Cyber Five 2022: Black Friday and Cyber Monday Ad Trends Across Google, Amazon and Meta

Another record-breaking stretch from Thanksgiving through Cyber Monday is in the bag for marketers. As many look to take stock of what happened over this pivotal five-day period, we examined same-store samples from more than $3 billion in annual ad spend under management to unpack what happened across the biggest digital marketing platforms.

Here’s what we found.

This post was coauthored by Andy Taylor and Mark Ballard.

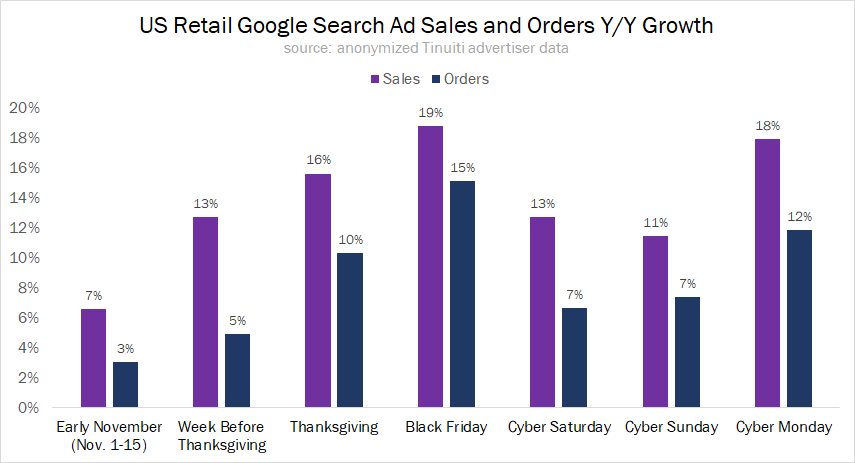

Heading into the Cyber Five stretch running from Thanksgiving through Cyber Monday, growth in retailer sales attributed to Google search ads was already beginning to pick up from a relatively modest showing earlier in the quarter. During the week before Thanksgiving, Google search ad sales rose 13% year over year, up from 7% growth during the first half of November.

Google sales rose 16% Y/Y on Thanksgiving and an impressive 19% on Black Friday. Sales growth cooled a bit over the weekend, but remained above early November levels. On Cyber Monday, sales growth picked back up, but didn’t quite match Black Friday levels.

These results are nearly the inverse of the trends advertisers saw a year earlier, when strong early November growth slowed sharply over Thanksgiving and Black Friday as many consumers at the time were travelling for the first time in two years.

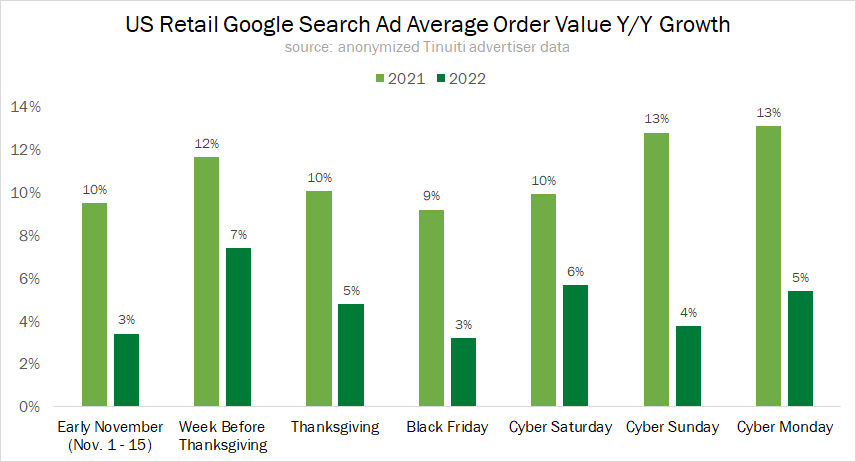

Growth in the average value of orders generated by Google search ads has been slowly decelerating from a peak of 14% in mid-2021. As inflationary pressure has waned and year-ago average order value (AOV) comps have strengthened, AOV has been a smaller driver of year-over-year Google sales growth, including over the Cyber Five.

In 2022, Google AOV rose by 5% over the Cyber Five, down from an average of 10% growth a year earlier. In 2021, advertisers saw flat or declining order volume on three of the five days between Thanksgiving and Cyber Monday, but strong AOV growth kept sales growth in positive territory. This year, order growth drove the bulk of retailers’ sales growth.

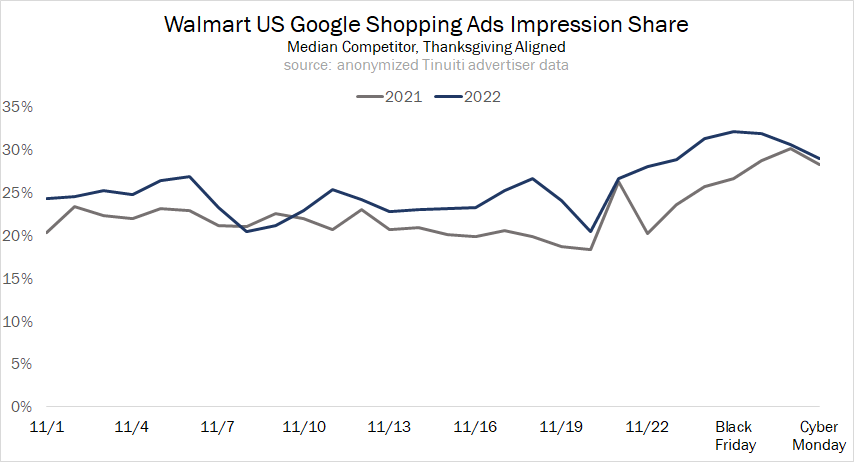

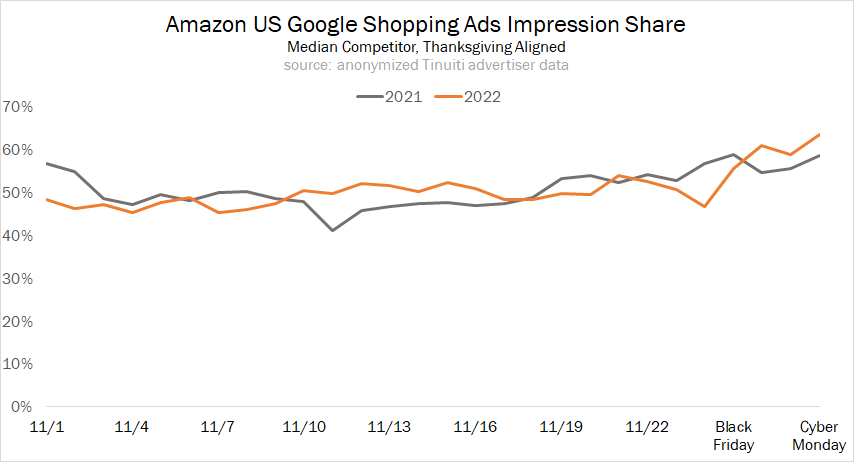

In our mid-Q4 update post, we noted how Walmart’s share of Google Shopping impressions had run below 2021 levels for most of Q3, before picking up sharply in late September and early October. Into the Cyber Five period, Walmart maintained a more aggressive stance in Google Shopping auctions, but by Cyber Monday its Shopping impression share was running just slightly above a year earlier.

For its part, Amazon appears to be employing a very similar strategy in Google Shopping auctions as it did in 2021. Although it dipped a bit on Thanksgiving, Amazon’s share of Google Shopping impressions has been on the rise since. In 2021, Amazon appeared to get much aggressive in Google auctions beginning the week of Cyber Monday and peaking in mid-December. Its competitors are now seeing signs of a similar ramp up this week.

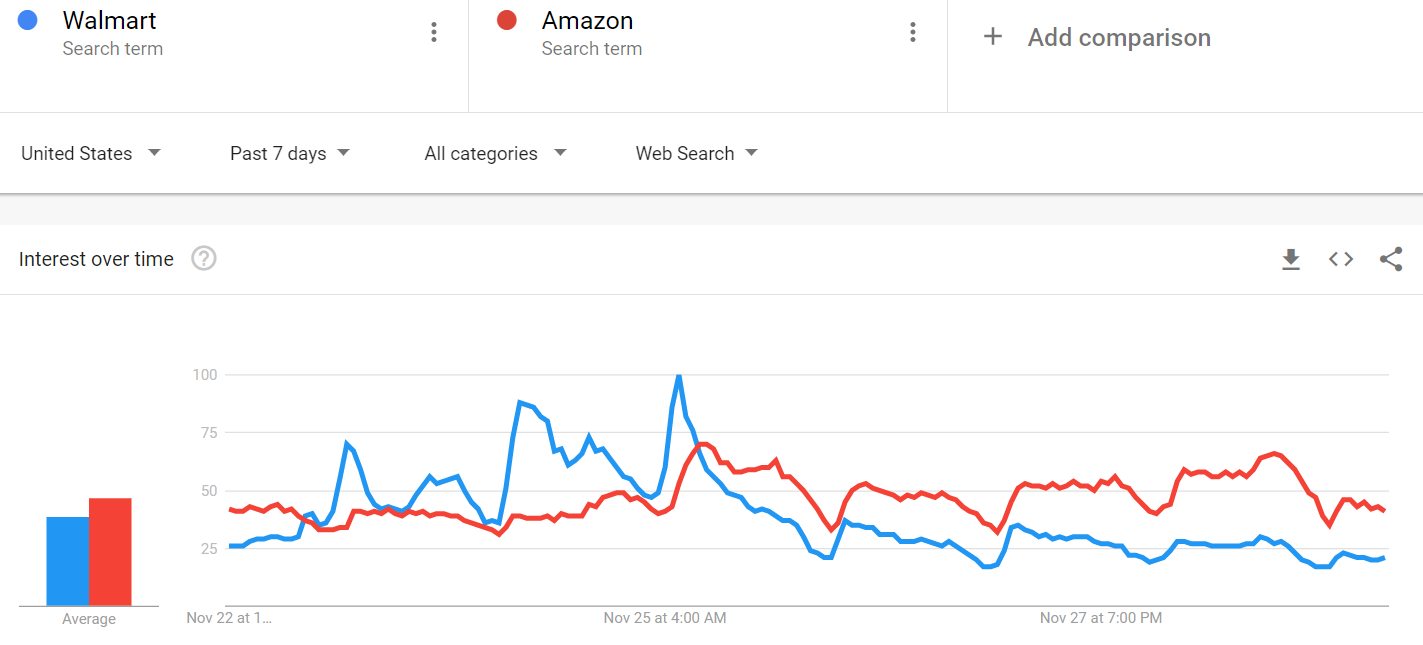

Taking a look at official Google Trends search volume for ‘Amazon’ vs ‘Walmart,’ it’s clear that the largest ecommerce store in the US is no match for the brick-and-mortar presence of Walmart when it comes to online search interest in the lead up to Black Friday, which is historically an in-store shopping event. Walmart interest topped that of Amazon the day before Thanksgiving, and remained higher until late morning on Black Friday.

However, Walmart’s stint on top was very short-lived, as search interest in Amazon surged relative to Walmart in the late morning hours of Black Friday and never looked back.

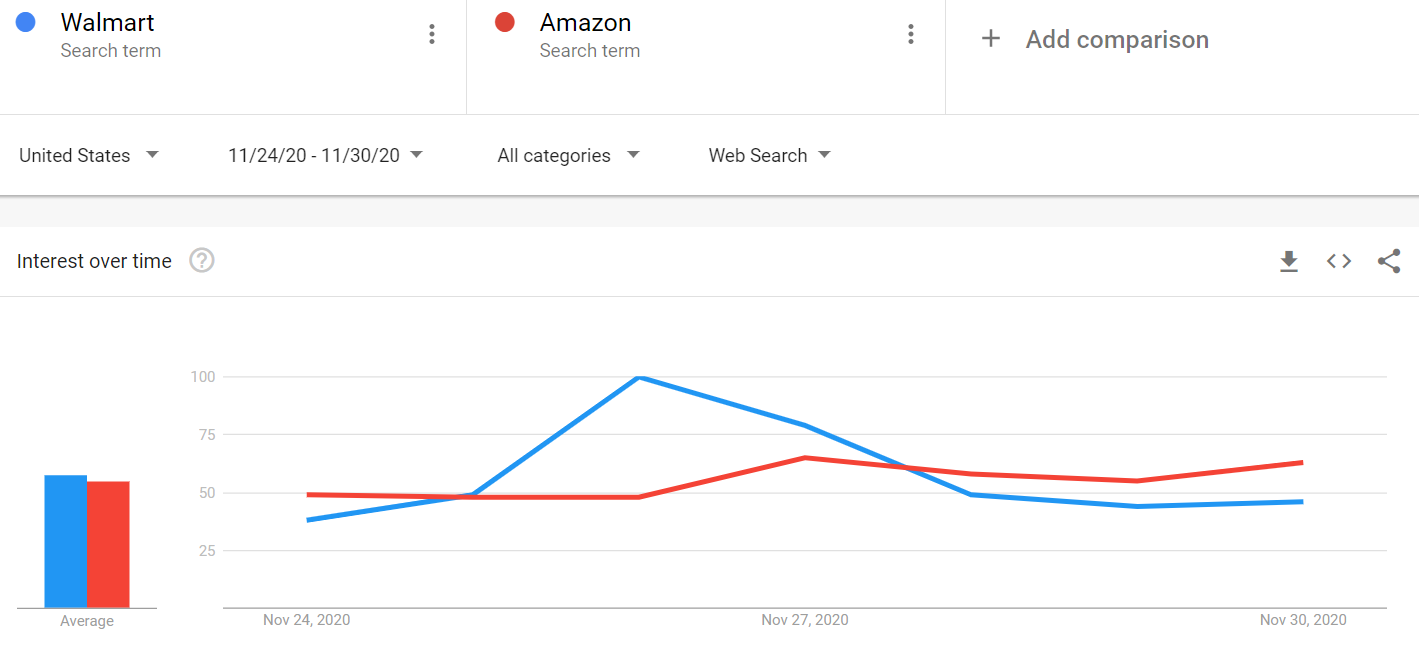

A similar trend played out in 2021 and, somewhat surprisingly, was even the case in the pandemic-affected Black Friday stretch of 2020.

Moving forward, it shouldn’t be surprising to anyone that search interest for brick-and-mortar players like Walmart is elevated heading into Black Friday compared to ecommerce-only counterparts, or that that trend reverses itself after the event.

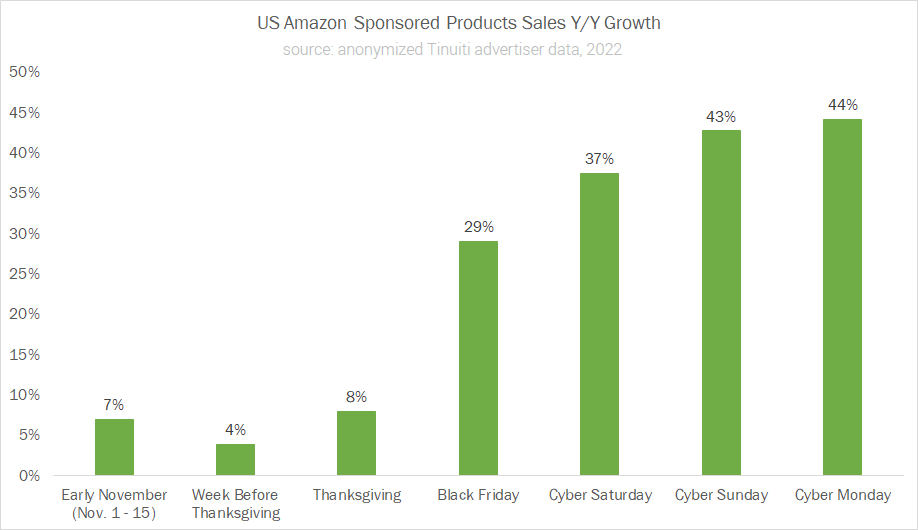

Even with brick-and-mortar stores top of mind for many US consumers, sales attributed to Amazon Sponsored Products exploded on Black Friday, and only grew stronger heading into Cyber Monday.

Much like on the Google search side of things, sales attributed to Amazon Sponsored Products grew only modestly over the first half of November, rising 7% compared to last year. This dipped to just 4% growth in the week before Thanksgiving, but quickly ramped up to 29% growth on Black Friday before peaking at 44% on Cyber Monday.

With many consumers focused on finding good deals in this year of economic uncertainty, it’s clear that many waited until sales holidays like Black Friday and Cyber Monday to make purchases. Advertisers that remained aggressive during this time saw the rewards of doing so.

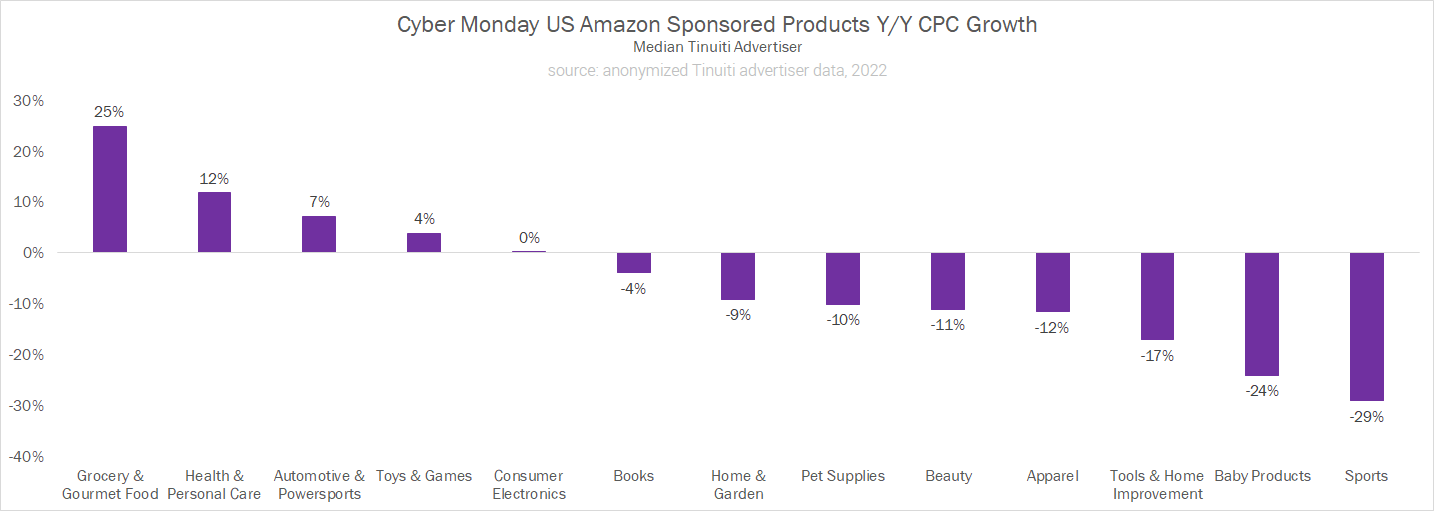

CPC growth for Amazon advertisers has been leveling off for several quarters now, and in Q3 Sponsored Products CPC was actually down year over year for six of thirteen major product categories tracked in our quarterly benchmark report.

This trend continued into the holiday shopping season, and on Cyber Monday CPC was down for the median advertiser in more than half of the product categories studied.

This is a welcome sign for many advertisers that the competitive pressures that have driven up ad pricing over the last couple of years are starting to level out.

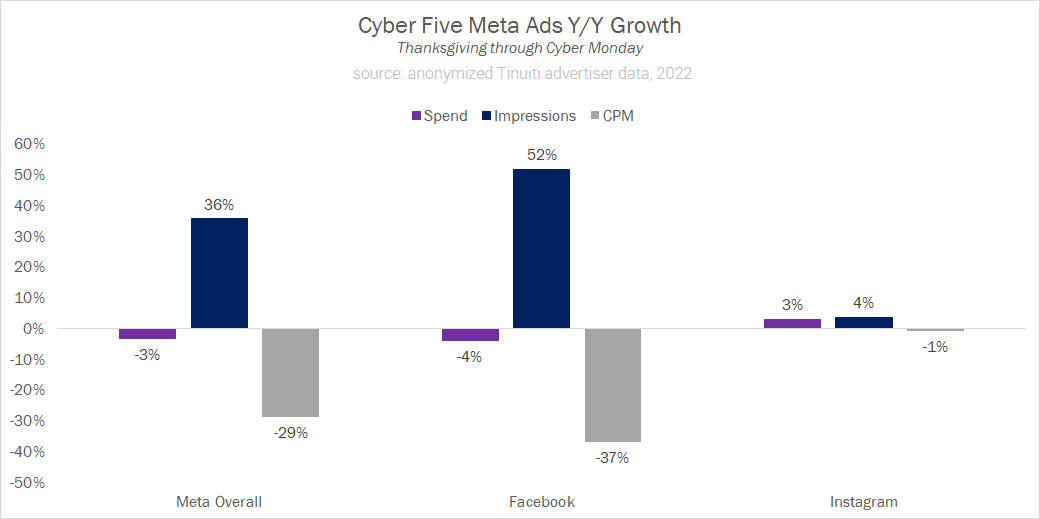

Amazon wasn’t the only major ad platform to see declines in ad pricing over the Cyber Five, as Meta advertisers also found much cheaper CPM this year.

If you’ve been keeping up with our blog, you know that Meta CPM was softer than a year earlier through the first half of Q4 2022, as ad auctions appear to have become less competitive than in 2021.

This trend continued into the pivotal Cyber Five stretch, during which CPM was down 29% across all Meta properties. However, the drop was much more pronounced for Facebook, where CPM fell 37%, than for Instagram, which saw just a 1% decline compared to last Cyber Five.

Total Meta spend was down 3% year over year, but 49% of Tinuiti advertisers increased their spend to some extent over this five-day stretch, and 38% ramped up investment by at least 25%, as not all advertisers pulled back.

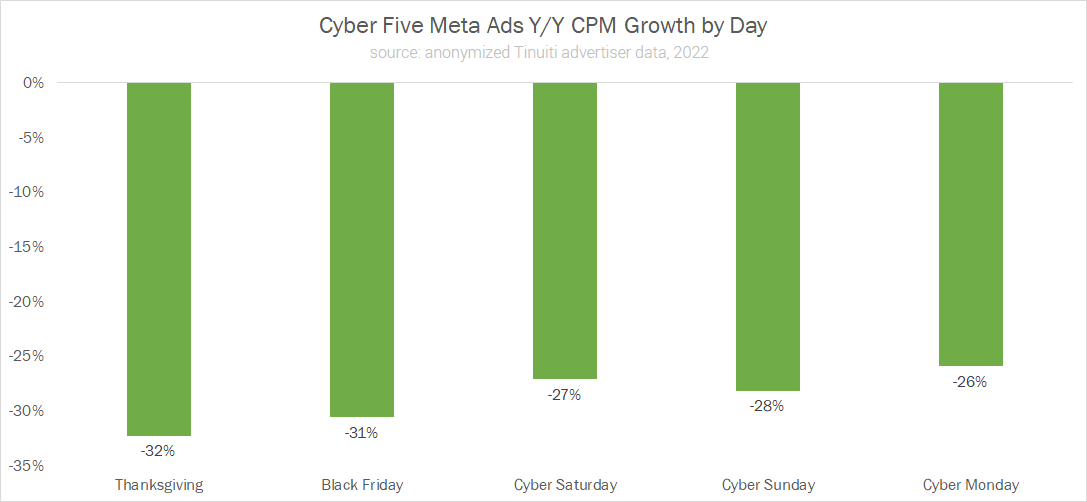

Looking at how ad pricing trended throughout this core five-day period, declines grew smaller from Thanksgiving through Cyber Monday, with CPM down 26% on Cyber Monday compared to a 32% drop on Thanksgiving. Judging by this trend, it appears that ad auctions got relatively more competitive heading into the biggest US online shopping day of the year.

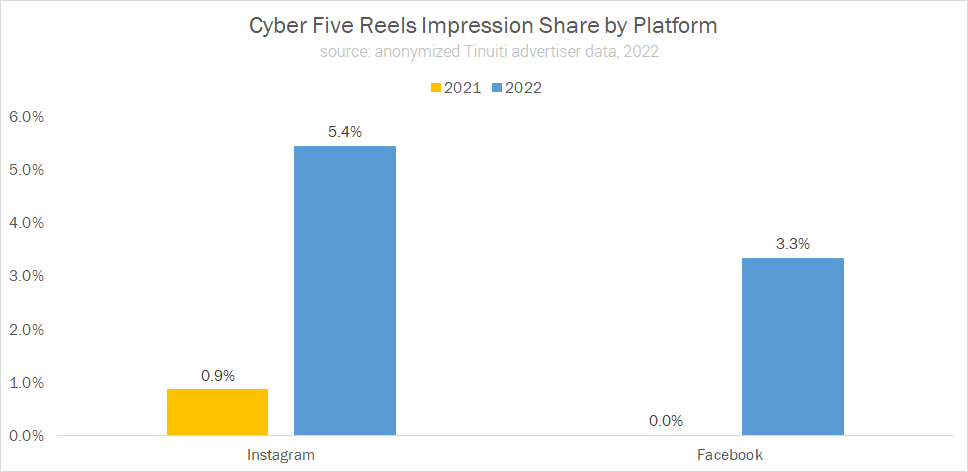

Meta has publicly stated that Reels now account for more than 20% of time spent in the Instagram app, as the social giant seeks to gain traction with its vertical video format built to rival TikTok.

For advertisers, this has meant steady growth in the share of ad impressions attributed to Reels, not only on Instagram but also on Facebook. Over the course of the Cyber Five, Reels accounted for 5.4% of Instagram ad impressions, compared to just 0.9% last year, while Facebook Reels placements (including Reels Overlay ads) rose from no impression share last Cyber Five to 3.3% in 2022.

Cyber Five Facebook and Instagram Reels impression shares also showed growth relative to Q3. It’s still early days for Reels placements, but the format is steadily gaining traction as we head into the final month of the year.

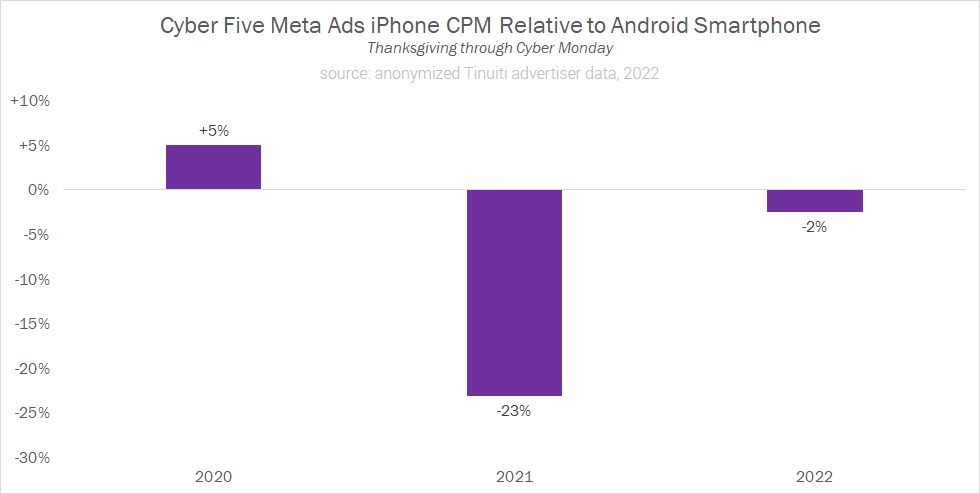

Apple’s App Tracking Transparency (ATT) prompt had significant impacts on device trends starting in 2021, as targeting and measurability was interrupted for users who opted out of tracking on iOS devices and ad auctions were relatively more competitive for those users who could still largely be targeted and measured using mobile IDs (like Android users). During the 2021 Cyber Five, advertisers saw iPhone CPMs run 23% lower than Android smartphone CPMs. In 2020, iPhone CPMs had run 5% higher than Android CPMs.

Whether by virtue of advertisers updating their targeting over the last year, Meta adjusting how opted-out iOS users are assigned to audiences, or both, CPM for these two device types was nearly identical from Thanksgiving through Cyber Monday in 2022.

The road to this convergence has steadily played out over the last couple of quarters, with Android smartphone CPM down to just 9% higher in Q3 2022 after coming in at 46% higher in the first quarter of the year. While ATT is certainly still affecting reporting and advertiser strategies on Meta, the gap in CPM for Android relative to iOS devices in particular appears to be waning.

VP, Research

Andy Taylor is the VP of Research at Tinuiti, where he leads proprietary data research that translates billions in annual ad spend into clear, actionable insights for brands. He lives in Richmond, VA, where he enjoys running, tending his yard, and binge‑watching baking shows.