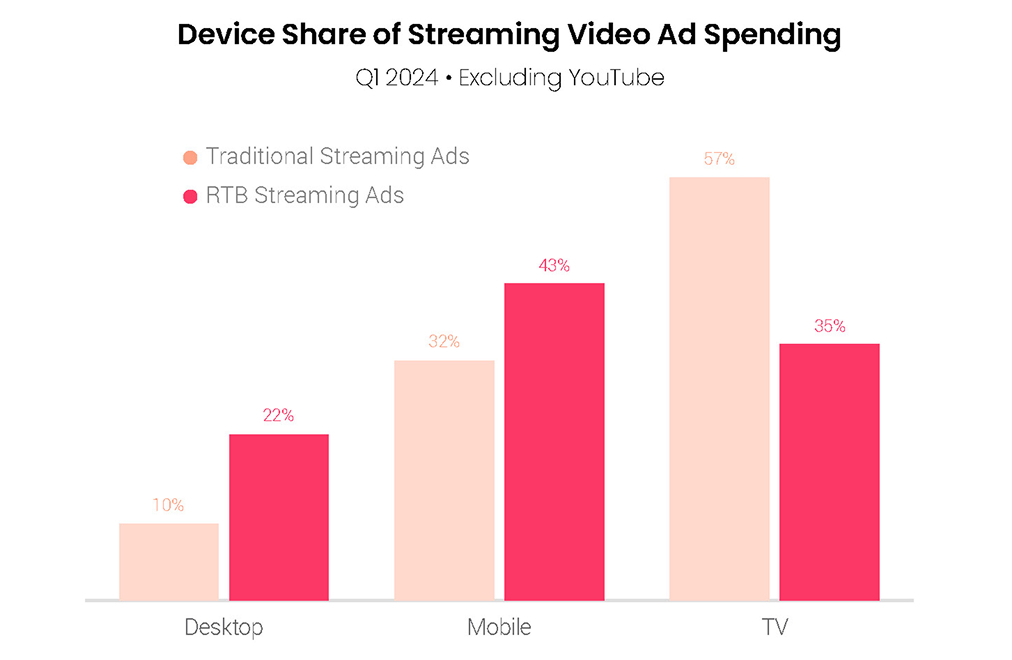

TV screens accounted for 57% of traditional streaming ad spending in Q1 2024, compared to 35% of spending on streaming inventory purchased through real-time bidding. For RTB streaming ads, mobile accounted for the largest share of spending at 43%, while desktop accounted for another 22%. For traditional streaming ads, mobile produced 32% of spending, while desktop produced just 10%.

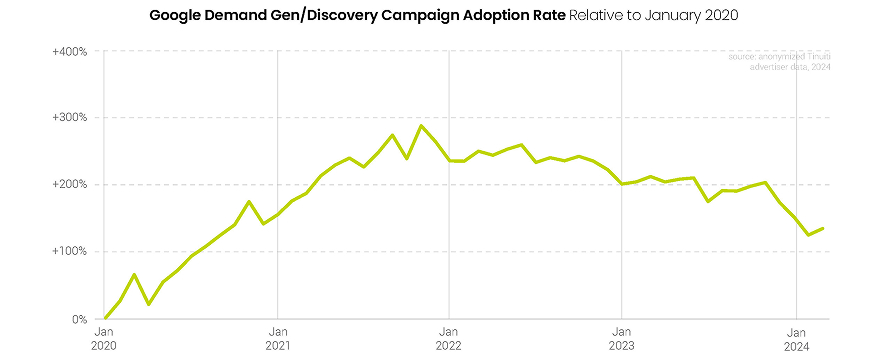

In Q4 2023, Google began the process of transitioning its Discovery campaigns to Demand Gen campaigns. The new model opened up additional inventory, including from YouTube Shorts, as well as other new ad options. While Demand Gen campaigns saw a slight bump in adoption in November 2023, adoption rates were down in Q1 2024. Adoption of Discovery campaigns also peaked in November 2020 and 2021 before running lower to start the following years.

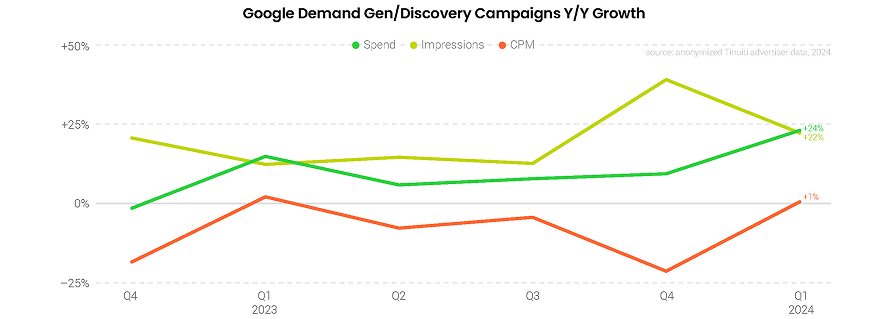

For brands that remained active on Discovery/Demand Gen campaigns in both Q1 2023 and Q1 2024, spending was up 24% Y/Y in Q1, up from 10% growth in Q4. Impression growth cooled from the big jump of 40% Y/Y brands saw in Q4, but pricing also recovered from the significant drop advertisers saw to close out 2024. Ultimately, Demand Gen impressions were up 22% Y/Y in Q1 while average CPM was 1% higher.

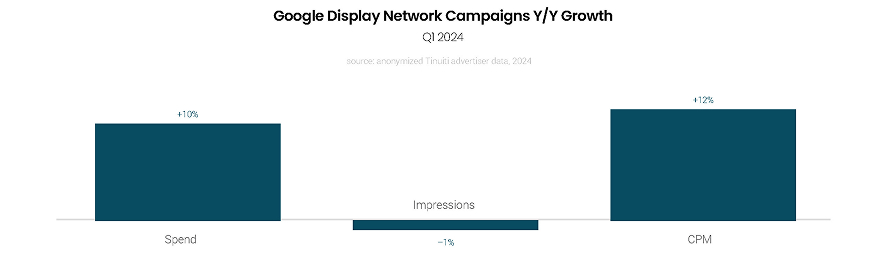

Advertiser spending on the Google Display Network (GDN) was up 10% Y/Y in Q1 2024, up from 6% growth in Q4 2023. GDN impressions were down 1% Y/Y in Q1, but that was up from a 10% decline in Q4. Average GDN CPM was up 12% Y/Y in Q1, down from 17% growth in Q4. While about half of GDN spending went to standard display campaigns in Q1, the remainder was spent on app and video inventory.

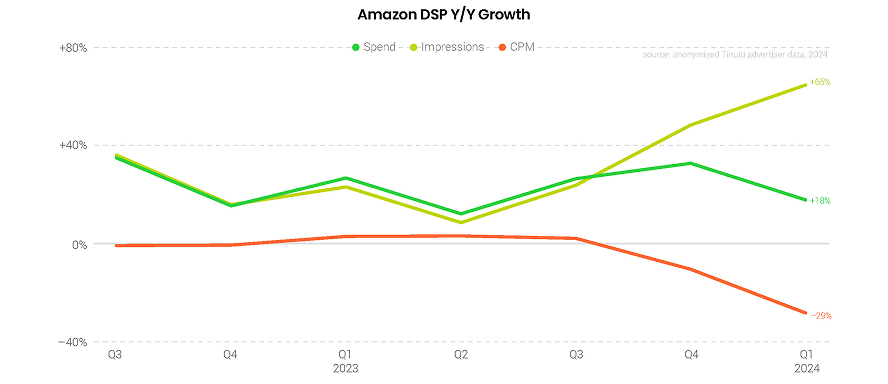

Brands investing in the Amazon demand-side platform (DSP) increased spend 18% year over year in Q1 2024. While this represents a slowdown from the 33% growth observed in Q4, the moderation is largely a result of tougher year-ago comparisons, as spend growth ramped up from 15% Y/Y in Q4 2022 to 27% in Q1 2023. Impression growth has been particularly strong in recent quarters, hitting 65% Y/Y in Q1 after 49% growth in Q4.

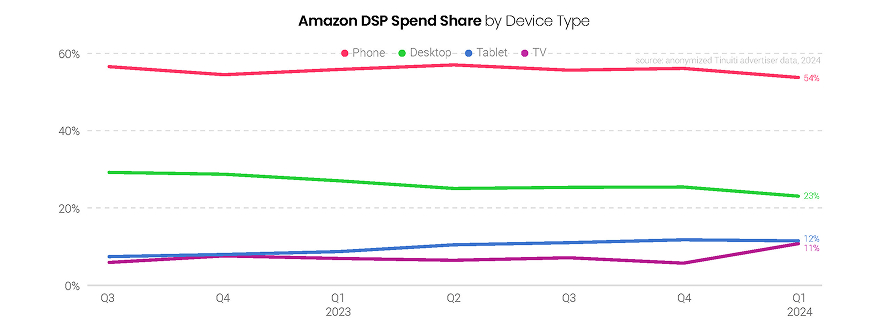

While more than half of Amazon DSP spend is still attributed to phones, connected TV has gained spend share over the last couple of years, and in Q1 2024 accounted for 11% of spend. That’s up from 7% of spend last Q1, and TV share of DSP spend is likely to continue to grow with the introduction of Prime Video ads to the available inventory sources. Both phones and desktop showed declines in spend share from Q4 to Q1 with the rise in TV share.

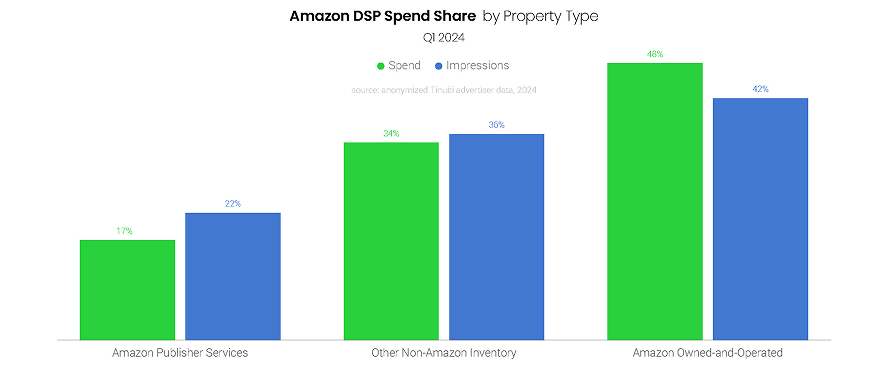

The share of total Amazon DSP investment attributed to Amazon owned-and-operated (O&O) sites, including the Amazon website and app, slipped from 53% in Q4 to 48% in Q1. Just 42% of impressions in the first quarter were attributed to O&O inventory, as ad placements on Amazon O&O properties carry a higher CPM than other DSP placements. A larger contribution from cheaper inventory sources is partly the reason for overall Amazon DSP CPM declining more in Q1 than in Q4.

Check out our most recent Digital Ads Benchmark Report for more exclusive insights.