2024 Beauty Marketing Study

How New Platforms, Changing Technology, and the Rise of Gen Z Are Shaping Beauty Shopping

How New Platforms, Changing Technology, and the Rise of Gen Z Are Shaping Beauty Shopping

Beauty shopping habits continue to evolve as the rise of new digital platforms, rapidly changing technology, and the growing buying power of Gen Z are all pushing brands to adapt their marketing strategies to meet shoppers through the channels that matter most to them with messaging that resonates. To help marketers better understand the modern beauty customer journey, Tinuiti surveyed 1,021 US beauty shoppers in April 2024 on everything from the use of AI for personalized beauty recommendations, to where TikTok users will turn for beauty recommendations if the platform is banned.

When asked how their current beauty spending stacked up to the same time last year, 38% said they’re spending more, while 37% responded that their expenditures are about the same. Among the highest earners, those with household incomes of $200,000 or more, 52% said they were spending more on beauty products than a year ago. Just 33% of those earning less than $50,000 a year said they were spending more.

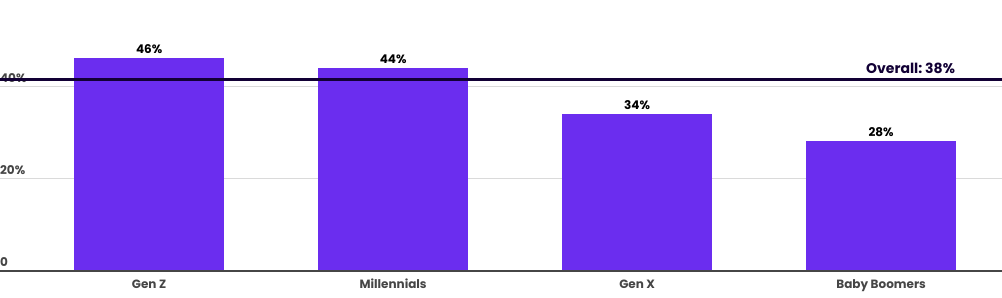

Younger generations were also more likely than average to say they are spending more on beauty products now than a year earlier. Among Gen Z, 46% said they are spending more now, while just 28% of baby boomers said the same.

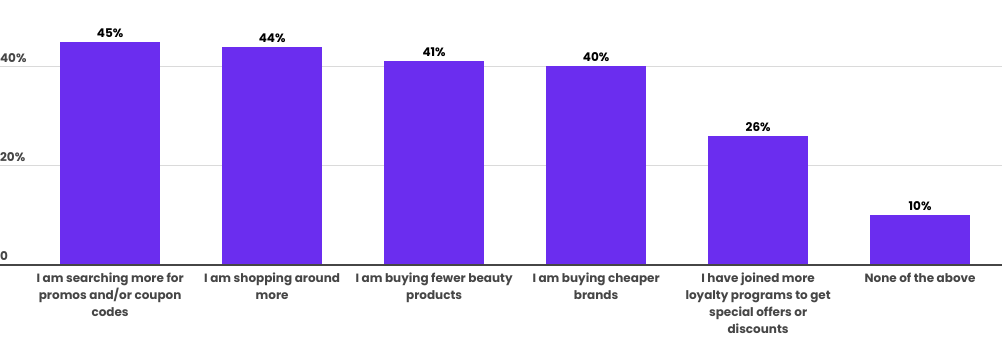

While most respondents say they’ve kept their beauty expenses at least where they were at the same time last year, inflation is still having an impact on shopping habits, with 45% saying they’re searching for more promos and/or coupon codes and about the same share is shopping around more.

All told, 41% of respondents say they’re buying fewer beauty products because of inflation, such that the relatively positive responses regarding current beauty spending compared to last year may have still involved cuts in the number of beauty products purchased.

Looking to the year ahead, 27% of respondents expect to buy more beauty products either in store or online relative to the year prior, compared to just 17% who expect to buy less, a promising sign for demand moving forward.

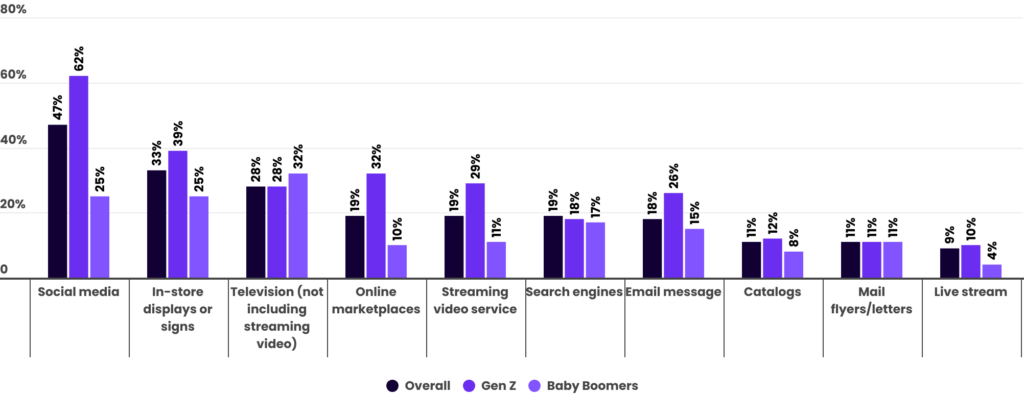

The most popular response by a wide margin for where respondents recalled first seeing or hearing about a new beauty product that they later went on to purchase in the past year was social media, with 47% choosing this channel. Second place went to in-store signs and displays at 33%, highlighting the continued importance of brick-and-mortar stores to beauty product discovery.

Traditional television placed third for product discovery at 28%, meaningfully outpacing streaming video services which was only selected by 19% of respondents. Growth in streaming video consumption combined with the arrival of new major ad-supported options such as Prime Video ads, will likely lead to a higher share of shoppers who are exposed to ads on streaming video services over the coming years.

Social media was especially important for product discovery for Gen Z, with 62% recalling hearing about a new beauty product on social media in the past year that they later went on to purchase. Streaming video services were also a relatively popular product discovery channel for Gen Z, with 29% selecting that option, which outpaced traditional TV at 28%.

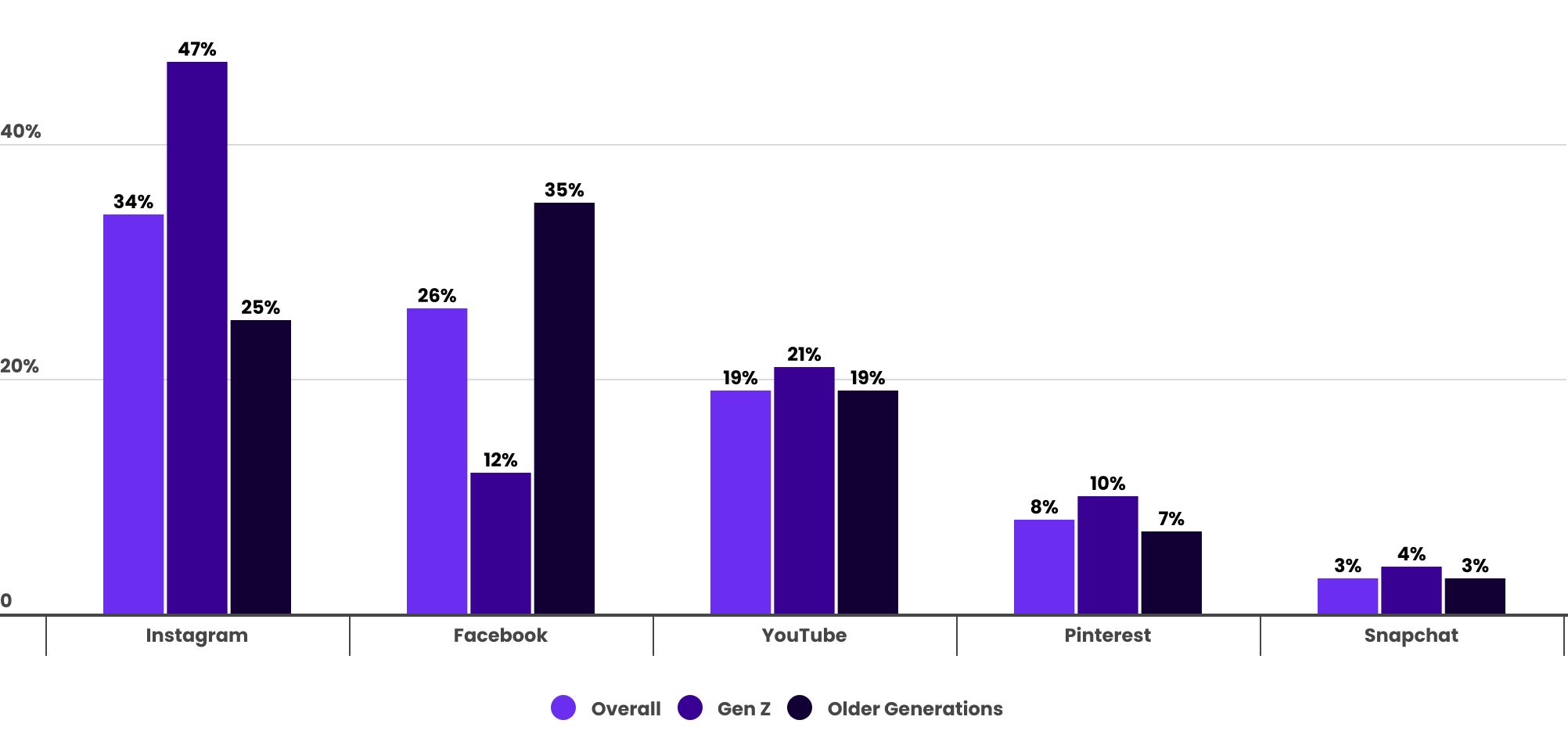

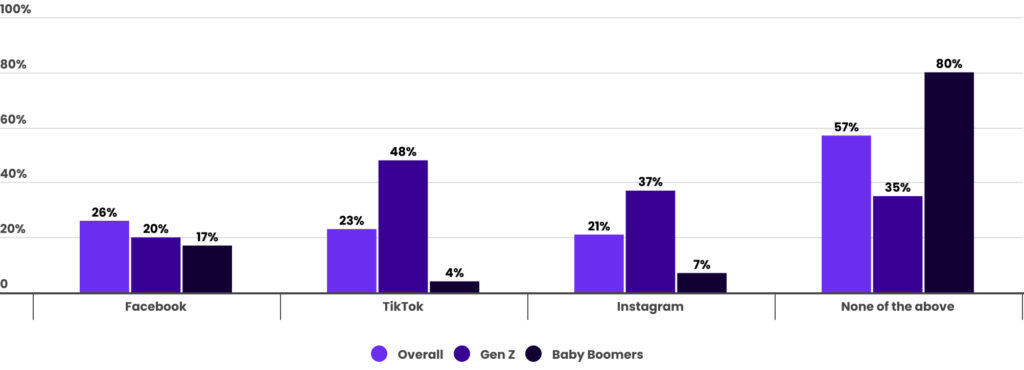

For Gen Z, 47% of respondents who picked TikTok as the social platform where they most often discover beauty products said they would turn to Instagram if TikTok were banned. For older generations, that rate was 25%. YouTube saw less variation as a TikTok alternative across generations, with 21% of Gen Z picking it, along with 19% of older generations.

Fully 43% of respondents say they’ve completed surveys/questionnaires on their skin/hair type in order to receive more personalized beauty product recommendations and experiences. Nearly 30% of respondents said they’ve done personal in-store consultations, as both in-store display and personnel are key for beauty product discovery and consideration.

Younger generations were more likely to seek out personalized recommendations through any of the five methods asked about it in this survey with only 19% of Gen Z saying they had not tried any of the options, compared to 57% of baby boomers

Across generations, just 16% and 10% of respondents say they’ve used artificial intelligence or augmented reality for more personalized beauty experiences, respectively. However, 39% of respondents said they have used technology such as filters to see digitally how a beauty product would look on them before purchasing, as some consumers may be unaware of the incorporation of AR/AI into filter technology.

Over half of Gen Z respondents said that they had virtually tried out a beauty product before purchasing, while nearly half of millennials had as well. This compares to just 33% of Gen X and 19% of baby boomers.

Asked how they approach beauty purchases, 41% of respondents say they typically buy the same exact products, while 29% tend to try different products within the same brands. Fully 30% of beauty shoppers say they usually look for new brands to try.

When it comes to what influences beauty purchases the most, 69% of respondents selected price as one of the three most influential factors, the most popular answer. Quality was a distant second at 56%, and no other factor garnered more than 35% of responses.

Gen Z was the most open to buying new beauty products with just 35% saying they tend to buy the exact same products, compared to 43% for older generations. As a result, brand name and familiarity were also less influential factors for Gen Z. Instead, Gen Z was much more likely than older generations to say that influencers were a top factor in their beauty purchases, with 23% picking that option compared to just 2% for baby boomers.

Across all respondents, 65% purchased a beauty product based on the recommendation of an online influencer over the past year, with 14% saying they do so frequently or very frequently. For Gen Z, 85% said they had bought a beauty product in the past year based on an influencer recommendation, with 19% doing so frequently.

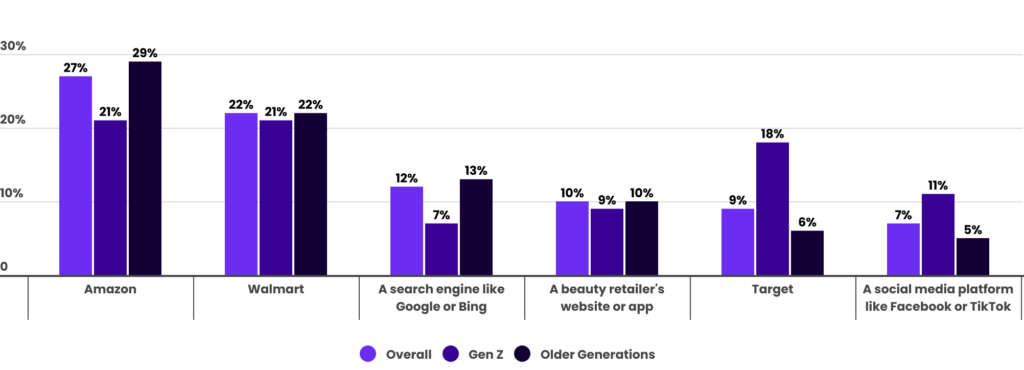

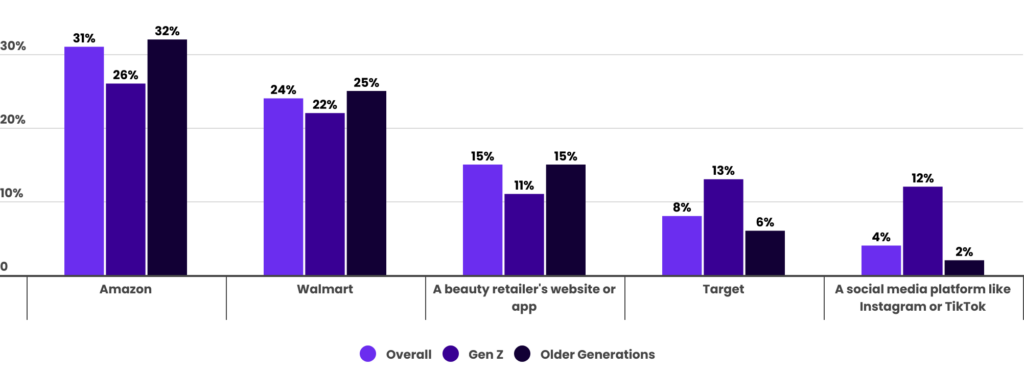

Respondents chose Amazon and Walmart as the top two online destinations for beauty product searches. These were also the top selections for online beauty product purchases, with Amazon the most likely website or app for 31% of respondents and Walmart coming in second at 24%.

For both Amazon and Walmart, the share of respondents who said they were a top site or app for purchases topped the share who identified them as top spots for online searches, highlighting their importance as bottom-of-the-funnel destinations for shoppers ready to convert.

Social media platforms are becoming a destination for product searches for some shoppers, with 7% of respondents selecting a social platform as the place they’re most likely to start online beauty searches. Just 4% said it’s their top destination for purchases, however, as social commerce is still in the early stages in the US.

For Gen Z, Target was a close third for beauty searches behind Amazon and Walmart with 18% choosing it, compared to just 6% for older generations. Gen Z was also more likely to start beauty searches on a social platform with 11% choosing that option. The search share gains for Target and social among Gen Z primarily came at the expense of Amazon, with Walmart being roughly equally popular for Gen Z and older generations.

While social platforms may not be a top destination for beauty product purchases, over 40% of respondents said that they have purchased a beauty product directly on one of Facebook, Instagram, or TikTok at least once. This share may be inflated by some confusion regarding when purchases occur directly on a social platform compared to when users see a listing on social media but navigate off of the social platform to convert on a different website/app.

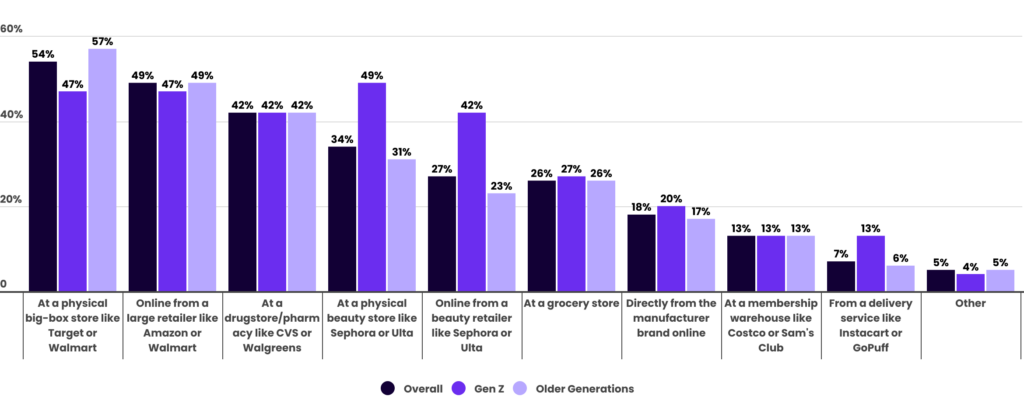

While online shopping is hugely popular among beauty shoppers, the most commonly selected destination for beauty purchases over the past year was big box stores like Target or Walmart with 54% of respondents. That was followed by online purchases from large retailers like Amazon and Walmart, with drugstores/pharmacies like CVS or Walgreens rounding out the top three.

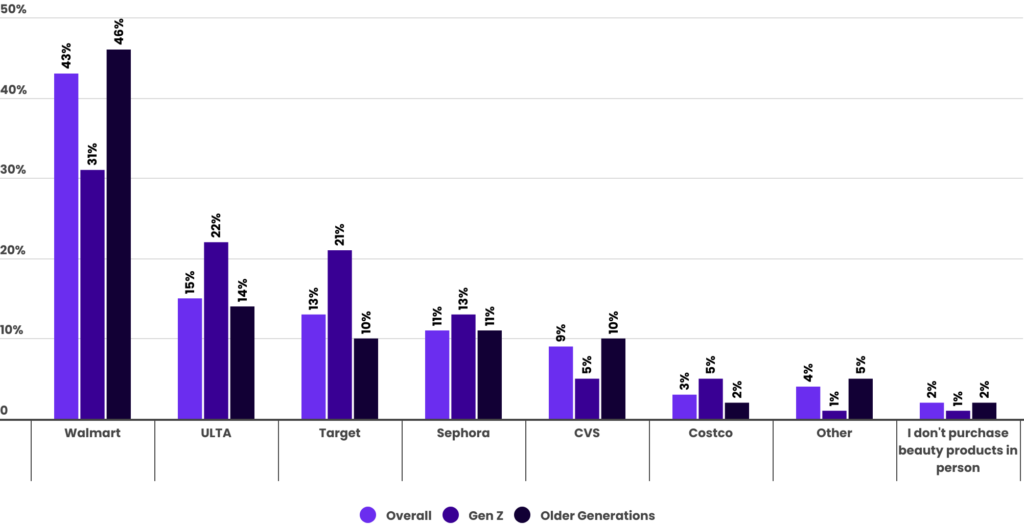

Asked where they’re most likely to make in-person beauty purchases, 43% of respondents selected Walmart, the top choice. ULTA came in second with 15% of shoppers, followed by Target at 13%.

ULTA and Target were both more popular in-store choices among Gen Z, with 22% and 21% selecting each respectively. Just 31% of Gen Z picked Walmart as their preferred retailer for buying beauty products in person, well below the 46% level Walmart hit among older shoppers.

Even when they’re in a physical store, many beauty shoppers turn to online sources for additional information. Fully 40% have searched for a product/brand on a search engine while in-store, and 37% have visited the store’s website.

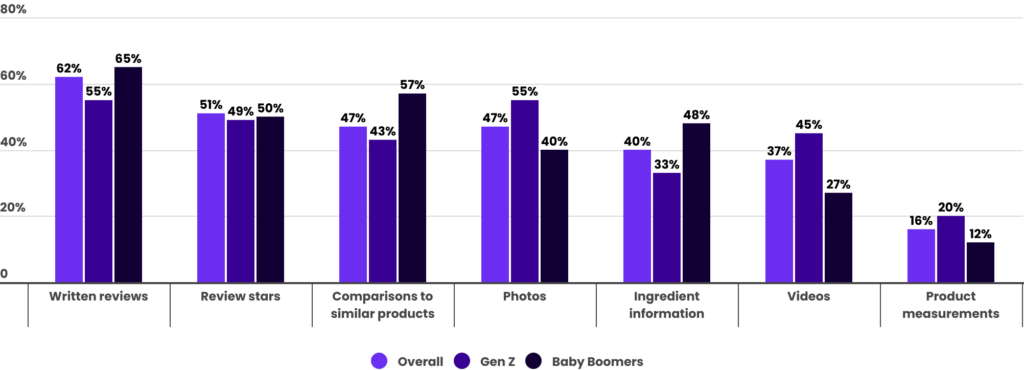

Asked to identify the three most helpful features of product detail pages to their decision to purchase beauty products, 62% of respondents who do purchase beauty products online chose written reviews, with an additional 51% selecting review stars. These were the top two options, as shoppers rely heavily on the opinions of those who have purchased products previously.

Comparisons to similar products came in third at 47%, while photos came in just behind in fourth with 47% of respondents also selecting it as a top three feature.

Videos were only selected as a top three feature by 37% of online beauty shoppers, but that share jumps to 45% among Gen Z. Just 27% of baby boomers who buy beauty products online thought videos were a particularly helpful feature.

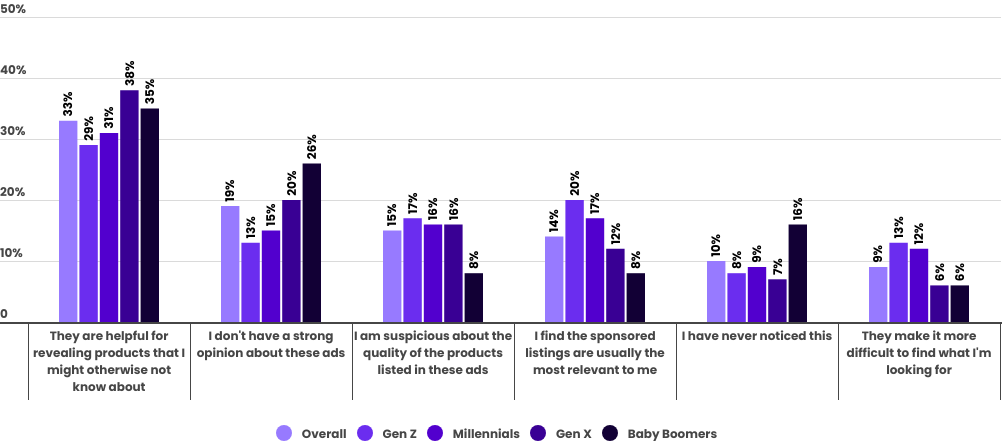

When asked about how they feel about sponsored product listings on sites like Amazon or Walmart, one third said that these listings are helpful for revealing products they might otherwise not know about, the most popular answer. Another 14% believed that sponsored listings are usually the most relevant listings to them, as retail media ads are seen as a positive feature of online marketplaces for many beauty shoppers.

Gen Z was the most opinionated about sponsored product listings, but those opinions differed within the group. Just 13% of Gen Z said they didn’t have a strong opinion of sponsored listings, compared to 26% for baby boomers. Gen Z was the most likely generation to say they were suspicious of the quality of the products in sponsored listings, but also the most likely to say that the sponsored listings were usually the most relevant.

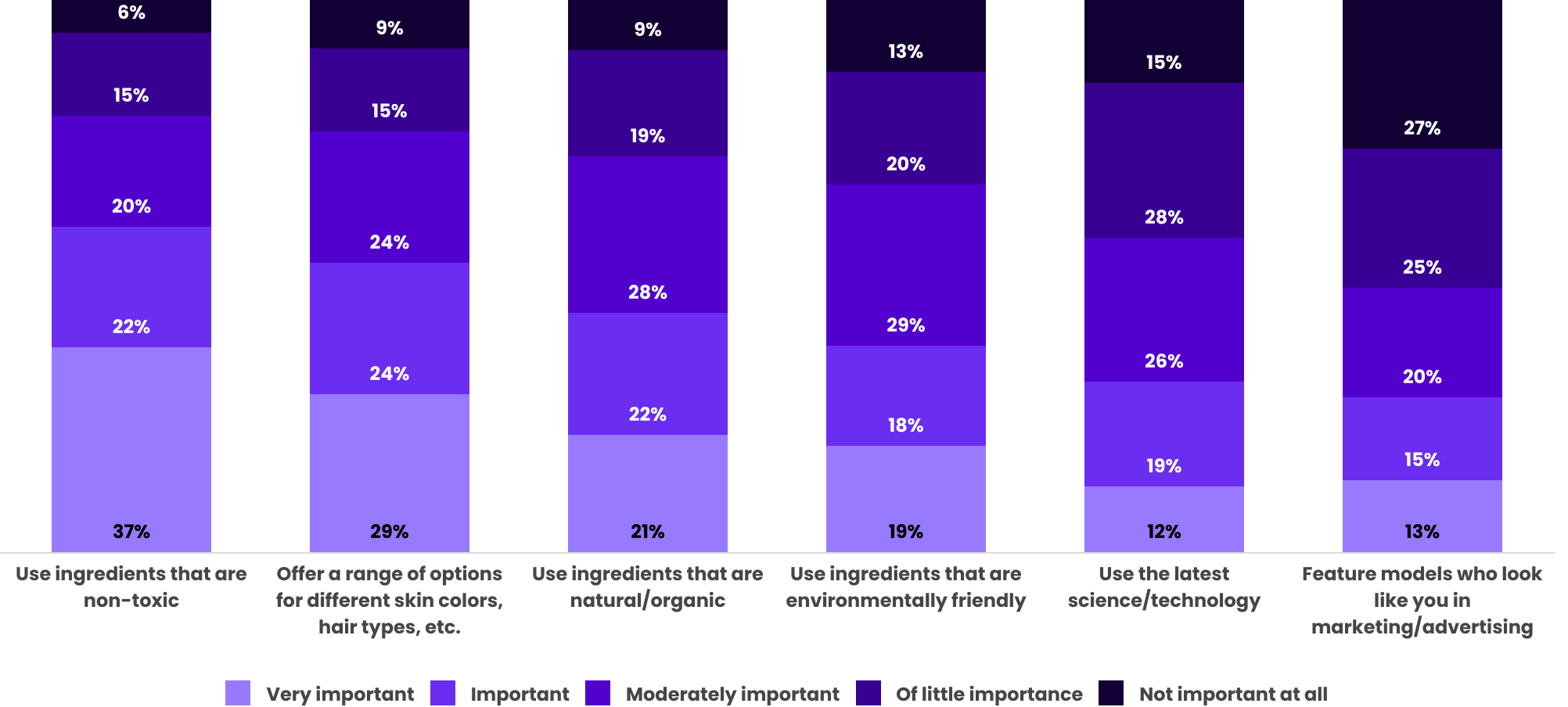

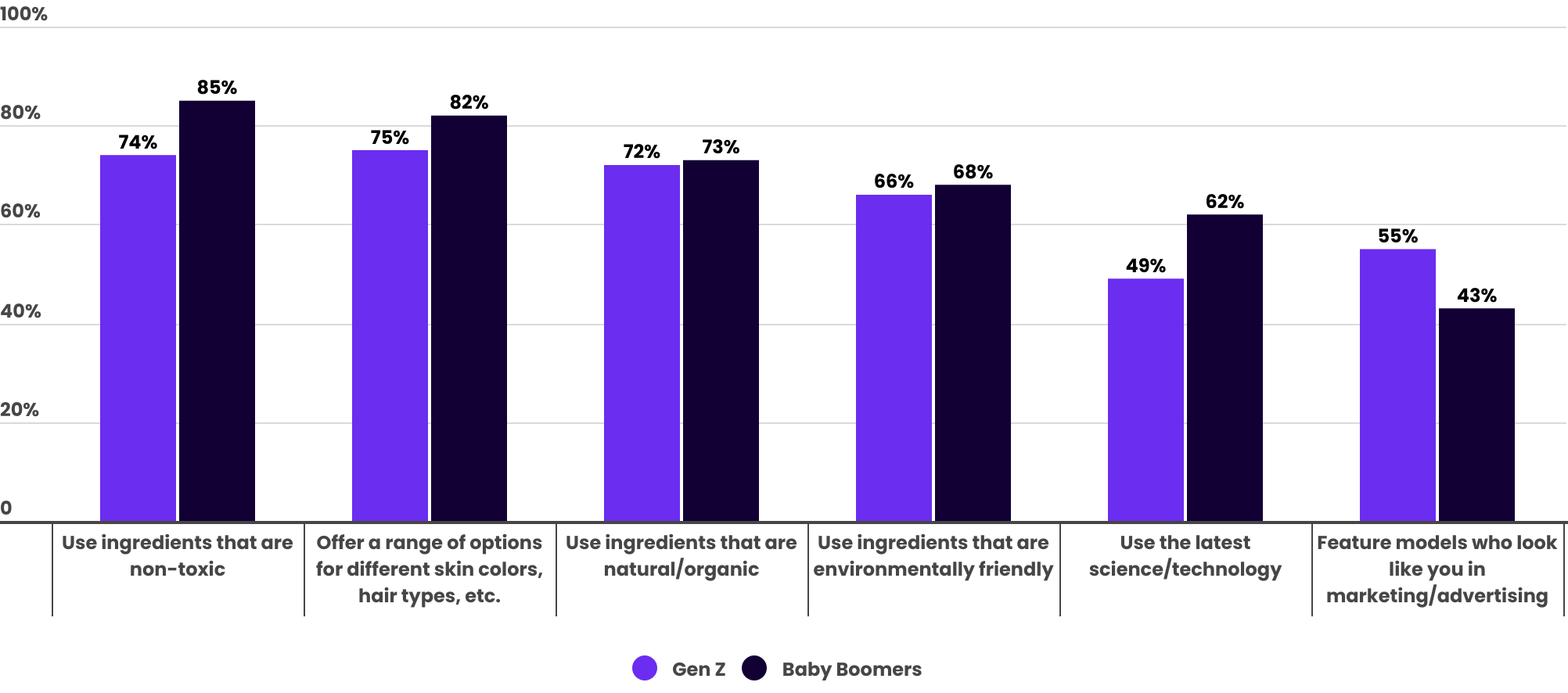

Nearly 60% of respondents said that products being non-toxic was important or very important to their decision to purchase a beauty brand’s products, compared to just 6% who said this was not at all important. Over 50% of respondents said that a brand offering a range of options for different skin colors and hair types is important or very important to beauty purchase decisions.

While respondents confirmed that a diverse product selection is important, fewer believed that it was important to feature models who look like them in marketing/advertising, and 27% believed this was not at all important.

Among Gen Z, only 19% of respondents said that it was not important at all to feature models who look like them in advertisements. For baby boomers that share was 37%. There was greater agreement across generations that it is important for a beauty brand to offer a range of options for different skin colors, hair types, etc. 75% of Gen Z felt this was at least moderately important, while 82% of baby boomers agreed.

Check out our most recent Beauty Marketing Study for exclusive insights.